![]() NEW YORK, NY — Mercer International reported second quarter 2026 Operating EBITDA of negative $21.0 million, a decrease from negative $20.9 million in the same quarter of 2025 and positive $7.8 million in the first quarter of 2026. In the second quarter of 2026, net loss was $76.0 million compared to $86.1 million in the same quarter of 2025 and $52.0 million in the first quarter of 2026. Mr. Juan Carlos Bueno, Chief Executive Officer, stated: “Our pulp sales realizations remained steady this quarter, as continued economic uncertainty delayed market recovery. Our second quarter results were also weighed down by rising European fiber costs, driven by regional supply shortages and intense competition for sawmill residuals from energy producers. As a result, we recognized a non-cash impairment of $29.0 million primarily against pulp and fiber inventory.

NEW YORK, NY — Mercer International reported second quarter 2026 Operating EBITDA of negative $21.0 million, a decrease from negative $20.9 million in the same quarter of 2025 and positive $7.8 million in the first quarter of 2026. In the second quarter of 2026, net loss was $76.0 million compared to $86.1 million in the same quarter of 2025 and $52.0 million in the first quarter of 2026. Mr. Juan Carlos Bueno, Chief Executive Officer, stated: “Our pulp sales realizations remained steady this quarter, as continued economic uncertainty delayed market recovery. Our second quarter results were also weighed down by rising European fiber costs, driven by regional supply shortages and intense competition for sawmill residuals from energy producers. As a result, we recognized a non-cash impairment of $29.0 million primarily against pulp and fiber inventory.

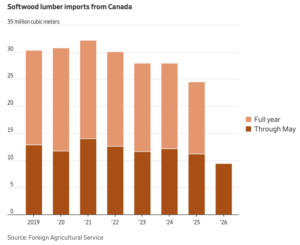

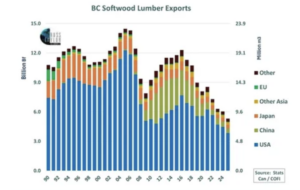

The United States’ share of Canada’s softwood lumber exports fell by 1 percentage point to 89% in January-June 2026. Canada exported 13.2 million m3, down 12%, while export value fell 26% to $2.45 billion and the average price declined 16% to $186 per m3. …Shipments to the US fell 13% to 11.7 million m3, a reduction of 1.73 million m3 from a year earlier. Export value dropped 29% to $2.02 billion, and the average price fell 18% to $172 per m3. The listed destinations with higher shipments added 77 thousand m3, equal to about 4% of the US shortfall. Declines in Japan, the Philippines, Germany and the remaining destinations totaled 128 thousand m3, leaving total non-U.S. exports down 51 thousand m3, or 3%, at 1.50 million m3. China remained Canada’s second-largest market with a 4% share. Shipments rose 3% to 525 thousand m3. Japan ranked third with a 3% share, but shipments fell 19% to 373 thousand m3. Taiwan accounted for 1.4%, the Philippines retained a 0.8% share, Mexico rose to 49 thousand m3,Germany received 33 thousand m3.

The United States’ share of Canada’s softwood lumber exports fell by 1 percentage point to 89% in January-June 2026. Canada exported 13.2 million m3, down 12%, while export value fell 26% to $2.45 billion and the average price declined 16% to $186 per m3. …Shipments to the US fell 13% to 11.7 million m3, a reduction of 1.73 million m3 from a year earlier. Export value dropped 29% to $2.02 billion, and the average price fell 18% to $172 per m3. The listed destinations with higher shipments added 77 thousand m3, equal to about 4% of the US shortfall. Declines in Japan, the Philippines, Germany and the remaining destinations totaled 128 thousand m3, leaving total non-U.S. exports down 51 thousand m3, or 3%, at 1.50 million m3. China remained Canada’s second-largest market with a 4% share. Shipments rose 3% to 525 thousand m3. Japan ranked third with a 3% share, but shipments fell 19% to 373 thousand m3. Taiwan accounted for 1.4%, the Philippines retained a 0.8% share, Mexico rose to 49 thousand m3,Germany received 33 thousand m3.

Home sales are slumping, renovation spending is losing steam and yet lumber prices have risen this summer to their highest level in four years. Back in 2022, the price of two-by-fours was falling back to earth after a record-setting spike during Covid. …This time around, reduced supply rather than unyielding demand has driven lumber prices higher. Imports are down due to steep duties on Canadian boards and President Trump’s 10% softwood lumber tariff. Meanwhile, low prices last year prompted sawmill curtailments and closures from BC to northern Florida. …Home builders… say the run-up in prices has become a headwind and will filter through to the cost of houses. Yet lumber futures, which are down about 12% from their high in late July, suggest that wood prices may have peaked for this year. …“I don’t anticipate that those mills that have been shut down are going to come back,” said Weyerhaeuser CEO Devin Stockfish. [to access the full story a WSJ subscription is required]

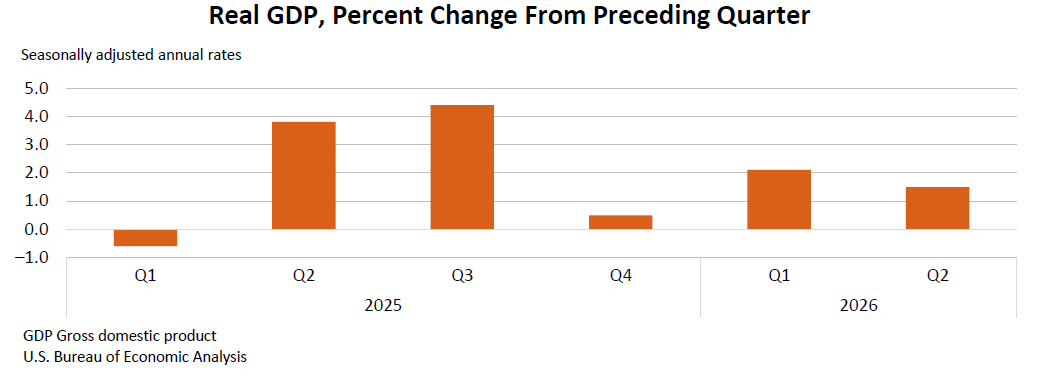

Home sales are slumping, renovation spending is losing steam and yet lumber prices have risen this summer to their highest level in four years. Back in 2022, the price of two-by-fours was falling back to earth after a record-setting spike during Covid. …This time around, reduced supply rather than unyielding demand has driven lumber prices higher. Imports are down due to steep duties on Canadian boards and President Trump’s 10% softwood lumber tariff. Meanwhile, low prices last year prompted sawmill curtailments and closures from BC to northern Florida. …Home builders… say the run-up in prices has become a headwind and will filter through to the cost of houses. Yet lumber futures, which are down about 12% from their high in late July, suggest that wood prices may have peaked for this year. …“I don’t anticipate that those mills that have been shut down are going to come back,” said Weyerhaeuser CEO Devin Stockfish. [to access the full story a WSJ subscription is required] Canada’s economy showed signs of growth in the second quarter of 2026, but uncertainty from U.S. trade policies and the war in Iran means monetary policy must remain nimble, the Bank of Canada’s governing council said during deliberations preceding its July 15 interest rate decision. A summary of deliberations that led to the council’s decision to hold interest rates steady at 2.25 per cent shows that members discussed Canada’s sluggish economy. Gross domestic product had not grown between the first quarter of 2025 and the first quarter of 2026, members said, and the heightened uncertainty around tariffs and the Canada–U.S.–Mexico (CUSMA) agreement had kept the economy in excess supply. However, members noted recent indicators that showed the economy was recovering in the second quarter of 2026 after it adjusted to the U.S. tariffs and geopolitical turbulence, and the growth was broadening instead of relying on strong consumer and government spending.

Canada’s economy showed signs of growth in the second quarter of 2026, but uncertainty from U.S. trade policies and the war in Iran means monetary policy must remain nimble, the Bank of Canada’s governing council said during deliberations preceding its July 15 interest rate decision. A summary of deliberations that led to the council’s decision to hold interest rates steady at 2.25 per cent shows that members discussed Canada’s sluggish economy. Gross domestic product had not grown between the first quarter of 2025 and the first quarter of 2026, members said, and the heightened uncertainty around tariffs and the Canada–U.S.–Mexico (CUSMA) agreement had kept the economy in excess supply. However, members noted recent indicators that showed the economy was recovering in the second quarter of 2026 after it adjusted to the U.S. tariffs and geopolitical turbulence, and the growth was broadening instead of relying on strong consumer and government spending. Canadian wildfires are driving up the price of wood products that the US construction industry depends on — with knock-on effects on housing. Western Spruce Pine Fir futures were selling for $653 per thousand board feet in late July, not far off last year’s high, and up from a low of $524 in late January. The 937 wildfires threatening forests throughout BC are driving that increase. Alex Strong at the NAHB, said President Trump’s proposed 50% tariff on Canadian goods is adding to uncertainty around the supply chain. Set to take effect Aug. 19, the 50% tariffs would directly apply to Canadian plywood, fiberboard and other wood-derived products used in homebuilding. Canada is one of the top suppliers of fiberboard to the US. Derek Nighbor, CEO of FPAC, said that the country is also America’s third-largest supplier of plywood. …The US Congress Joint Economic Committee warned that Trump’s tariffs on a range of materials could increase building costs by $10,900 per home.

Canadian wildfires are driving up the price of wood products that the US construction industry depends on — with knock-on effects on housing. Western Spruce Pine Fir futures were selling for $653 per thousand board feet in late July, not far off last year’s high, and up from a low of $524 in late January. The 937 wildfires threatening forests throughout BC are driving that increase. Alex Strong at the NAHB, said President Trump’s proposed 50% tariff on Canadian goods is adding to uncertainty around the supply chain. Set to take effect Aug. 19, the 50% tariffs would directly apply to Canadian plywood, fiberboard and other wood-derived products used in homebuilding. Canada is one of the top suppliers of fiberboard to the US. Derek Nighbor, CEO of FPAC, said that the country is also America’s third-largest supplier of plywood. …The US Congress Joint Economic Committee warned that Trump’s tariffs on a range of materials could increase building costs by $10,900 per home.

Two numbers describe President Trump’s new tariffs on Canada, and they point in opposite directions. 50% is the rate, imposed Monday under Section 338 of the Tariff Act. 2.5% is the effect. The Hub‘s reporting on the proclamations puts the affected goods at roughly 5.5% of Canadian exports now crossing the border duty-free. Weight the new duties by those trade flows and Canada’s average effective tariff rate rises by about 2.5 percentage points, pushing the blended rate toward 10%. The composition of the list reinforces the arithmetic. …Before this round, Canada faced the lowest overall tariff rate of any US trading partner—roughly 6% weighted by 2024 trade flows. Even after the duties take effect in mid-August, Canada remains among the least-tariffed economies selling into the American market. …At the level of the firm, the damage is real and concentrated. …At the level of the national economy, the needle barely moves. Both readings are true simultaneously.

Two numbers describe President Trump’s new tariffs on Canada, and they point in opposite directions. 50% is the rate, imposed Monday under Section 338 of the Tariff Act. 2.5% is the effect. The Hub‘s reporting on the proclamations puts the affected goods at roughly 5.5% of Canadian exports now crossing the border duty-free. Weight the new duties by those trade flows and Canada’s average effective tariff rate rises by about 2.5 percentage points, pushing the blended rate toward 10%. The composition of the list reinforces the arithmetic. …Before this round, Canada faced the lowest overall tariff rate of any US trading partner—roughly 6% weighted by 2024 trade flows. Even after the duties take effect in mid-August, Canada remains among the least-tariffed economies selling into the American market. …At the level of the firm, the damage is real and concentrated. …At the level of the national economy, the needle barely moves. Both readings are true simultaneously. West Fraser, North America’s top lumber producer, is taking a hit from President Trump’s latest round of tariffs on Canada. Its stock is one of the day’s worst performers among forest and building-products shares. The BC company that has sawmills and other wood-products facilities on both sides of the border is already contending with Trump’s 10% national-security tariff on lumber as well as the long-standing duties on Canadian softwood exports. The 50% tariffs Trump announced exempt softwood lumber but include plywood and specialty engineered wood products. West Fraser’s exposure should be minimal because most of its products slated for the 50% levy are sold in Canada, according to TD Cowen analysts. They estimate that just 1% of West Fraser’s aggregate sales would be exposed. And that is assuming that the tariffs stick. [to access the full story a WSJ subscription is required]

West Fraser, North America’s top lumber producer, is taking a hit from President Trump’s latest round of tariffs on Canada. Its stock is one of the day’s worst performers among forest and building-products shares. The BC company that has sawmills and other wood-products facilities on both sides of the border is already contending with Trump’s 10% national-security tariff on lumber as well as the long-standing duties on Canadian softwood exports. The 50% tariffs Trump announced exempt softwood lumber but include plywood and specialty engineered wood products. West Fraser’s exposure should be minimal because most of its products slated for the 50% levy are sold in Canada, according to TD Cowen analysts. They estimate that just 1% of West Fraser’s aggregate sales would be exposed. And that is assuming that the tariffs stick. [to access the full story a WSJ subscription is required] RUSS TAYLOR provided the latest quarterly report from the

RUSS TAYLOR provided the latest quarterly report from the

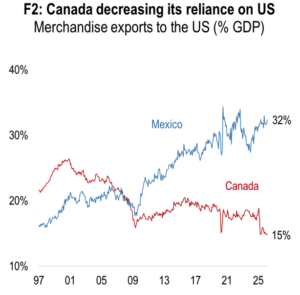

The US has formally declined to renew the USMCA trade agreement for a further 16 years. While existing tariff-free trade terms will continue, the decision triggers annual reviews until the agreement expires in 10 years. President Trump openly views the agreement as detrimental to US manufacturing, placing the burden of concessions firmly on Mexico and Canada. But as today’s chart shows, Canada has a much lower reliance on the US than Mexico, and the Carney administration is taking active steps to diversify its export base further. Exports from industrial sectors subject to tariffs – metals and auto – have fallen sharply, but the hit to activity is limited, as these account for just 2.5% of GDP. …Adjusted for a shrinking working-age population, production in these sectors has picked up. …Goods exports to the US make up close to one-third of Mexico’s GDP. Canada’s share is also high at 15%, but has fallen over time.

The US has formally declined to renew the USMCA trade agreement for a further 16 years. While existing tariff-free trade terms will continue, the decision triggers annual reviews until the agreement expires in 10 years. President Trump openly views the agreement as detrimental to US manufacturing, placing the burden of concessions firmly on Mexico and Canada. But as today’s chart shows, Canada has a much lower reliance on the US than Mexico, and the Carney administration is taking active steps to diversify its export base further. Exports from industrial sectors subject to tariffs – metals and auto – have fallen sharply, but the hit to activity is limited, as these account for just 2.5% of GDP. …Adjusted for a shrinking working-age population, production in these sectors has picked up. …Goods exports to the US make up close to one-third of Mexico’s GDP. Canada’s share is also high at 15%, but has fallen over time.

The Canadian lumber industry saw enormous price spikes during the pandemic years of 2020-2022, with costs close to triple what they are today for some products. … “We saw prices skyrocket during COVID, but so too did the cost to operate,” said Aspen Dudzic, the Alberta Forest Products Assocation’s communications director. “And interestingly, post-COVID, we saw the market prices for lumber go down, but the costs to operate have not come down in the same way.” Even though lumber costs have seen a huge drop in prices in a vacuum, why haven’t these cost savings been passed on to the consumer? …“The supply chain is really complex,” Dudzic said. “Nothing we do operates in a vacuum, so there’s a lot of other compounding costs that we have to look at, like inflationary pressures, upticks in fuel and energy prices. …Top of mind is the ongoing trade war with the US.

The Canadian lumber industry saw enormous price spikes during the pandemic years of 2020-2022, with costs close to triple what they are today for some products. … “We saw prices skyrocket during COVID, but so too did the cost to operate,” said Aspen Dudzic, the Alberta Forest Products Assocation’s communications director. “And interestingly, post-COVID, we saw the market prices for lumber go down, but the costs to operate have not come down in the same way.” Even though lumber costs have seen a huge drop in prices in a vacuum, why haven’t these cost savings been passed on to the consumer? …“The supply chain is really complex,” Dudzic said. “Nothing we do operates in a vacuum, so there’s a lot of other compounding costs that we have to look at, like inflationary pressures, upticks in fuel and energy prices. …Top of mind is the ongoing trade war with the US. BC has seen lower timber harvests and lumber and lumber exports. …BC exported 2.5 million m3 of softwood logs in 2025, a trend that has been in place since 2022. …BC lumber exports have always focused on the US market, with 64% of production and 76% of total exports directed at the US in 2025. But with US duties and tariffs totalling over 45%. the volumes started to drop in 2025 Q4. Total BC lumber exports in 2025 were 5.1 billion bf, a drop of 12% from 2024. Lumber exports to the US were 3.83 billion bf in 2025, a drop of 14.3% from 2024. …In the first quarter of 2026, total BC lumber exports were lower by 20.1% compared to 2025 Q1, with exports to the US down by a whopping 24.7% (the bite of US duties and tariffs is evident), lower to Japan by 17.7% but higher to China by 10%. It will be challenging for BC mills in export markets for much of 2026 unless demand improves or prices move higher—both unlikely until 2027.

BC has seen lower timber harvests and lumber and lumber exports. …BC exported 2.5 million m3 of softwood logs in 2025, a trend that has been in place since 2022. …BC lumber exports have always focused on the US market, with 64% of production and 76% of total exports directed at the US in 2025. But with US duties and tariffs totalling over 45%. the volumes started to drop in 2025 Q4. Total BC lumber exports in 2025 were 5.1 billion bf, a drop of 12% from 2024. Lumber exports to the US were 3.83 billion bf in 2025, a drop of 14.3% from 2024. …In the first quarter of 2026, total BC lumber exports were lower by 20.1% compared to 2025 Q1, with exports to the US down by a whopping 24.7% (the bite of US duties and tariffs is evident), lower to Japan by 17.7% but higher to China by 10%. It will be challenging for BC mills in export markets for much of 2026 unless demand improves or prices move higher—both unlikely until 2027.

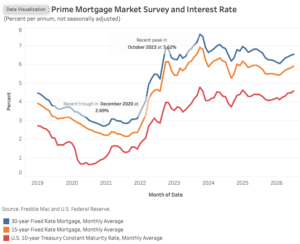

Re-escalation of the conflict in Iran pushed mortgage rates higher in July. According to Freddie Mac, the 30-year fixed-rate mortgage averaged 6.54% in July, up 5 basis points (bps) over June. Since the conflict in the Middle East began, the 30-year mortgage rate has climbed by almost 50 bps. The average 15-year rate averaged 5.91% in July, up 9 bps from June, and up 48 basis points since the end of February. Compared to a year ago, the 30-year rate remains lower by 18 bps, however, the 15-year rate is now higher by 5 bps. The 10-year Treasury yield, a key benchmark for long-term borrowing, rose 10 bps to an average of 4.58% in July as renewed attacks in the Strait of Hormuz heightened concerns about energy supplies and inflation. The yield rose sharply, ending July at 4.67%, 23 bps above its June closing level.

Re-escalation of the conflict in Iran pushed mortgage rates higher in July. According to Freddie Mac, the 30-year fixed-rate mortgage averaged 6.54% in July, up 5 basis points (bps) over June. Since the conflict in the Middle East began, the 30-year mortgage rate has climbed by almost 50 bps. The average 15-year rate averaged 5.91% in July, up 9 bps from June, and up 48 basis points since the end of February. Compared to a year ago, the 30-year rate remains lower by 18 bps, however, the 15-year rate is now higher by 5 bps. The 10-year Treasury yield, a key benchmark for long-term borrowing, rose 10 bps to an average of 4.58% in July as renewed attacks in the Strait of Hormuz heightened concerns about energy supplies and inflation. The yield rose sharply, ending July at 4.67%, 23 bps above its June closing level.

The average long-term U.S. mortgage rate climbed this week to its highest level in nearly 12 months, pushing up borrowing costs for prospective homebuyers at a time when

The average long-term U.S. mortgage rate climbed this week to its highest level in nearly 12 months, pushing up borrowing costs for prospective homebuyers at a time when  Congress’ historic effort to boost the nation’s housing supply passed both chambers with overwhelming bipartisan support and became law earlier this month. It also left a mountain of paperwork for Washington’s significantly shrunken federal agencies, which are now tasked with turning dozens of new policies into reality. Some of the lawmakers who pushed for the law worry that the Department of Housing and Urban Development — which has shed more than 30% of its core policy workforce in just three years following budget cuts — is too understaffed to quickly issue new rules and implement its provisions, aimed at making building and buying homes cheaper and easier. HUD Secretary Scott Turner is “up to the task, but you’ve got to have the underlying organization to get it done,” Sen. Thom Tillis (R-N.C.) told reporters. …HUD’s budget estimates show the offices that run the department’s programs shed more than 1,800 staff since 2023.

Congress’ historic effort to boost the nation’s housing supply passed both chambers with overwhelming bipartisan support and became law earlier this month. It also left a mountain of paperwork for Washington’s significantly shrunken federal agencies, which are now tasked with turning dozens of new policies into reality. Some of the lawmakers who pushed for the law worry that the Department of Housing and Urban Development — which has shed more than 30% of its core policy workforce in just three years following budget cuts — is too understaffed to quickly issue new rules and implement its provisions, aimed at making building and buying homes cheaper and easier. HUD Secretary Scott Turner is “up to the task, but you’ve got to have the underlying organization to get it done,” Sen. Thom Tillis (R-N.C.) told reporters. …HUD’s budget estimates show the offices that run the department’s programs shed more than 1,800 staff since 2023.

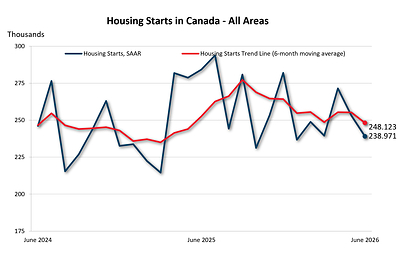

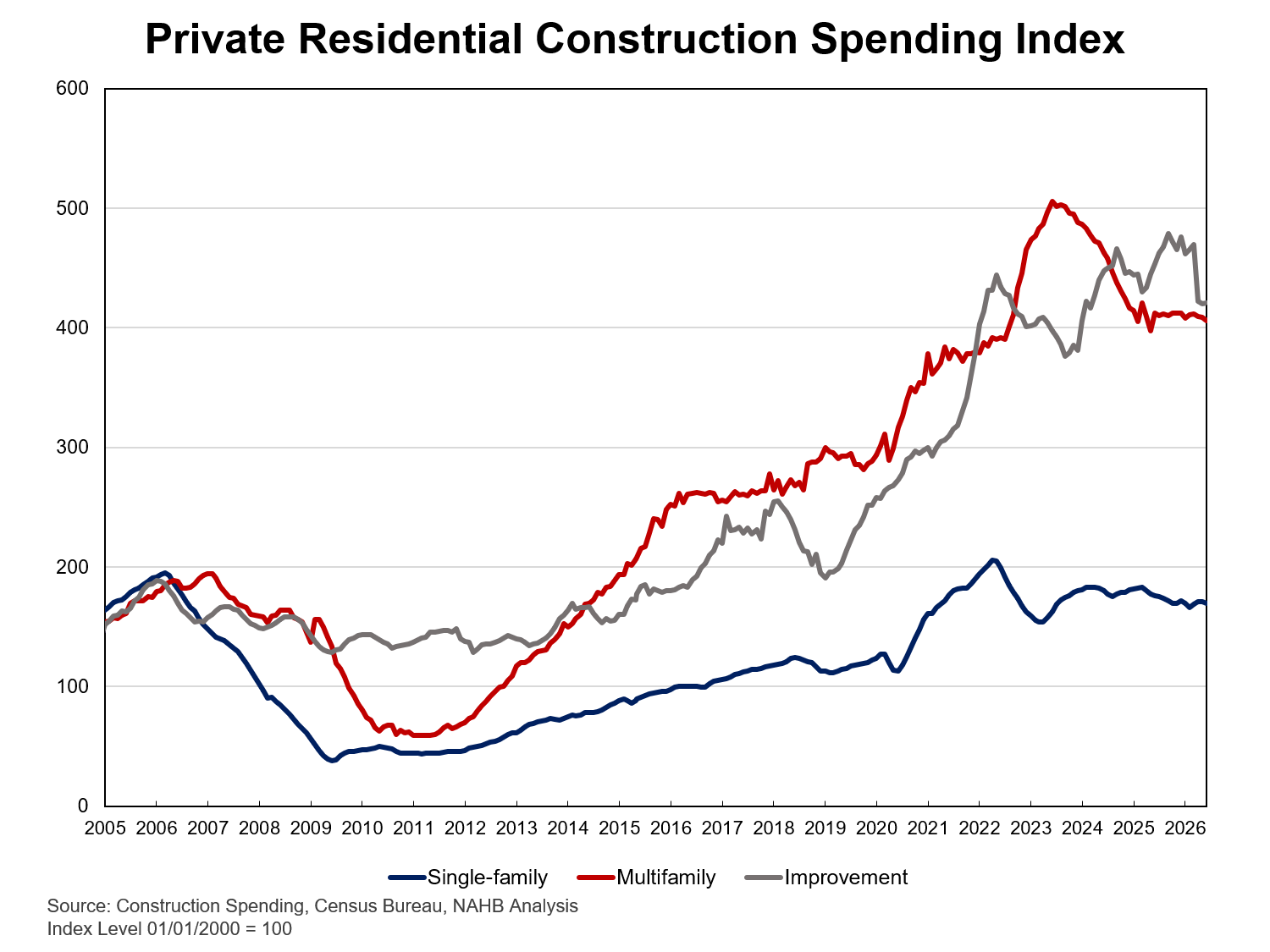

US single-family homebuilding and permits for future construction fell in June, weighed down by higher mortgage rates and inventory of unsold new homes on the market. Single-family housing starts, which account for the bulk of homebuilding, slipped 0.2% to a seasonally adjusted annual rate of 895,000 units. Single-family homebuilding dropped 3.2% year-on-year in June. Permits for future construction of single-family homes dropped 2.4% last month to a rate of 871,000 units. They fell 0.2% year-on-year in June. The rate on the popular 30-year fixed-mortgage has increased by nearly 60 basis points since the US and Israel attacked Iran at the end of February. …Building permits for multi-family housing projects dropped 4.9% to a rate of 445,000 units last month. Overall building permits fell 3.0% to a rate of 1.367 million units. They declined 2.3% year-on-year in June.

US single-family homebuilding and permits for future construction fell in June, weighed down by higher mortgage rates and inventory of unsold new homes on the market. Single-family housing starts, which account for the bulk of homebuilding, slipped 0.2% to a seasonally adjusted annual rate of 895,000 units. Single-family homebuilding dropped 3.2% year-on-year in June. Permits for future construction of single-family homes dropped 2.4% last month to a rate of 871,000 units. They fell 0.2% year-on-year in June. The rate on the popular 30-year fixed-mortgage has increased by nearly 60 basis points since the US and Israel attacked Iran at the end of February. …Building permits for multi-family housing projects dropped 4.9% to a rate of 445,000 units last month. Overall building permits fell 3.0% to a rate of 1.367 million units. They declined 2.3% year-on-year in June.

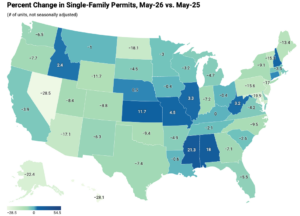

State-level permitting activity continued to reflect a divided housing market through the first five months of 2026. Elevated mortgage rates and ongoing affordability challenges continued to weigh on single-family construction across much of the country, while multifamily permitting remained comparatively stronger, supported by gains in several regions despite continued weakness in parts of the South. Over the first five months of the year, the number of single-family permits issued nationwide reached 380,130. Compared with the same period in 2025, this represents a 6.1 percent decline compared with the May 2025 total of 404,977. In contrast, multifamily permitting activity remained stronger, with 208,192 permits issued nationwide, marking a 6.5 percent increase from the same period last year.

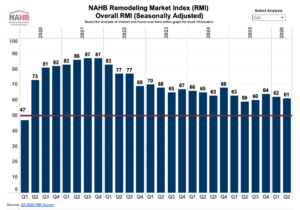

State-level permitting activity continued to reflect a divided housing market through the first five months of 2026. Elevated mortgage rates and ongoing affordability challenges continued to weigh on single-family construction across much of the country, while multifamily permitting remained comparatively stronger, supported by gains in several regions despite continued weakness in parts of the South. Over the first five months of the year, the number of single-family permits issued nationwide reached 380,130. Compared with the same period in 2025, this represents a 6.1 percent decline compared with the May 2025 total of 404,977. In contrast, multifamily permitting activity remained stronger, with 208,192 permits issued nationwide, marking a 6.5 percent increase from the same period last year. In the second quarter of 2026, the NAHB Remodeling Market Index (RMI) posted a reading of 61, down one point compared to the previous quarter. The RMI has remained in the low 60s consistently over the past year. Even with this slight decline from the previous quarter, remodeler sentiment remains the standout sector within the housing industry, outperforming both its single-family and multifamily counterparts. …However, ongoing economic uncertainty and current cost pressures due to inflation are causing project delays, especially for larger ones. In the latest RMI survey, 74% of remodelers reported that their suppliers have increased prices of materials since March due to higher fuel costs, with the average increase in materials prices over that span being 6.7%.

In the second quarter of 2026, the NAHB Remodeling Market Index (RMI) posted a reading of 61, down one point compared to the previous quarter. The RMI has remained in the low 60s consistently over the past year. Even with this slight decline from the previous quarter, remodeler sentiment remains the standout sector within the housing industry, outperforming both its single-family and multifamily counterparts. …However, ongoing economic uncertainty and current cost pressures due to inflation are causing project delays, especially for larger ones. In the latest RMI survey, 74% of remodelers reported that their suppliers have increased prices of materials since March due to higher fuel costs, with the average increase in materials prices over that span being 6.7%. The U.S. goods trade deficit is widening, the Commerce Department said Friday, suggesting stockpiling ahead of higher tariffs and a continued reliance on imports for the domestic data center rollout, analysts say. The goods trade deficit for May jumped more than $20 billion to $105.8 billion, up from $83 billion in April, according to

The U.S. goods trade deficit is widening, the Commerce Department said Friday, suggesting stockpiling ahead of higher tariffs and a continued reliance on imports for the domestic data center rollout, analysts say. The goods trade deficit for May jumped more than $20 billion to $105.8 billion, up from $83 billion in April, according to

Drax’s Pellet Production adjusted EBITDA fell 14% to £64 million in the first half of 2026 from £74 million a year earlier, as production declined and internal sales prices fell. Pellet output decreased to 1.9 million metric tons from 2.1 million metric tons, according to Drax Group. The lower production reflected the closure of the Williams Lake pellet plant in Canada and outages at facilities in the U.S. South. Drax also weighted more production toward the second half of 2026 to align pellet supply with expected generation at Drax Power Station. Market conditions affected the Canadian business through limited fibre availability and lower margins. Canadian operations otherwise performed well during the period, while Drax continued a strategic review of the business. Cost reductions in the U.S. South also lowered Pellet Production earnings under Drax’s cost-plus transfer-pricing system.

Drax’s Pellet Production adjusted EBITDA fell 14% to £64 million in the first half of 2026 from £74 million a year earlier, as production declined and internal sales prices fell. Pellet output decreased to 1.9 million metric tons from 2.1 million metric tons, according to Drax Group. The lower production reflected the closure of the Williams Lake pellet plant in Canada and outages at facilities in the U.S. South. Drax also weighted more production toward the second half of 2026 to align pellet supply with expected generation at Drax Power Station. Market conditions affected the Canadian business through limited fibre availability and lower margins. Canadian operations otherwise performed well during the period, while Drax continued a strategic review of the business. Cost reductions in the U.S. South also lowered Pellet Production earnings under Drax’s cost-plus transfer-pricing system.

The economic situation of the German sawmilling and timber industry remains strained, according to the latest report from the German Sawmill and Timber Industry Association (DESH). Ther Berlin-based group, which represents German sawmillers, says the persistently weak construction sector, the global economic and sales crisis, high raw material and production costs, and mounting cost pressures are placing a significant burden on domestic companies. It warns of a further deterioration in the situation. In the coming weeks, DESH says many companies will be forced to scale back production capacities and extend scheduled maintenance periods. “Despite promising rhetoric from policymakers, the hoped-for recovery of the domestic construction industry has yet to materialize,” it said. “Demand for construction timber in key export markets also remains subdued due to geopolitical crises and a global economic slowdown. At the same time, persistently high costs for raw materials, energy, and production are burdening companies.

The economic situation of the German sawmilling and timber industry remains strained, according to the latest report from the German Sawmill and Timber Industry Association (DESH). Ther Berlin-based group, which represents German sawmillers, says the persistently weak construction sector, the global economic and sales crisis, high raw material and production costs, and mounting cost pressures are placing a significant burden on domestic companies. It warns of a further deterioration in the situation. In the coming weeks, DESH says many companies will be forced to scale back production capacities and extend scheduled maintenance periods. “Despite promising rhetoric from policymakers, the hoped-for recovery of the domestic construction industry has yet to materialize,” it said. “Demand for construction timber in key export markets also remains subdued due to geopolitical crises and a global economic slowdown. At the same time, persistently high costs for raw materials, energy, and production are burdening companies.

Housing starts across Japan climbed 18.6% in June for a third straight monthly rise, with the recovery missing the two-by-four segment built on imported dimension lumber, where starts fell 7.4%. That is according to data the Ministry of Land, Infrastructure, Transport and Tourism released, which shows owner-occupied, rental, and built-for-sale housing all rising, while the platform-frame trade went the other way. Economists had expected a 12.8% rise, with the stronger result still slowing sharply from May’s 33.9% surge as owner-occupied growth eased to 15.7% from 31.8, rentals to 24.6 from 33.3, and built-for-sale homes to 14.2 from 39.2. Prefab housing swung 13.7% higher after a 3.4% fall in May, leaving two-by-four as the only wooden segment in decline. None of the growth measures a strong market, because the comparison month produced just 55,956 starts, down 15.6% in a third straight fall after the April 2025 revision to the Building Standards Act.

Housing starts across Japan climbed 18.6% in June for a third straight monthly rise, with the recovery missing the two-by-four segment built on imported dimension lumber, where starts fell 7.4%. That is according to data the Ministry of Land, Infrastructure, Transport and Tourism released, which shows owner-occupied, rental, and built-for-sale housing all rising, while the platform-frame trade went the other way. Economists had expected a 12.8% rise, with the stronger result still slowing sharply from May’s 33.9% surge as owner-occupied growth eased to 15.7% from 31.8, rentals to 24.6 from 33.3, and built-for-sale homes to 14.2 from 39.2. Prefab housing swung 13.7% higher after a 3.4% fall in May, leaving two-by-four as the only wooden segment in decline. None of the growth measures a strong market, because the comparison month produced just 55,956 starts, down 15.6% in a third straight fall after the April 2025 revision to the Building Standards Act.

Softwood markets across Latin America and the Asia-Pacific are approaching a turning point, according to the latest market report from Global Wood Trends and O’Kelly Acumen. The report says some of the world’s lowest-cost plantation producers are increasingly linked to major importing markets where domestic supply growth is limited. “With harvests expected to decline in key exporting regions, China remaining structurally dependent on imports, and Japan nearing peak production, the regional supply balance is likely to tighten through 2035 – creating new risks and opportunities for producers, investors, traders, and wood consumers,” it says. The ‘Global Softwood Roundwood Supply – Latin America & Asia-Pacific’ report… says Latin America, Asia, and Oceania. Latin America remain a highly competitive source of softwood roundwood. Brazil, Chile, Argentina, and Uruguay account for nearly all regional softwood supply, supported by large-scale plantation forestry and investment by integrated forest-product companies and institutional owners.

Softwood markets across Latin America and the Asia-Pacific are approaching a turning point, according to the latest market report from Global Wood Trends and O’Kelly Acumen. The report says some of the world’s lowest-cost plantation producers are increasingly linked to major importing markets where domestic supply growth is limited. “With harvests expected to decline in key exporting regions, China remaining structurally dependent on imports, and Japan nearing peak production, the regional supply balance is likely to tighten through 2035 – creating new risks and opportunities for producers, investors, traders, and wood consumers,” it says. The ‘Global Softwood Roundwood Supply – Latin America & Asia-Pacific’ report… says Latin America, Asia, and Oceania. Latin America remain a highly competitive source of softwood roundwood. Brazil, Chile, Argentina, and Uruguay account for nearly all regional softwood supply, supported by large-scale plantation forestry and investment by integrated forest-product companies and institutional owners.  Japan’s housing starts surged 33.9% yoy in May 2026, sharply accelerating from a 11.4% increase in the previous month and marking the second straight month of expansion. It was also the fastest growth since March 2025, topping market expectations of 31.8%. Growth was broad-based across most segments, including owner-occupied homes (31.8% vs 19.5% in April), rental housing (33.3% vs 17.3%), built-for-sale housing (39.2% vs 3.4%), and two-by-four homes (24.8% vs 64.8%). In contrast, prefabricated housing fell 3.4%, swinging from a 11.1% increase in April.

Japan’s housing starts surged 33.9% yoy in May 2026, sharply accelerating from a 11.4% increase in the previous month and marking the second straight month of expansion. It was also the fastest growth since March 2025, topping market expectations of 31.8%. Growth was broad-based across most segments, including owner-occupied homes (31.8% vs 19.5% in April), rental housing (33.3% vs 17.3%), built-for-sale housing (39.2% vs 3.4%), and two-by-four homes (24.8% vs 64.8%). In contrast, prefabricated housing fell 3.4%, swinging from a 11.1% increase in April. Russia’s timber exports to China, its largest overseas market, fell sharply in the first four months of 2026 as Beijing’s prolonged property downturn weighed on demand, adding to mounting pressure on an industry already struggling with sanctions, high borrowing costs and weak profitability. Exports of Russian sawn timber to China dropped 30% year on year to 2.6 million cubic meters in January-April, while export revenue declined 26% to $603.7 million, the Vedomosti business daily reported. …China accounted for roughly half of Russia’s sawn timber exports in 2025 after Europe closed its market following Moscow’s full-scale invasion of Ukraine. But weakening Chinese construction activity, rising logistics costs and a stronger ruble have eroded demand, leaving Russian producers with fewer alternative markets. Russia’s total sawn timber exports fell 32% year-on-year to around 4 million cubic meters in the January-April period. China imported 11.2 million cubic meters of Russian sawn timber in 2025.

Russia’s timber exports to China, its largest overseas market, fell sharply in the first four months of 2026 as Beijing’s prolonged property downturn weighed on demand, adding to mounting pressure on an industry already struggling with sanctions, high borrowing costs and weak profitability. Exports of Russian sawn timber to China dropped 30% year on year to 2.6 million cubic meters in January-April, while export revenue declined 26% to $603.7 million, the Vedomosti business daily reported. …China accounted for roughly half of Russia’s sawn timber exports in 2025 after Europe closed its market following Moscow’s full-scale invasion of Ukraine. But weakening Chinese construction activity, rising logistics costs and a stronger ruble have eroded demand, leaving Russian producers with fewer alternative markets. Russia’s total sawn timber exports fell 32% year-on-year to around 4 million cubic meters in the January-April period. China imported 11.2 million cubic meters of Russian sawn timber in 2025.