We find ourselves once again compelled to address the US Lumber Coalition‘s (USLC) inaccurate commentary about the Canadian softwood lumber trade with the US in their March 24 release, “Canadian Imports Are Being Replaced by US Production – A Direct Result of US Trade Law Enforcement & Section 232 Tariff”. …Since October 2025, combined US duties and tariffs, averaging 45.16%, during flat periods of US demand coupled with low prices has meant that Canadian mills cannot compete until prices move higher. Consequently, it was inevitable that the highest cost producing regions in Canada would reduce shipments to the US. The USLC is endorsing these trade penalties which are essentially a subsidy for US sawmills. …Market share decline since 2016 is not just a result of duties and tariffs. …BC is the main reason for reduced Canadian lumber exports to the US. With very high domestic log costs, BC has had the lowest sawmilling margins in North America since 2017, as such, it is difficult to accept the USLC claim that BC has “unfair prices… and dumps lumber in the US.”

We find ourselves once again compelled to address the US Lumber Coalition‘s (USLC) inaccurate commentary about the Canadian softwood lumber trade with the US in their March 24 release, “Canadian Imports Are Being Replaced by US Production – A Direct Result of US Trade Law Enforcement & Section 232 Tariff”. …Since October 2025, combined US duties and tariffs, averaging 45.16%, during flat periods of US demand coupled with low prices has meant that Canadian mills cannot compete until prices move higher. Consequently, it was inevitable that the highest cost producing regions in Canada would reduce shipments to the US. The USLC is endorsing these trade penalties which are essentially a subsidy for US sawmills. …Market share decline since 2016 is not just a result of duties and tariffs. …BC is the main reason for reduced Canadian lumber exports to the US. With very high domestic log costs, BC has had the lowest sawmilling margins in North America since 2017, as such, it is difficult to accept the USLC claim that BC has “unfair prices… and dumps lumber in the US.”

…Canadian lumber production has always exceeded its consumption through much of the country’s modern history – Canada has a relatively small population and a vast forest resource. …The reality is that over the last 50 years, US lumber producers been not able to fully supply the US market demand. The huge gap between US production and consumption has ranged from a low of 12.0 billion board feet in 1990 to a high of 23.6 billion board feet in 2005 and was 12.7 billion board feet in 2025. The United States has benefited from a close trading relationship with Canada, especially through consistent access to economical and reliable lumber supplies. …That gap between US consumption and domestic supply exists today because US sawmills are operating close to full production – there is no “surplus production” without more logs, more workers, more capital – which are mostly domestic issues to effect any real change in production.

…Canadian lumber production has always exceeded its consumption through much of the country’s modern history – Canada has a relatively small population and a vast forest resource. …The reality is that over the last 50 years, US lumber producers been not able to fully supply the US market demand. The huge gap between US production and consumption has ranged from a low of 12.0 billion board feet in 1990 to a high of 23.6 billion board feet in 2005 and was 12.7 billion board feet in 2025. The United States has benefited from a close trading relationship with Canada, especially through consistent access to economical and reliable lumber supplies. …That gap between US consumption and domestic supply exists today because US sawmills are operating close to full production – there is no “surplus production” without more logs, more workers, more capital – which are mostly domestic issues to effect any real change in production.

The US says in a new report that Canada is failing to stop foreign goods made with forced labour from entering its market, a finding that coincides with Washington’s probe into the matter, which could lead to more tariffs. The 2026 National Trade Estimate Report on Foreign Trade Barriers from the US government says it appears Canada is importing goods that cost less than they should because they were made with forced labour. It’s an early indication of how the US will rule on Canada. …US customs policy treats all goods from China’s Xinjiang region as though they were made with forced labour unless importers can provide “clear and convincing evidence” to the contrary. …Canada passed a law, the

The US says in a new report that Canada is failing to stop foreign goods made with forced labour from entering its market, a finding that coincides with Washington’s probe into the matter, which could lead to more tariffs. The 2026 National Trade Estimate Report on Foreign Trade Barriers from the US government says it appears Canada is importing goods that cost less than they should because they were made with forced labour. It’s an early indication of how the US will rule on Canada. …US customs policy treats all goods from China’s Xinjiang region as though they were made with forced labour unless importers can provide “clear and convincing evidence” to the contrary. …Canada passed a law, the  OTTAWA — Provincial rules around alcohol and the federal government’s “Buy Canadian” policy have been flagged in a new report citing several trade irritants between Canada and the US. The annual document prepared by the Office of the US Trade Representative said market access barriers imposed by provincial liquor control boards “greatly hamper” exports of US wine, beer and spirits to Canada. …The report says U.S. companies have reported concerns about barriers in competing for contracts, including proving their Canadian subsidiary’s independence from a US parent company. Other issues listed in the report include delays with aircraft validation in Canada and high tariffs on U.S. dairy products. …Canada is still being slammed by Trump’s separate tariffs on industries like steel, aluminum, autos, lumber and cabinets. The Trump administration has launched investigations of a long list of countries, including Canada, citing forced labour in supply chains.

OTTAWA — Provincial rules around alcohol and the federal government’s “Buy Canadian” policy have been flagged in a new report citing several trade irritants between Canada and the US. The annual document prepared by the Office of the US Trade Representative said market access barriers imposed by provincial liquor control boards “greatly hamper” exports of US wine, beer and spirits to Canada. …The report says U.S. companies have reported concerns about barriers in competing for contracts, including proving their Canadian subsidiary’s independence from a US parent company. Other issues listed in the report include delays with aircraft validation in Canada and high tariffs on U.S. dairy products. …Canada is still being slammed by Trump’s separate tariffs on industries like steel, aluminum, autos, lumber and cabinets. The Trump administration has launched investigations of a long list of countries, including Canada, citing forced labour in supply chains.

The Home Depot currently offers more than a dozen AI-powered capabilities, with numerous others in development. …The Home Depot is simplifying the DIY journey by providing personalized, real-time advice that makes even the most complex projects feel achievable, paired with more seamless AI search and product discovery capabilities thanks to new technology integrations. Magic Apron & Outdoor Assistant—This virtual expert brings employee knowledge to customers virtually. With the Outdoor Assistant, customers can take a photo of a plant for immediate guidance on care, safety and sunlight. …Customers can now discover the latest Home Depot product catalog in ChatGPT. …Pros shop at The Home Depot an average of 60 times per year. Pros can create actionable job lists in minutes using natural language, voice-to-text or spreadsheet uploads. Pros can use AI to deliver complete material lists and project quotes in days instead of weeks.

The Home Depot currently offers more than a dozen AI-powered capabilities, with numerous others in development. …The Home Depot is simplifying the DIY journey by providing personalized, real-time advice that makes even the most complex projects feel achievable, paired with more seamless AI search and product discovery capabilities thanks to new technology integrations. Magic Apron & Outdoor Assistant—This virtual expert brings employee knowledge to customers virtually. With the Outdoor Assistant, customers can take a photo of a plant for immediate guidance on care, safety and sunlight. …Customers can now discover the latest Home Depot product catalog in ChatGPT. …Pros shop at The Home Depot an average of 60 times per year. Pros can create actionable job lists in minutes using natural language, voice-to-text or spreadsheet uploads. Pros can use AI to deliver complete material lists and project quotes in days instead of weeks. MAINE — As gas and diesel prices climb during the war in Iran, some of Maine’s most recognizable industries are feeling the strain. From the coast to the woods, people who rely on fuel to do their jobs say the higher costs are changing how they work and raising concerns about what comes next. Lobstermen are rethinking trips on the water, while logging contractors say the math is getting harder for truckers and mills across the state. …“I mean, there is no equipment that does not use diesel as its primary fuel for both harvesting and trucking,” Dana Doran, executive director of the Professional Logging Contractors of the Northeast, said. Doran said spiking diesel prices are adding roughly 20% to the cost of each trip a driver makes to and from a mill. That increase, he said, creates uncertainty for contractors and for mills that depend on a steady supply of wood.

MAINE — As gas and diesel prices climb during the war in Iran, some of Maine’s most recognizable industries are feeling the strain. From the coast to the woods, people who rely on fuel to do their jobs say the higher costs are changing how they work and raising concerns about what comes next. Lobstermen are rethinking trips on the water, while logging contractors say the math is getting harder for truckers and mills across the state. …“I mean, there is no equipment that does not use diesel as its primary fuel for both harvesting and trucking,” Dana Doran, executive director of the Professional Logging Contractors of the Northeast, said. Doran said spiking diesel prices are adding roughly 20% to the cost of each trip a driver makes to and from a mill. That increase, he said, creates uncertainty for contractors and for mills that depend on a steady supply of wood. Highly exposed to energy costs, today’s unpredictable global trade politics and the crisis in the Middle East are impacting the pulp and paper industry in many ways. These developments will certainly be reflected at Pulp & Beyond 2026, the leading forest-based bioeconomy event in Northern Europe, taking place on 15–16 April 2026 at the Helsinki Expo and Convention Centre in Helsinki, Finland. However, the main theme of this year’s event—focusing on the role of artificial intelligence in process industries, innovation within the forest sector, and the future of the bioeconomy—was defined before the Middle East war broke out, along with the subsequent oil and gas crisis, turbulence in global stock markets, and the growing risk of an unprecedented global recession.

Highly exposed to energy costs, today’s unpredictable global trade politics and the crisis in the Middle East are impacting the pulp and paper industry in many ways. These developments will certainly be reflected at Pulp & Beyond 2026, the leading forest-based bioeconomy event in Northern Europe, taking place on 15–16 April 2026 at the Helsinki Expo and Convention Centre in Helsinki, Finland. However, the main theme of this year’s event—focusing on the role of artificial intelligence in process industries, innovation within the forest sector, and the future of the bioeconomy—was defined before the Middle East war broke out, along with the subsequent oil and gas crisis, turbulence in global stock markets, and the growing risk of an unprecedented global recession.  OTTAWA — New data released by Statistics Canada suggests the economy was rebounding in the first few months of the year after a mild contraction to close 2025. The agency said on Tuesday real gross domestic product edged up 0.1% in January, helped by strength in goods-producing industries, which expanded by 0.2%. Looking ahead, the agency added that its preliminary estimate for February suggests the economy grew 0.2% for the month, though it cautioned the figure would be revised. Statistics Canada’s initial estimates for January published last month expected real GDP to be relatively flat. Doug Porter, chief economist at BMO, said “it does look like we had moderate growth in the first quarter of the year, which, given a lot of the other indicators, is not a bad place to be”. …Statistics Canada estimated the economy contracted 0.5% on an annualized basis in the final quarter of 2025.

OTTAWA — New data released by Statistics Canada suggests the economy was rebounding in the first few months of the year after a mild contraction to close 2025. The agency said on Tuesday real gross domestic product edged up 0.1% in January, helped by strength in goods-producing industries, which expanded by 0.2%. Looking ahead, the agency added that its preliminary estimate for February suggests the economy grew 0.2% for the month, though it cautioned the figure would be revised. Statistics Canada’s initial estimates for January published last month expected real GDP to be relatively flat. Doug Porter, chief economist at BMO, said “it does look like we had moderate growth in the first quarter of the year, which, given a lot of the other indicators, is not a bad place to be”. …Statistics Canada estimated the economy contracted 0.5% on an annualized basis in the final quarter of 2025. Lumber futures retreated toward $590 per thousand board feet as the cooling of the North American residential construction sector eroded the demand floor that had supported the market since January. The primary downward pressure stems from a slowdown in housing activity where single-family starts plunged 14.2% in March and building permits fell 5.4% signaling a sharp reduction in seasonal requirements. This demand destruction was catalyzed by a 11 basis point surge in mortgage rates to 6.45% following the Federal Reserve decision to hold interest rates steady alongside global inflationary spikes. While geopolitical tensions in the Strait of Hormuz initially pushed energy costs higher, the resulting increase in financing costs and a 10% drop in US housing starts outweighed the potential for supply chain disruptions. Furthermore a 2.4% increase in unsold builder inventory forced price cuts.

Lumber futures retreated toward $590 per thousand board feet as the cooling of the North American residential construction sector eroded the demand floor that had supported the market since January. The primary downward pressure stems from a slowdown in housing activity where single-family starts plunged 14.2% in March and building permits fell 5.4% signaling a sharp reduction in seasonal requirements. This demand destruction was catalyzed by a 11 basis point surge in mortgage rates to 6.45% following the Federal Reserve decision to hold interest rates steady alongside global inflationary spikes. While geopolitical tensions in the Strait of Hormuz initially pushed energy costs higher, the resulting increase in financing costs and a 10% drop in US housing starts outweighed the potential for supply chain disruptions. Furthermore a 2.4% increase in unsold builder inventory forced price cuts.

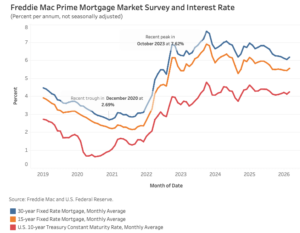

Mortgage rates, which dipped below 6% in February, climbed back up to end the month just under 6.4%. According to

Mortgage rates, which dipped below 6% in February, climbed back up to end the month just under 6.4%. According to  The landscape of the United States wood products industry in 2026 is being shaped by evolution from commodity lumber toward high-performance engineered wood systems. …While traditional sawmills have faced a turbulent consolidation period, the emergence of mass timber, specifically glulam and cross laminated timber, have created a high-growth sector that is increasingly more independent from the traditional volatility of the single-family residential market. …On the supply side, the wood industry is navigating a period of restructured supply and capacity following a series of significant mill closures in recent years. …Looking ahead to 2027 and beyond, as new mills come online, the industry is poised to move engineered wood products and mass timber from a niche specialty to a standard building practice. The core business challenge for the next 24 months will be the development of a more robust domestic supply chain that can support American builders amid logistics disruptions.

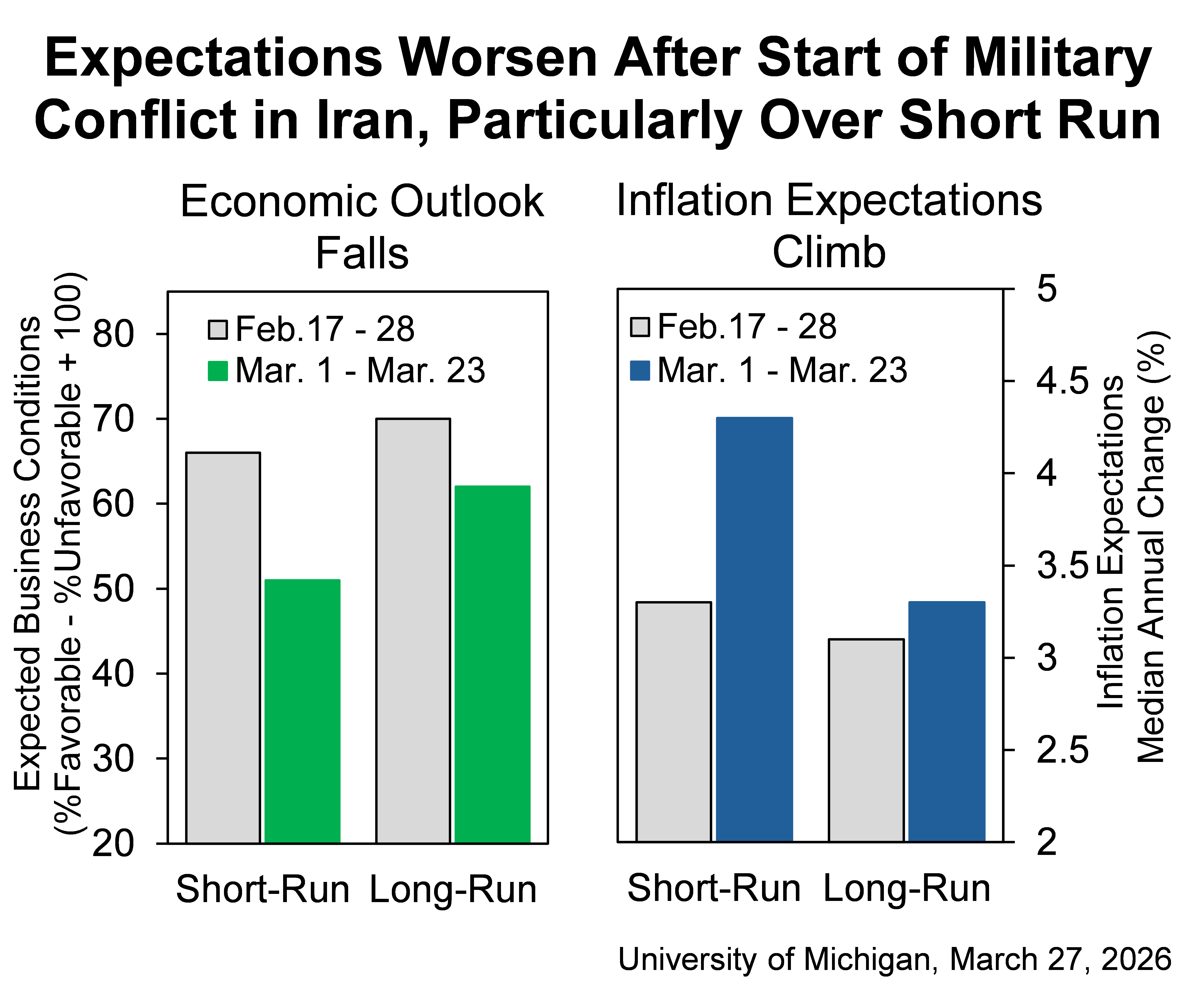

The landscape of the United States wood products industry in 2026 is being shaped by evolution from commodity lumber toward high-performance engineered wood systems. …While traditional sawmills have faced a turbulent consolidation period, the emergence of mass timber, specifically glulam and cross laminated timber, have created a high-growth sector that is increasingly more independent from the traditional volatility of the single-family residential market. …On the supply side, the wood industry is navigating a period of restructured supply and capacity following a series of significant mill closures in recent years. …Looking ahead to 2027 and beyond, as new mills come online, the industry is poised to move engineered wood products and mass timber from a niche specialty to a standard building practice. The core business challenge for the next 24 months will be the development of a more robust domestic supply chain that can support American builders amid logistics disruptions.  US consumer confidence unexpectedly edged up in March, but households anticipated higher inflation over the next 12 months amid a surge in gasoline prices and continued tariffs pass-through, a survey showed on Tuesday. The Conference Board said its consumer confidence index increased to 91.8 this month. Data for February was revised slightly down to show the index at 91.0 instead of 91.2. Economists polled by Reuters had forecast the index at 88.0. “Comments about prices and the cost of goods suggest that the cost of living remained at the top of consumers’ minds,” said Dana Peterson, chief economist at the Conference Board. Consumers’ average and median 12-month inflation expectations surged in March to levels last seen in August 2025. The month-long U.S.-Israeli war with Iran has sent global oil prices surging more than 50%.

US consumer confidence unexpectedly edged up in March, but households anticipated higher inflation over the next 12 months amid a surge in gasoline prices and continued tariffs pass-through, a survey showed on Tuesday. The Conference Board said its consumer confidence index increased to 91.8 this month. Data for February was revised slightly down to show the index at 91.0 instead of 91.2. Economists polled by Reuters had forecast the index at 88.0. “Comments about prices and the cost of goods suggest that the cost of living remained at the top of consumers’ minds,” said Dana Peterson, chief economist at the Conference Board. Consumers’ average and median 12-month inflation expectations surged in March to levels last seen in August 2025. The month-long U.S.-Israeli war with Iran has sent global oil prices surging more than 50%. National housing data shows deck inclusion in new homes remains below 18%, according to the US Census Bureau’s Survey of Construction. For dealers and distributors, that number doesn’t tell the whole story. It does, however, set the stage for a stronger, more profitable era for decking—especially in custom home construction and high-end remodel markets. Custom builds may represent a smaller slice of total housing starts, but they also make up a disproportionately larger share of premium decking materials and system upgrades. And that’s where one opportunity lies. In the custom builder market, decks are far from an afterthought. They’re often part of the architectural plan from Day 1—particularly in markets with walkout basements, elevated foundations, and building lots with natural views. …The stakes go beyond just a nice-looking place to sit outside. Today’s builders, remodelers, and homeowners need environmentally sound, code ready, and easy to install materials.

National housing data shows deck inclusion in new homes remains below 18%, according to the US Census Bureau’s Survey of Construction. For dealers and distributors, that number doesn’t tell the whole story. It does, however, set the stage for a stronger, more profitable era for decking—especially in custom home construction and high-end remodel markets. Custom builds may represent a smaller slice of total housing starts, but they also make up a disproportionately larger share of premium decking materials and system upgrades. And that’s where one opportunity lies. In the custom builder market, decks are far from an afterthought. They’re often part of the architectural plan from Day 1—particularly in markets with walkout basements, elevated foundations, and building lots with natural views. …The stakes go beyond just a nice-looking place to sit outside. Today’s builders, remodelers, and homeowners need environmentally sound, code ready, and easy to install materials.

Japan’s

Japan’s  Today, not only is Canada in a housing affordability crisis, but Build Canada Homes (BCH), the new federal agency-turned-Crown Corporation tasked with building affordable housing at record speed and scale, is already largely staffed, selecting projects, and hoping to break ground by this fall.

Today, not only is Canada in a housing affordability crisis, but Build Canada Homes (BCH), the new federal agency-turned-Crown Corporation tasked with building affordable housing at record speed and scale, is already largely staffed, selecting projects, and hoping to break ground by this fall. As more U.S. states consider extended producer responsibility (EPR) laws, the American Forest & Paper Association warns the policy could raise the cost of everyday goods, Midland reports. EPR raises costs for American families because it shifts recycling expenses onto manufacturers. Global studies show when there are new regulatory fees, prices for packaged items increase. EPR works like a consumption tax. It ultimately increases the overall cost of groceries, household goods and paper products. As a result, Americans will feel the impact when shopping at the grocery store and for everyday necessities, according to AF&PA. EPR will increase costs without improving paper recycling. …Extended Producer Responsibility requires companies to pay for collecting, recycling and disposing of their products. That’s true even for materials like paper that are already widely and successfully recycled today.

As more U.S. states consider extended producer responsibility (EPR) laws, the American Forest & Paper Association warns the policy could raise the cost of everyday goods, Midland reports. EPR raises costs for American families because it shifts recycling expenses onto manufacturers. Global studies show when there are new regulatory fees, prices for packaged items increase. EPR works like a consumption tax. It ultimately increases the overall cost of groceries, household goods and paper products. As a result, Americans will feel the impact when shopping at the grocery store and for everyday necessities, according to AF&PA. EPR will increase costs without improving paper recycling. …Extended Producer Responsibility requires companies to pay for collecting, recycling and disposing of their products. That’s true even for materials like paper that are already widely and successfully recycled today. DENMARK — The timber industry is intensifying efforts to expand the use of wood in construction, with a new action plan aiming to raise its market share to 20% by 2030. Launched under the “TiB 2.0” initiative by industry body Træ i Byggeriet, the strategy seeks to accelerate adoption by addressing key barriers, including restrictive building regulations, entrenched industry practices and limited knowledge of wood’s capabilities. Lauritz Rasmussen, head of the organisation’s secretariat, said the initiative builds on growing interest in timber as a sustainable building material but acknowledges progress has been too slow. He stated that “all reason dictates that we should use more wood for the climate, the environment and for the qualities for which wood is recognized”. The plan focuses on increasing visibility, improving documentation and promoting knowledge-sharing to influence decision-makers. Leadership changes also form part of the strategy, with Per Thomas Dahl of CLT Denmark appointed as the new chairman.

DENMARK — The timber industry is intensifying efforts to expand the use of wood in construction, with a new action plan aiming to raise its market share to 20% by 2030. Launched under the “TiB 2.0” initiative by industry body Træ i Byggeriet, the strategy seeks to accelerate adoption by addressing key barriers, including restrictive building regulations, entrenched industry practices and limited knowledge of wood’s capabilities. Lauritz Rasmussen, head of the organisation’s secretariat, said the initiative builds on growing interest in timber as a sustainable building material but acknowledges progress has been too slow. He stated that “all reason dictates that we should use more wood for the climate, the environment and for the qualities for which wood is recognized”. The plan focuses on increasing visibility, improving documentation and promoting knowledge-sharing to influence decision-makers. Leadership changes also form part of the strategy, with Per Thomas Dahl of CLT Denmark appointed as the new chairman. The construction industry is a major contributor to greenhouse gas emissions, mostly due to conventional materials production. Because of this, there is an urgent need for sustainable alternatives. Bio-based materials offer a promising alternative but remain underutilized. This study examines wood to derive insights that could support the broader adoption of bio-based alternatives. This research explores the systemic drivers and barriers to the diffusion of wood through interviews with key actors. A system dynamics model is developed to capture the main factors affecting wood diffusion and their interdependencies. …It shows that successful diffusion requires systemic innovation, necessitating collaboration across the ecosystem. This systemic analysis offers important insights for other bio-based materials, which differ in resource availability, applications, and production cycles, but face similar barriers such as workforce shortages, scalability, and societal acceptance. Overcoming these barriers requires targeted trainings and supportive policies.

The construction industry is a major contributor to greenhouse gas emissions, mostly due to conventional materials production. Because of this, there is an urgent need for sustainable alternatives. Bio-based materials offer a promising alternative but remain underutilized. This study examines wood to derive insights that could support the broader adoption of bio-based alternatives. This research explores the systemic drivers and barriers to the diffusion of wood through interviews with key actors. A system dynamics model is developed to capture the main factors affecting wood diffusion and their interdependencies. …It shows that successful diffusion requires systemic innovation, necessitating collaboration across the ecosystem. This systemic analysis offers important insights for other bio-based materials, which differ in resource availability, applications, and production cycles, but face similar barriers such as workforce shortages, scalability, and societal acceptance. Overcoming these barriers requires targeted trainings and supportive policies.  TOKYO — Leaders from the global forestry sector met last week in Tokyo to advance the

TOKYO — Leaders from the global forestry sector met last week in Tokyo to advance the  It’s a well-established fact that forests and water are deeply connected. For decades, paired-watershed experiments have shown that when we lose forests, the total amount of water flowing through our rivers tends to rise. But a critical question has remained unanswered: does this extra water come from previous reserves, or is it simply “new” rain that the land is failing to hold? Is forest loss causing our watersheds to lose their internal integrity and leak like a sifter? Our recent study at the University of BC analyzed 657 watersheds across the globe. By using a tool called the Young Water Fraction, we found that forest loss significantly accelerates how fast precipitation travels through a landscape. We estimate that for every 1% of forest lost, the “young water” in our streams increases by about 0.17%. Crucially, our research reveals that… the way we arrange forest patches can either aggravate or mitigate this leakage.

It’s a well-established fact that forests and water are deeply connected. For decades, paired-watershed experiments have shown that when we lose forests, the total amount of water flowing through our rivers tends to rise. But a critical question has remained unanswered: does this extra water come from previous reserves, or is it simply “new” rain that the land is failing to hold? Is forest loss causing our watersheds to lose their internal integrity and leak like a sifter? Our recent study at the University of BC analyzed 657 watersheds across the globe. By using a tool called the Young Water Fraction, we found that forest loss significantly accelerates how fast precipitation travels through a landscape. We estimate that for every 1% of forest lost, the “young water” in our streams increases by about 0.17%. Crucially, our research reveals that… the way we arrange forest patches can either aggravate or mitigate this leakage. ANCHORAGE, Alaska – The federal government isn’t holding public meetings on a rule that could reshape logging across the nation’s largest national forest — so a conservation group is doing it instead. The Southeast Alaska Conservation Council is hosting a series of community “public hearings” this month on the Tongass National Forest’s roadless rule. …The group plans to collect public testimony and submit it directly into the federal record as the US Forest Service weighs potential changes to those protections. Nathan Newcomer, SEACC’s Tongass campaigner, said the group stepped in after learning the Forest Service had no plans to hold its own public meetings. …The Forest Service is expected to publish a draft environmental impact statement on the roadless rule — a step that would open a formal public comment period. Newcomer said that the window is expected to last 30 days and could begin as soon as late April.

ANCHORAGE, Alaska – The federal government isn’t holding public meetings on a rule that could reshape logging across the nation’s largest national forest — so a conservation group is doing it instead. The Southeast Alaska Conservation Council is hosting a series of community “public hearings” this month on the Tongass National Forest’s roadless rule. …The group plans to collect public testimony and submit it directly into the federal record as the US Forest Service weighs potential changes to those protections. Nathan Newcomer, SEACC’s Tongass campaigner, said the group stepped in after learning the Forest Service had no plans to hold its own public meetings. …The Forest Service is expected to publish a draft environmental impact statement on the roadless rule — a step that would open a formal public comment period. Newcomer said that the window is expected to last 30 days and could begin as soon as late April. The U.S. Department of Agriculture’s Agricultural Marketing Service (AMS) announced the launch of an innovative new tool, the

The U.S. Department of Agriculture’s Agricultural Marketing Service (AMS) announced the launch of an innovative new tool, the  As the Trump administration wages war on Iran, it’s citing national security to seek an exemption from the Endangered Species Act for expanded oil and gas drilling in the Gulf of Mexico — a move alarming environmental groups who say it could set a dangerous precedent for future fossil fuel projects. Environmentalists argue the government hasn’t followed proper procedure and they’re seeking to block the move before Interior Secretary Doug Burgum convenes the Endangered Species Committee on Tuesday. The committee, nicknamed the “God Squad” by groups who say it can determine the fate of a species, is comprised of six high-ranking federal officials plus a representative for states involved. …The Center for Biological Diversity sued last week to block the committee meeting. …The committee was established in 1978 as a way to exempt projects from the Endangered Species Act. …The committee has only convened three times in its 53-year history and issued only two exemptions.

As the Trump administration wages war on Iran, it’s citing national security to seek an exemption from the Endangered Species Act for expanded oil and gas drilling in the Gulf of Mexico — a move alarming environmental groups who say it could set a dangerous precedent for future fossil fuel projects. Environmentalists argue the government hasn’t followed proper procedure and they’re seeking to block the move before Interior Secretary Doug Burgum convenes the Endangered Species Committee on Tuesday. The committee, nicknamed the “God Squad” by groups who say it can determine the fate of a species, is comprised of six high-ranking federal officials plus a representative for states involved. …The Center for Biological Diversity sued last week to block the committee meeting. …The committee was established in 1978 as a way to exempt projects from the Endangered Species Act. …The committee has only convened three times in its 53-year history and issued only two exemptions.