![]() VANCOUVER, BC — West Fraser Timber reported their fourth quarter results of 2025. Fourth quarter sales were $1.165 billion, compared to $1.307 billion in Q3, 2025. Fourth quarter earnings were $(751) million, compared to earnings of $(204) million in Q3, 2025. Fourth quarter Adjusted EBITDA was $(79) million compared to $(144) million in Q3, 2025. Full year sales were $5.462 billion, compared to $6.174 billion in 2024. Full year earnings were $(937) million, compared to earnings of $(5) million. Full year Adjusted EBITDA was $56 million compared to $673 million in 2024. …”The fourth quarter of 2025 was another challenging period for West Fraser, marked by elevated softwood lumber duties and tariffs, southern yellow pine lumber and OSB oversupply, and tempered demand for many of our wood-based building products, much of which can be attributed to housing affordability constraints that have continued into early 2026. Notwithstanding this environment, we made great advances with some of our major capital investments,” said Sean McLaren, President and CEO.

VANCOUVER, BC — West Fraser Timber reported their fourth quarter results of 2025. Fourth quarter sales were $1.165 billion, compared to $1.307 billion in Q3, 2025. Fourth quarter earnings were $(751) million, compared to earnings of $(204) million in Q3, 2025. Fourth quarter Adjusted EBITDA was $(79) million compared to $(144) million in Q3, 2025. Full year sales were $5.462 billion, compared to $6.174 billion in 2024. Full year earnings were $(937) million, compared to earnings of $(5) million. Full year Adjusted EBITDA was $56 million compared to $673 million in 2024. …”The fourth quarter of 2025 was another challenging period for West Fraser, marked by elevated softwood lumber duties and tariffs, southern yellow pine lumber and OSB oversupply, and tempered demand for many of our wood-based building products, much of which can be attributed to housing affordability constraints that have continued into early 2026. Notwithstanding this environment, we made great advances with some of our major capital investments,” said Sean McLaren, President and CEO.

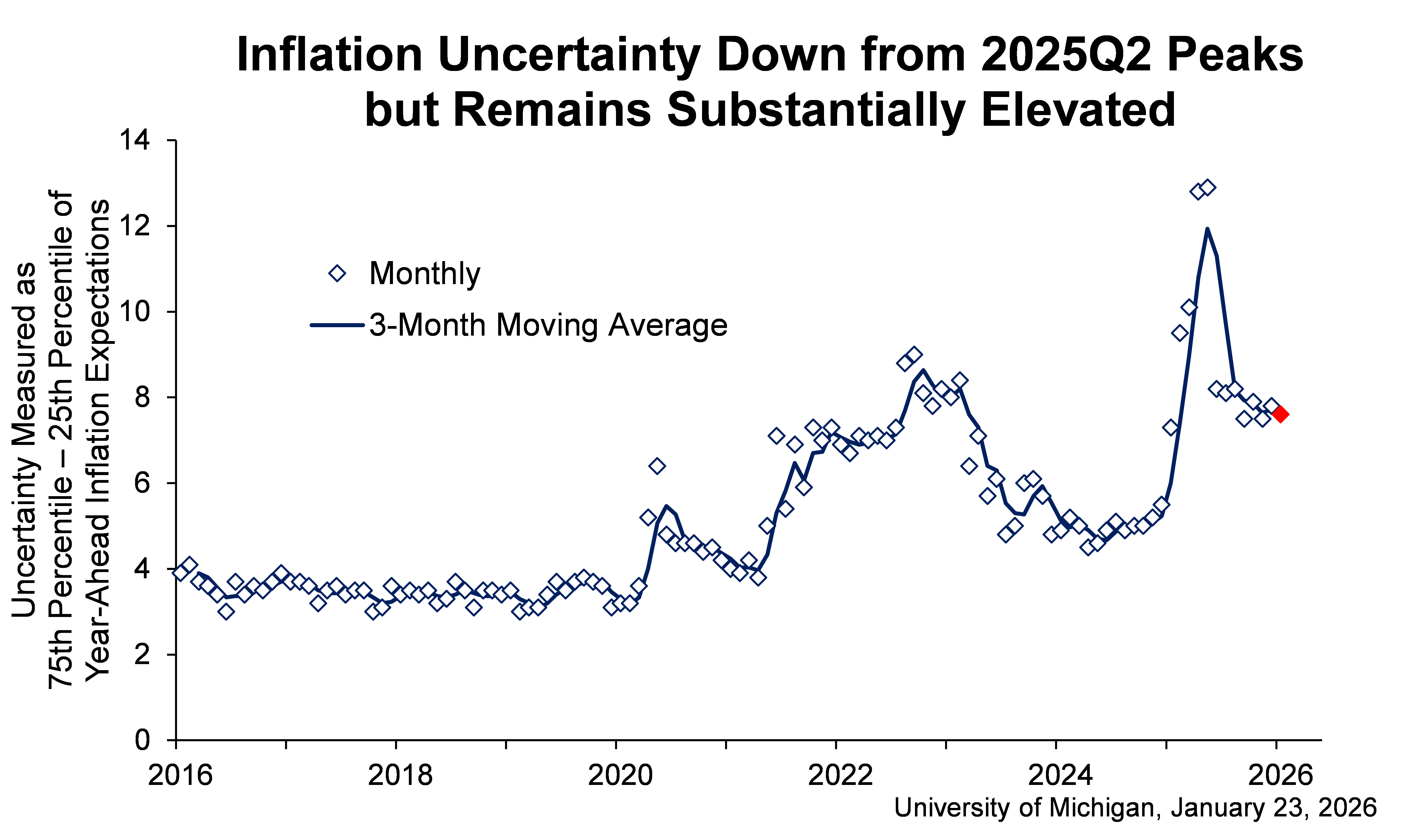

The Bank of Canada’s latest survey of financial-market participants pointed to a modestly brighter growth outlook than the central bank’s own projections, even as trade tensions with the US remain the dominant threat hanging over Canada’s economy and housing market. In the fourth‑quarter Market Participants Survey, 93% of respondents cited an “increase in trade tensions” as the top downside risk to Canadian growth, well ahead of tighter global financial conditions and weaker consumer spending. Participants still assign a 20% probability to a recession over the next six months, but their median forecast calls for real GDP growth of 1.6% by the end of 2026 and 1.9% by late 2027, slightly stronger than the Bank’s own projections of 1.1% and 1.5%. While the survey suggests some stabilization in expectations, it underscores that tariff policy remains the key macroeconomic swing factor. …PwC Canada’s latest survey among 133 CEOs showed that only 27% expect the domestic economy to improve over the next 12 months.

The Bank of Canada’s latest survey of financial-market participants pointed to a modestly brighter growth outlook than the central bank’s own projections, even as trade tensions with the US remain the dominant threat hanging over Canada’s economy and housing market. In the fourth‑quarter Market Participants Survey, 93% of respondents cited an “increase in trade tensions” as the top downside risk to Canadian growth, well ahead of tighter global financial conditions and weaker consumer spending. Participants still assign a 20% probability to a recession over the next six months, but their median forecast calls for real GDP growth of 1.6% by the end of 2026 and 1.9% by late 2027, slightly stronger than the Bank’s own projections of 1.1% and 1.5%. While the survey suggests some stabilization in expectations, it underscores that tariff policy remains the key macroeconomic swing factor. …PwC Canada’s latest survey among 133 CEOs showed that only 27% expect the domestic economy to improve over the next 12 months.

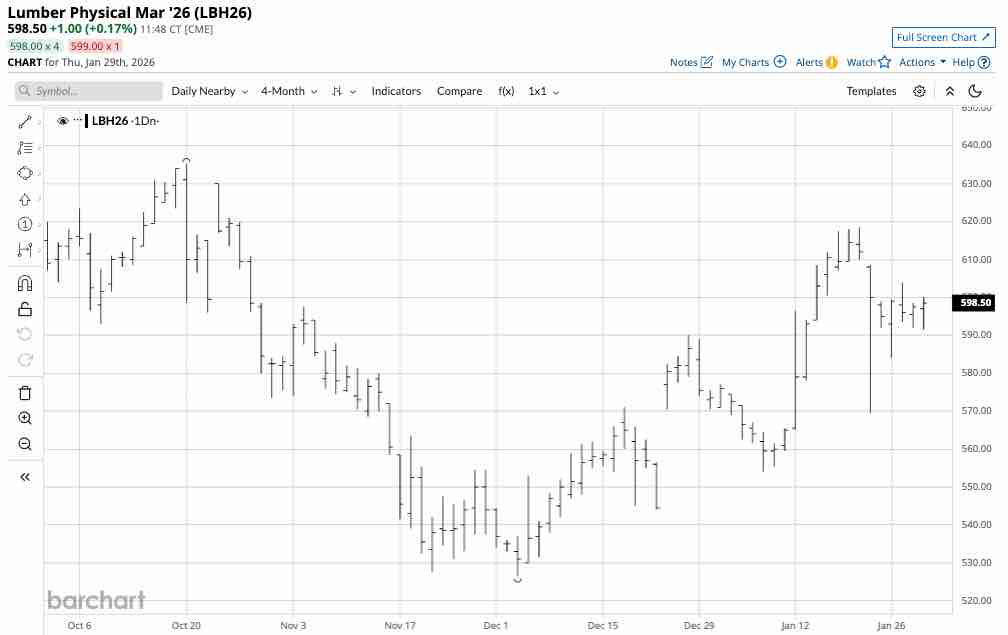

Lumber futures slipped below $590 per thousand board feet, the lowest level in nearly four weeks, as housing demand weakened and earlier restocking momentum faded. Demand softened as financing costs edged higher and housing activity cooled, with US pending home sales plunging 9.3% month on month in December 2025, removing a key source of construction and renovation related wood consumption ahead of the spring building season. At the same time, mills continued running to rebuild inventories after the winter squeeze, increasing physical availability while distributors reported quieter order books. The combination of softer demand and rising availability encouraged position unwinds after January’s rally, with falling volumes and open interest amplifying the price decline. [END]

Lumber futures slipped below $590 per thousand board feet, the lowest level in nearly four weeks, as housing demand weakened and earlier restocking momentum faded. Demand softened as financing costs edged higher and housing activity cooled, with US pending home sales plunging 9.3% month on month in December 2025, removing a key source of construction and renovation related wood consumption ahead of the spring building season. At the same time, mills continued running to rebuild inventories after the winter squeeze, increasing physical availability while distributors reported quieter order books. The combination of softer demand and rising availability encouraged position unwinds after January’s rally, with falling volumes and open interest amplifying the price decline. [END]

Canada’s housing and homelessness crisis touches nearly every Canadian. Over the past decade, while federal housing spending has increased, affordability has worsened for all but the wealthiest, and homelessness is surging. Despite recent declines in housing prices and rents, unsheltered homelessness is still up 300% since 2018, according to the most recent national point-in-time count. The country has a narrow but historic window to tackle this crisis and rebuild our housing system so it delivers at the speed, scale and affordability this moment demands. …Federal action alone won’t get us there. Provinces and territories control the planning systems, development-charge frameworks, zoning rules, supportive housing, health services and income supports. …That is why we need a Canada Housing Accord. [Tim Richter is the chief executive of the Canadian Alliance to End Homelessness and Tyler Meredith is a senior fellow at the Munk School of Global Affairs and Public Policy]

Canada’s housing and homelessness crisis touches nearly every Canadian. Over the past decade, while federal housing spending has increased, affordability has worsened for all but the wealthiest, and homelessness is surging. Despite recent declines in housing prices and rents, unsheltered homelessness is still up 300% since 2018, according to the most recent national point-in-time count. The country has a narrow but historic window to tackle this crisis and rebuild our housing system so it delivers at the speed, scale and affordability this moment demands. …Federal action alone won’t get us there. Provinces and territories control the planning systems, development-charge frameworks, zoning rules, supportive housing, health services and income supports. …That is why we need a Canada Housing Accord. [Tim Richter is the chief executive of the Canadian Alliance to End Homelessness and Tyler Meredith is a senior fellow at the Munk School of Global Affairs and Public Policy] RUSS TAYLOR provided the latest quarterly report from the

RUSS TAYLOR provided the latest quarterly report from the  MONTREAL — Tariffs and economic angst delivered a significant blow to Canadian National Railway Co. last year, as the question mark hanging over North American free trade continues to threaten profits in 2026. “Tariffs, trade uncertainty and volatility impacted our full-year 2025 revenues by over $350 million,” chief commercial officer Janet Drysdale told analysts on a conference call Friday. Forest products and metals took the biggest bruising, she said, with the two segments seeing a year-over-year revenue drop of eight and four per cent, respectively, in the latest quarter. …On top of trade uncertainty, a less publicized source of angst has rippled through the rail industry since last summer. Union Pacific Corp., the second-largest railway operator in the United States, announced in July it wants to buy Norfolk Southern Corp. in a US$85-billion deal that would create that country’s first transcontinental railway, and potentially trigger a final wave of rail mergers across North America.

MONTREAL — Tariffs and economic angst delivered a significant blow to Canadian National Railway Co. last year, as the question mark hanging over North American free trade continues to threaten profits in 2026. “Tariffs, trade uncertainty and volatility impacted our full-year 2025 revenues by over $350 million,” chief commercial officer Janet Drysdale told analysts on a conference call Friday. Forest products and metals took the biggest bruising, she said, with the two segments seeing a year-over-year revenue drop of eight and four per cent, respectively, in the latest quarter. …On top of trade uncertainty, a less publicized source of angst has rippled through the rail industry since last summer. Union Pacific Corp., the second-largest railway operator in the United States, announced in July it wants to buy Norfolk Southern Corp. in a US$85-billion deal that would create that country’s first transcontinental railway, and potentially trigger a final wave of rail mergers across North America.

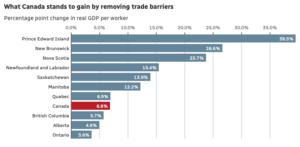

Canada’s economy could gain nearly 7%, or $210 billion, in real GDP over a gradual period by fully removing internal trade barriers between the country’s 13 provinces and territories, according to a report published Tuesday by the International Monetary Fund (IMF). On average, regulation-related barriers are the equivalent of a 9% tariff nationally, estimates the report, which was co-authored by IMF researchers Federico J. Diez and Yuanchen Yang with contributions from University of Calgary economist Trevor Tombe. …Because of the trade barriers between provinces, “Canada isn’t really one economy. It’s really 10 economies,” said Alicia Planincic, director of policy and economics at the Business Council of Alberta in Calgary. …The report points to finance, telecom, transportation and professional services as far-reaching sectors that “ripple through the economy” and raise costs for all of the businesses they touch.

Canada’s economy could gain nearly 7%, or $210 billion, in real GDP over a gradual period by fully removing internal trade barriers between the country’s 13 provinces and territories, according to a report published Tuesday by the International Monetary Fund (IMF). On average, regulation-related barriers are the equivalent of a 9% tariff nationally, estimates the report, which was co-authored by IMF researchers Federico J. Diez and Yuanchen Yang with contributions from University of Calgary economist Trevor Tombe. …Because of the trade barriers between provinces, “Canada isn’t really one economy. It’s really 10 economies,” said Alicia Planincic, director of policy and economics at the Business Council of Alberta in Calgary. …The report points to finance, telecom, transportation and professional services as far-reaching sectors that “ripple through the economy” and raise costs for all of the businesses they touch.  B.C.’s export performance moved against the national pattern in November. Domestic exports to international markets rose 7.6 per cent year over year to $4.59 billion, whereas exports nationally declined by about four per cent on a customs basis. This contrast partly reflects differences in the types of goods each region exports. Nevertheless, provincial export trends remain soft, reflecting U.S. tariffs on key products like lumber, and end of de minimis treatment of low value exports. Year-to-date, B.C. exports slipped a mild 0.1 per cent from same-period 2024, which was slightly stronger than the national reading. …That said, a declining trend continued in the battered forestry sector (-13.7 per cent year over year), where tariffs have compounded weakness from timber supply constraints and other duties already imposed by the U.S.

B.C.’s export performance moved against the national pattern in November. Domestic exports to international markets rose 7.6 per cent year over year to $4.59 billion, whereas exports nationally declined by about four per cent on a customs basis. This contrast partly reflects differences in the types of goods each region exports. Nevertheless, provincial export trends remain soft, reflecting U.S. tariffs on key products like lumber, and end of de minimis treatment of low value exports. Year-to-date, B.C. exports slipped a mild 0.1 per cent from same-period 2024, which was slightly stronger than the national reading. …That said, a declining trend continued in the battered forestry sector (-13.7 per cent year over year), where tariffs have compounded weakness from timber supply constraints and other duties already imposed by the U.S. EDMUNDSTON, New Brunswick – Acadian Timber reported financial and operating results for the three months ended December 31, 2025 as well as for the full 2025 fiscal year. “While 2025 brought a multitude of challenges, Acadian delivered steady operational performance in New Brunswick, helping to offset weather-related challenges, trucking constraints, and productivity issues in Maine,” said Adam Sheparski, President and Chief Executive Officer. …During the fourth quarter, Acadian generated sales of $22.0 million compared to $20.2 million in the fourth quarter of 2024. Acadian generated $5.2 million of Adjusted EBITDA and declared dividends of $5.3 million. During 2025, Acadian generated revenue from timber sales and services of $87.0 million, compared to $91.6 million in the prior year. The sale of 752,100 voluntary carbon credits contributed an additional $24.6 million to total sales in 2024 while no sales of carbon credits occurred in 2025.

EDMUNDSTON, New Brunswick – Acadian Timber reported financial and operating results for the three months ended December 31, 2025 as well as for the full 2025 fiscal year. “While 2025 brought a multitude of challenges, Acadian delivered steady operational performance in New Brunswick, helping to offset weather-related challenges, trucking constraints, and productivity issues in Maine,” said Adam Sheparski, President and Chief Executive Officer. …During the fourth quarter, Acadian generated sales of $22.0 million compared to $20.2 million in the fourth quarter of 2024. Acadian generated $5.2 million of Adjusted EBITDA and declared dividends of $5.3 million. During 2025, Acadian generated revenue from timber sales and services of $87.0 million, compared to $91.6 million in the prior year. The sale of 752,100 voluntary carbon credits contributed an additional $24.6 million to total sales in 2024 while no sales of carbon credits occurred in 2025.

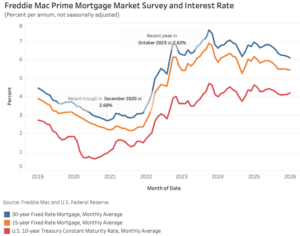

Long-term mortgage rates continued to decline in January. According to Freddie Mac, the 30-year fixed-rate mortgage averaged 6.10% last month, 9 basis points (bps) lower than December. Meanwhile, the 15-year rate declined 4 bps to 5.44%. Compared to a year ago, the 30-year rate is lower by 86 bps. The 15-year rate is also lower by 72 bps. The 10-year Treasury yield, a key benchmark for long-term borrowing, averaged 4.20% in January – an increase of 8 bps from the previous month, but remained considerably lower than last year by 43 bps. While mortgage rates typically move in tandem with the treasury yields, the spread between the two narrowed during the month. Reports that the Trump administration encouraged Fannie Mae and Freddie Mac to expand purchases of mortgage-backed securities (MBS) boosted demand for MBS, pushing mortgage rates lower. However, treasury yields rose sharply in the final week of January from global and fiscal pressures.

Long-term mortgage rates continued to decline in January. According to Freddie Mac, the 30-year fixed-rate mortgage averaged 6.10% last month, 9 basis points (bps) lower than December. Meanwhile, the 15-year rate declined 4 bps to 5.44%. Compared to a year ago, the 30-year rate is lower by 86 bps. The 15-year rate is also lower by 72 bps. The 10-year Treasury yield, a key benchmark for long-term borrowing, averaged 4.20% in January – an increase of 8 bps from the previous month, but remained considerably lower than last year by 43 bps. While mortgage rates typically move in tandem with the treasury yields, the spread between the two narrowed during the month. Reports that the Trump administration encouraged Fannie Mae and Freddie Mac to expand purchases of mortgage-backed securities (MBS) boosted demand for MBS, pushing mortgage rates lower. However, treasury yields rose sharply in the final week of January from global and fiscal pressures.  When it comes to housing affordability, the logic of “build build build” is straightforward enough: Housing is too expensive. If there were more of it, prices would fall. …Homebuilders are even pushing a plan for a million new affordable houses. …Unfortunately, it’s not that simple. The problem of housing affordability is much bigger than insufficient supply; it’s a mismatch with demand. And that demand is driven by income inequality that has seen soaring income growth at the top and tepid growth (or even stagnation) in the middle. In other words: The way to improve housing affordability is to reduce income inequality. …What’s needed are policies that increase income for households at the bottom and middle. Rather than boosting the housing supply in the hope that they benefit, the answer is to fix the labor market to make sure that they do.

When it comes to housing affordability, the logic of “build build build” is straightforward enough: Housing is too expensive. If there were more of it, prices would fall. …Homebuilders are even pushing a plan for a million new affordable houses. …Unfortunately, it’s not that simple. The problem of housing affordability is much bigger than insufficient supply; it’s a mismatch with demand. And that demand is driven by income inequality that has seen soaring income growth at the top and tepid growth (or even stagnation) in the middle. In other words: The way to improve housing affordability is to reduce income inequality. …What’s needed are policies that increase income for households at the bottom and middle. Rather than boosting the housing supply in the hope that they benefit, the answer is to fix the labor market to make sure that they do.  The United States is one of the world’s largest timberland investment markets, with returns driven primarily by land values rather than timber prices, according to Domain Timber Advisors’ timberland market analysis. Timberland values remain strong at the end of 2025, supported by continued appreciation in land values, while timber prices remain relatively flat. …During 2025, Domain underwrites 14 institutional bid events, 54 public listings, and 38 off-market or non-public offerings. By the end of the fourth quarter, the acquisition pipeline consists of 46 deals covering more than 500 thousand acres, providing visibility into pricing dynamics, regional demand shifts, and emerging non-timber value drivers. …Looking ahead, Domain states that renewable energy development and technology infrastructure are expected to expand non-timber revenue opportunities in 2026 and beyond. Alternative timber product markets, including molded fiber products and biomass-to-electricity, are expected to offset part of the pulpwood demand lost due to mill closures and production quotas.

The United States is one of the world’s largest timberland investment markets, with returns driven primarily by land values rather than timber prices, according to Domain Timber Advisors’ timberland market analysis. Timberland values remain strong at the end of 2025, supported by continued appreciation in land values, while timber prices remain relatively flat. …During 2025, Domain underwrites 14 institutional bid events, 54 public listings, and 38 off-market or non-public offerings. By the end of the fourth quarter, the acquisition pipeline consists of 46 deals covering more than 500 thousand acres, providing visibility into pricing dynamics, regional demand shifts, and emerging non-timber value drivers. …Looking ahead, Domain states that renewable energy development and technology infrastructure are expected to expand non-timber revenue opportunities in 2026 and beyond. Alternative timber product markets, including molded fiber products and biomass-to-electricity, are expected to offset part of the pulpwood demand lost due to mill closures and production quotas.

Russia’s lumber industry is entering a period of sustained pressure as production volumes continue to fall and regulatory risks increase. Official data shows that lumber output declined by more than 2.5% last year, reinforcing concerns across the forestry and wood processing sectors. According to Rosstat, Russia’s lumber production dropped from 29.2 million cubic metres in 2024 to 28.48 million cubic metres in 2025. Output remains well below historical highs. Current production is estimated to be 2 to 3 million cubic metres lower than the 2019 peak of roughly 32 million cubic metres. The downturn reflects structural challenges rather than short-term disruption. Domestic demand has weakened. Export markets have narrowed. Access to European machinery and technology has been reduced. These pressures are being felt across both logging and downstream processing operations. China now absorbs more than 70% of Russia’s lumber exports. …Softwood lumber production fell by 3.5% last year. Output declined to 25.7 million cubic metres.

Russia’s lumber industry is entering a period of sustained pressure as production volumes continue to fall and regulatory risks increase. Official data shows that lumber output declined by more than 2.5% last year, reinforcing concerns across the forestry and wood processing sectors. According to Rosstat, Russia’s lumber production dropped from 29.2 million cubic metres in 2024 to 28.48 million cubic metres in 2025. Output remains well below historical highs. Current production is estimated to be 2 to 3 million cubic metres lower than the 2019 peak of roughly 32 million cubic metres. The downturn reflects structural challenges rather than short-term disruption. Domestic demand has weakened. Export markets have narrowed. Access to European machinery and technology has been reduced. These pressures are being felt across both logging and downstream processing operations. China now absorbs more than 70% of Russia’s lumber exports. …Softwood lumber production fell by 3.5% last year. Output declined to 25.7 million cubic metres.