The US tariff regime is far from over despite a US Supreme Court ruling striking down last year’s tariffs authorized by President Trump under the International Emergency Economic Powers Act (IEEPA). Although the court noted in its ruling that the president overstepped his authority in applying reciprocal tariffs on virtually all trading partners, it did leave the door open for other means of tariff application—and the US Administration has wasted no time in charging through that door, turning to Section 122 of the Trade Act of 1974 to impose new global tariffs of 10% (likely moving to 15%). Tariffs under Section 122 expire after 150 days without congressional approval, but we assume other options will be put in place before expiry (Section 232, 301 or some other creative mechanism).

The US tariff regime is far from over despite a US Supreme Court ruling striking down last year’s tariffs authorized by President Trump under the International Emergency Economic Powers Act (IEEPA). Although the court noted in its ruling that the president overstepped his authority in applying reciprocal tariffs on virtually all trading partners, it did leave the door open for other means of tariff application—and the US Administration has wasted no time in charging through that door, turning to Section 122 of the Trade Act of 1974 to impose new global tariffs of 10% (likely moving to 15%). Tariffs under Section 122 expire after 150 days without congressional approval, but we assume other options will be put in place before expiry (Section 232, 301 or some other creative mechanism).

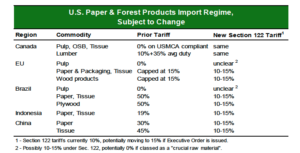

With respect to the forest products industry, cessation of IEEPA tariffs and application of these new Section 122 tariffs have no impact on existing lumber duties (35% remains intact), nor for any existing tariffs under Section 232 (at 10%) or goods currently compliant under USMCA (such goods remain tariff-free under Section 122). Although USMCA-compliant goods are safe from tariffs for now, with that trade deal being reviewed this summer the tariff-free flow of goods among the US, Mexico and Canada could be upended. Since almost all newsprint supply comes from Canada (see page 19), that fear is ostensibly already causing U.S. buyers to accelerate purchases.

The table details what we know at the moment about the new tariff regime (Section 122 at 10% but probably moving to 15%). Brazil and China appear to be winners in these latest moves, but, with other mechanisms available to Trump, we don’t think these recent tariff reductions are going to lead to any dramatic increase in imports from these countries (uncertainty seems to be part of the goal under Trump’s methods).

The table details what we know at the moment about the new tariff regime (Section 122 at 10% but probably moving to 15%). Brazil and China appear to be winners in these latest moves, but, with other mechanisms available to Trump, we don’t think these recent tariff reductions are going to lead to any dramatic increase in imports from these countries (uncertainty seems to be part of the goal under Trump’s methods).

Forest Products Outlook:

- Solid Wood: Lumber prices are diverging as S-P-F keeps nudging up while SYP falls (most SYP production is above breakeven). A strong spring season is possible if producers don’t outrun the market. Panel demand is weak, but new capacity has been delayed (and WFG is shutting a mill).

- Timber/Log: Log prices are generally flat to down, even as end markets show some life. Export options are limited. Timberland values continue to defy the reality of weak cash flows.

- Pulp prices are moving up lately, and more so for hardwood than softwood. Hardwood production is being negatively impacted by various issues while softwood continues to languish below cash-cost levels. Spring’s arrival and the end of Lunar New Year will be key to watch.

- Paper prices were stable this month but are set to move higher in March for a raft of grades. Newsprint’s $50 hike looks to succeed, while increases for other uncoated mechanical grades will likely fall short. For uncoated woodfrees, initial feedback is that price increases are gaining traction but will not be fully in place next month (but a meaningful amount to be in place by April).

- Containerboard: Producers are working on trying to push through their March price hikes ($70)—but now with the backdrop of PPI Pulp & Paper Week having just lowered its price assessment by $20. Massive capacity reductions are driving the market more than demand (which remains sluggish). This hike will take some time to implement and will likely come up a bit short.

- Boxboard: Oversupply remains a key issue for boxboard, and SBS/FBB in particular. The shut by Smurfit (La Tuque, QC) helps but isn’t enough. CRB has been losing market share to bleached grades (SBS/FBB) and we suspect will need to respond with more competitive pricing. The demand outlook remains weak given challenges in consumer spending coupled with the impact of GLP-1 drugs on food consumption. We foresee more shuts this year before prices improve.