Tony Kryzanowski

Canadians faced with escalating fuel costs, crushing grocery bills and higher rent are understandably less concerned about the environment these days, according to the latest public opinion polls. And predictably, politicians eager for re-election are following the polls in terms of their own priorities. But the numbers don’t lie. The world is becoming warmer and climate change is real. The consequences go far beyond the recent ferocity of repeated massive forest fires right across Canada. Given what appears to be a more muted voice in environmental advocacy these days, this is the forestry sector’s moment to present itself as Canada’s strongest champion for the environment because we undeniably have a great story to tell. …A good starting point for industry to develop its environmental advocacy strategy is to take stock.

We should revisit past important research and development initiatives as it relates to wood fibre as the feedstock. This includes further commercialization of bio-based nanotechnology from cellulose, expanding the market for mass timber products, exploring afforestation potentially with fast-growing wood species to grow the wood basket while also expanding the forest footprint to achieve greater carbon sequestration, substituting wood pellets for diesel to provide power to northern communities, and rehabilitating landscapes marred by industrial activity. …It’s astounding to think of how many billions of dollars of investment are being considered for such unproven practices as carbon dioxide sequestration from Canada’s oil and gas industry, when trees represent the largest, single natural carbon sequestration tool on the planet—and Canada has the second largest landmass in the world. …The field is now so much more wide open and desperately looking for a champion to remind us that climate change is here to stay—unless we take action and that forestry can and should be a much bigger part of the solution.

We find ourselves once again compelled to address the

We find ourselves once again compelled to address the

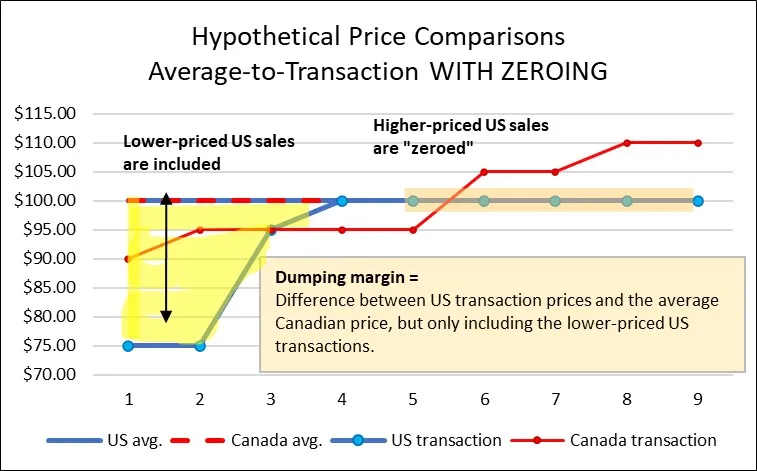

With President-elect Trump set to take over the Oval Office on January 20, the Canadian lumber industry looks to be taking action… advising customers that they will add 25% to lumber exports to the US when the tariff is announced. With Canadian mills already paying an average of 14.4% import duties on US shipments, they have no alternative but to increase prices by the 25% to cover the potential tariff. Nic Wilson, CEO of the Denver Mass Timber Group Summit reports that… “

With President-elect Trump set to take over the Oval Office on January 20, the Canadian lumber industry looks to be taking action… advising customers that they will add 25% to lumber exports to the US when the tariff is announced. With Canadian mills already paying an average of 14.4% import duties on US shipments, they have no alternative but to increase prices by the 25% to cover the potential tariff. Nic Wilson, CEO of the Denver Mass Timber Group Summit reports that… “

In the face of significant challenges—from mill closures to tariffs and shifting global markets—one question we hear more than any other from people: “What can I actually do to help?” When the headlines are dominated by uncertainty, it can feel like the hurdles facing the forest industry are too large for any one person to influence. But there is a powerful way to make your voice heard and tell the provincial government it isn’t just an industry priority but a priority for every British Columbian that wants a resilient future.

In the face of significant challenges—from mill closures to tariffs and shifting global markets—one question we hear more than any other from people: “What can I actually do to help?” When the headlines are dominated by uncertainty, it can feel like the hurdles facing the forest industry are too large for any one person to influence. But there is a powerful way to make your voice heard and tell the provincial government it isn’t just an industry priority but a priority for every British Columbian that wants a resilient future.

The BCTS Review that was launched in January 2025, and co-chaired by Brian Frenkel, Lenny Joe and George Abbott, is nearing an end for public input intake. The BC government describes this initiative as a periodic review to ensure BCTS is evolving in an ever-changing marketplace while meeting its mandate commitments. The reality is that BCTS performance has been seriously impacted over the last few years. This review comes as the Premier seeks to meet his mandated target for a timber harvest of 45 million m3. Raising the BCTS harvest off its historic lows will help the Premier in his drive to 45!

The BCTS Review that was launched in January 2025, and co-chaired by Brian Frenkel, Lenny Joe and George Abbott, is nearing an end for public input intake. The BC government describes this initiative as a periodic review to ensure BCTS is evolving in an ever-changing marketplace while meeting its mandate commitments. The reality is that BCTS performance has been seriously impacted over the last few years. This review comes as the Premier seeks to meet his mandated target for a timber harvest of 45 million m3. Raising the BCTS harvest off its historic lows will help the Premier in his drive to 45! Well, 2025 will prove to be an interesting year ahead. …Provincially there are some glimmers of hope for some directional changes to the current trajectory of BC’s forest sector through the appointment of an energized and determined Minister of Forests. At the recent TLA convention, there also seemed to be acknowledgment that the need for change was recognized with the Premier and Minister. …The government’s forestry mandate appears to be granted for firm actions, even more so with our obvious need for more self-reliance as a country. But muddying the background is the reality that anything that needs to be accomplished must be done within the spectre of massive provincial deficits and a hiring freeze. Where to start?

Well, 2025 will prove to be an interesting year ahead. …Provincially there are some glimmers of hope for some directional changes to the current trajectory of BC’s forest sector through the appointment of an energized and determined Minister of Forests. At the recent TLA convention, there also seemed to be acknowledgment that the need for change was recognized with the Premier and Minister. …The government’s forestry mandate appears to be granted for firm actions, even more so with our obvious need for more self-reliance as a country. But muddying the background is the reality that anything that needs to be accomplished must be done within the spectre of massive provincial deficits and a hiring freeze. Where to start?

As most may have heard by now, Premier Eby has announced an agreement in principle between the BC NDP and Greens. …Of key significance to the forest sector, the agreement commits “to undertake a review of BC forests with First Nations, workers, unions, business and community to address concerns about sustainability, jobs, environmental protection and the future of the industry.” Such broad encompassing reviews typically take several months, if not over a year to complete and even longer before acting on recommendations. To propose such a review now is a prime example of just how forestry in British Columbia has truly become all about politics and not common sense. The two parties in their wisdom, have agreed to a review while the BC forest industry is literally in its death throes.

As most may have heard by now, Premier Eby has announced an agreement in principle between the BC NDP and Greens. …Of key significance to the forest sector, the agreement commits “to undertake a review of BC forests with First Nations, workers, unions, business and community to address concerns about sustainability, jobs, environmental protection and the future of the industry.” Such broad encompassing reviews typically take several months, if not over a year to complete and even longer before acting on recommendations. To propose such a review now is a prime example of just how forestry in British Columbia has truly become all about politics and not common sense. The two parties in their wisdom, have agreed to a review while the BC forest industry is literally in its death throes.

Planting a tree can seem like an easy win for the planet. It’s a popular pledge for corporations and organizations eager to participate in sustainability programs and promote environmental responsibility. But here’s the catch: not all trees have the same impact, and not all tree-planting efforts contribute to forest sustainability. As we approach International Day of Forests, it’s worth asking: Are we missing the forests for the trees? Many sustainability programs focus on planting but often overlook the critical role of future forest management — particularly the need for processes like forest thinning. Thinning removes competitive trees which allows the healthiest trees to grow larger and more valuable, and be better equipped to withstand droughts, wildfires, diseases and insect infestations.

Planting a tree can seem like an easy win for the planet. It’s a popular pledge for corporations and organizations eager to participate in sustainability programs and promote environmental responsibility. But here’s the catch: not all trees have the same impact, and not all tree-planting efforts contribute to forest sustainability. As we approach International Day of Forests, it’s worth asking: Are we missing the forests for the trees? Many sustainability programs focus on planting but often overlook the critical role of future forest management — particularly the need for processes like forest thinning. Thinning removes competitive trees which allows the healthiest trees to grow larger and more valuable, and be better equipped to withstand droughts, wildfires, diseases and insect infestations.