![]() VANCOUVER, BC – Canfor Corporation announced today that it will record a non-cash asset write down and impairment charge totaling approximately $321 million in its fourth quarter of 2025 results. Of this amount, $215 million relates to the Company’s lumber segment and $106 million relates to its pulp and paper segment. In the lumber segment, the impairment is associated with the Company’s European operations and reflects ongoing log supply pressures in the region, which have resulted in significant increases in log costs and reduced asset carrying values. In the pulp segment, the impairment reflects sustained declines in global US-dollar pulp list prices as well as continued challenges in securing economically viable fibre necessary to support operations. This impairment charge is non-cash in nature and does not affect Canfor’s liquidity position, cash flows or day-to-day operations.

VANCOUVER, BC – Canfor Corporation announced today that it will record a non-cash asset write down and impairment charge totaling approximately $321 million in its fourth quarter of 2025 results. Of this amount, $215 million relates to the Company’s lumber segment and $106 million relates to its pulp and paper segment. In the lumber segment, the impairment is associated with the Company’s European operations and reflects ongoing log supply pressures in the region, which have resulted in significant increases in log costs and reduced asset carrying values. In the pulp segment, the impairment reflects sustained declines in global US-dollar pulp list prices as well as continued challenges in securing economically viable fibre necessary to support operations. This impairment charge is non-cash in nature and does not affect Canfor’s liquidity position, cash flows or day-to-day operations.

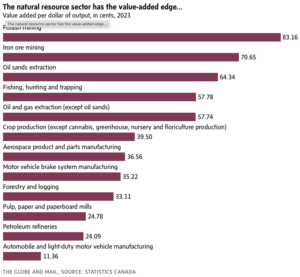

It’s been nearly a century since political economist Harold Innis popularized the phrase “hewers of wood and drawers of water” in decrying Canada’s dependence on natural resources. …Underpinning that cry is the (wrongheaded) assumption that natural resources such as mining, agriculture and energy are second-grade economic activity, less desirable than manufacturing. …That mistake is the foundation for many public policy blunders over many decades. The numbers demolish that myth, and tell a very different story, one in which energy, mining and other natural resources sectors create enormous economic value and are globally competitive. …The federal government needs to get itself out of the way of some of the strongest parts of the Canadian economy. Stop subsidizing inefficient sectors. Stop raising protective tariffs that harm other parts of the economy. Focus on rolling back unjustified regulatory barriers that harm the ability of the entire economy, particularly globally exposed natural resources sectors, to compete. And, most of all, stop the undervaluing Canada’s great natural advantage in natural resources. [to access the full story a Globe & Mail subscription is required]

It’s been nearly a century since political economist Harold Innis popularized the phrase “hewers of wood and drawers of water” in decrying Canada’s dependence on natural resources. …Underpinning that cry is the (wrongheaded) assumption that natural resources such as mining, agriculture and energy are second-grade economic activity, less desirable than manufacturing. …That mistake is the foundation for many public policy blunders over many decades. The numbers demolish that myth, and tell a very different story, one in which energy, mining and other natural resources sectors create enormous economic value and are globally competitive. …The federal government needs to get itself out of the way of some of the strongest parts of the Canadian economy. Stop subsidizing inefficient sectors. Stop raising protective tariffs that harm other parts of the economy. Focus on rolling back unjustified regulatory barriers that harm the ability of the entire economy, particularly globally exposed natural resources sectors, to compete. And, most of all, stop the undervaluing Canada’s great natural advantage in natural resources. [to access the full story a Globe & Mail subscription is required] The pace of homebuilding in Canada continues to slow with no near-term signs of a turnaround, said Canada Mortgage and Housing Corp. on Monday. The national housing agency said the seasonally-adjusted annual pace of housing starts declined 15% in January. Housing starts can vary considerably month-to-month as big projects get started, but the agency’s six-month moving average for annual starts also showed a 3.5% decline. “The six-month trend has decreased for the fourth consecutive month,” said CMHC deputy chief economist Tania Bourassa-Ochoa in a news release. “We expect new construction to continue trending lower going forward as trade and geopolitical uncertainty, high construction costs, weaker demand, and rising inventories continue to constrain developer activity.” She said a near-term turnaround is looking unlikely, and reflects what the agency has been hearing from developers over recent months. The pullback comes amid a variety of pressures, including lower immigration numbers and US trade policy.

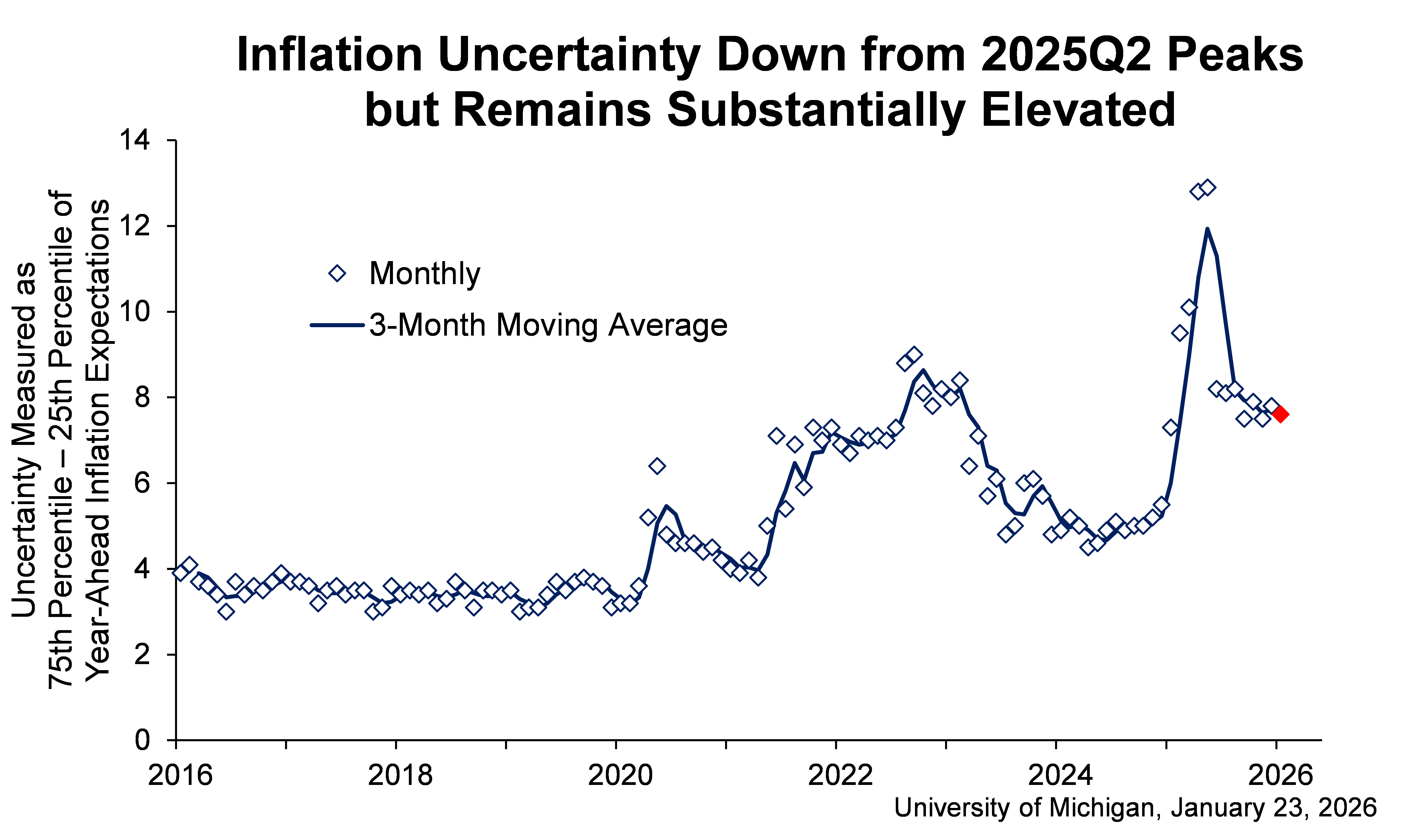

The pace of homebuilding in Canada continues to slow with no near-term signs of a turnaround, said Canada Mortgage and Housing Corp. on Monday. The national housing agency said the seasonally-adjusted annual pace of housing starts declined 15% in January. Housing starts can vary considerably month-to-month as big projects get started, but the agency’s six-month moving average for annual starts also showed a 3.5% decline. “The six-month trend has decreased for the fourth consecutive month,” said CMHC deputy chief economist Tania Bourassa-Ochoa in a news release. “We expect new construction to continue trending lower going forward as trade and geopolitical uncertainty, high construction costs, weaker demand, and rising inventories continue to constrain developer activity.” She said a near-term turnaround is looking unlikely, and reflects what the agency has been hearing from developers over recent months. The pullback comes amid a variety of pressures, including lower immigration numbers and US trade policy. Canada’s annual inflation rate edged down to 2.3% in January, Statistics Canada said on Tuesday, driven downward by a decline in the cost of gasoline. Economists were largely expecting the rate to remain unchanged from December’s 2.4%. Pump prices put pressure on the headline rate, having fallen 16.7% in January compared to the same period last year. With gas excluded, January’s inflation rate came in at 3%. The Bank of Canada’s preferred measures of core inflation, which strip away volatility from one-time tax changes and gas prices, all ticked down in January — bringing those rates closer to the central bank’s two per cent inflation target. “Overall, this is an encouraging result for the Bank of Canada, with inflation finally nearing the [2%] target on a broader basis,” wrote Douglas Porter, chief economist at Bank of Montreal. ›

Canada’s annual inflation rate edged down to 2.3% in January, Statistics Canada said on Tuesday, driven downward by a decline in the cost of gasoline. Economists were largely expecting the rate to remain unchanged from December’s 2.4%. Pump prices put pressure on the headline rate, having fallen 16.7% in January compared to the same period last year. With gas excluded, January’s inflation rate came in at 3%. The Bank of Canada’s preferred measures of core inflation, which strip away volatility from one-time tax changes and gas prices, all ticked down in January — bringing those rates closer to the central bank’s two per cent inflation target. “Overall, this is an encouraging result for the Bank of Canada, with inflation finally nearing the [2%] target on a broader basis,” wrote Douglas Porter, chief economist at Bank of Montreal. › BURNABY, BC — Interfor recorded a net loss in Q4, 2025 of $104.6 million, compared to a net loss of $215.8 million in Q3’25 and a net loss of $49.9 million in Q4’24. Adjusted EBITDA was a loss of $29.2 million on sales of $600.6 million in Q4’25 versus an Adjusted EBITDA loss of $183.8 million on sales of $689.3 million in Q3’25 and Adjusted EBITDA of $80.4 million on sales of $746.5 million in Q4’24. …During and subsequent to Q4’25, Interfor completed a series of financing transactions. Taken together, these transactions significantly enhance Interfor’s financial flexibility, bolster liquidity and provide meaningful additional runway as the Company continues to navigate volatile lumber market conditions. …Lumber production of 753 million board feet was down 159 million board feet versus the preceding quarter. …Interfor’s strategy of maintaining a diversified portfolio of operations in multiple regions allows the Company to both reduce risk and maximize returns on capital over the business cycle.

BURNABY, BC — Interfor recorded a net loss in Q4, 2025 of $104.6 million, compared to a net loss of $215.8 million in Q3’25 and a net loss of $49.9 million in Q4’24. Adjusted EBITDA was a loss of $29.2 million on sales of $600.6 million in Q4’25 versus an Adjusted EBITDA loss of $183.8 million on sales of $689.3 million in Q3’25 and Adjusted EBITDA of $80.4 million on sales of $746.5 million in Q4’24. …During and subsequent to Q4’25, Interfor completed a series of financing transactions. Taken together, these transactions significantly enhance Interfor’s financial flexibility, bolster liquidity and provide meaningful additional runway as the Company continues to navigate volatile lumber market conditions. …Lumber production of 753 million board feet was down 159 million board feet versus the preceding quarter. …Interfor’s strategy of maintaining a diversified portfolio of operations in multiple regions allows the Company to both reduce risk and maximize returns on capital over the business cycle.

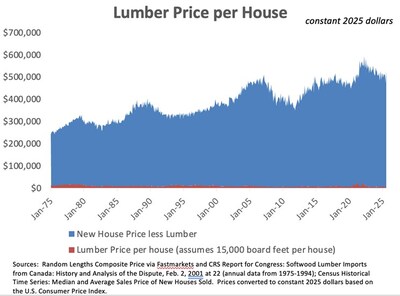

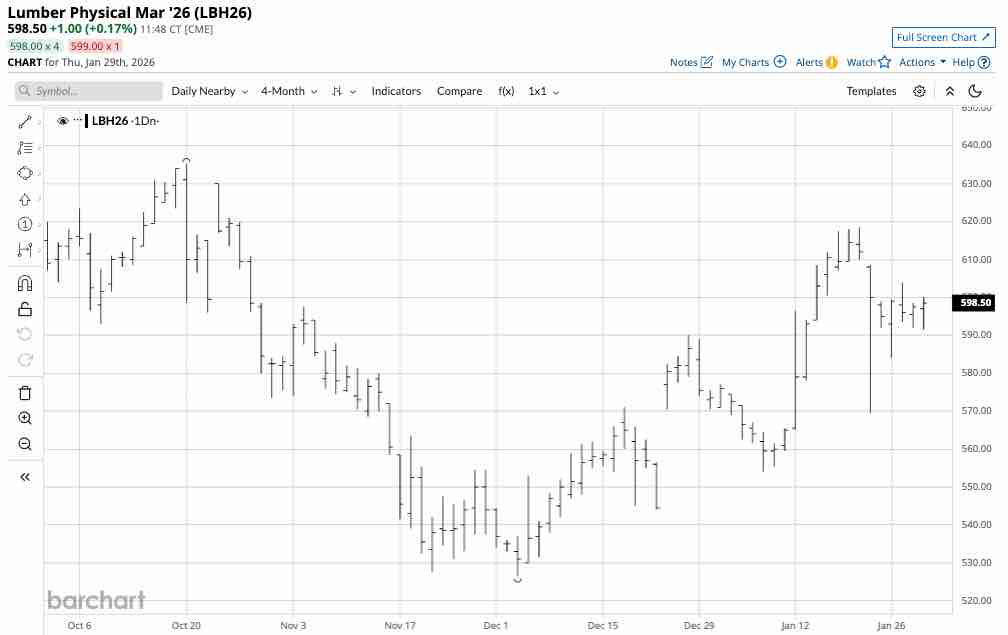

Lumber futures slipped below $590 per thousand board feet, the lowest level in nearly four weeks, as housing demand weakened and earlier restocking momentum faded. Demand softened as financing costs edged higher and housing activity cooled, with US pending home sales plunging 9.3% month on month in December 2025, removing a key source of construction and renovation related wood consumption ahead of the spring building season. At the same time, mills continued running to rebuild inventories after the winter squeeze, increasing physical availability while distributors reported quieter order books. The combination of softer demand and rising availability encouraged position unwinds after January’s rally, with falling volumes and open interest amplifying the price decline. [END]

Lumber futures slipped below $590 per thousand board feet, the lowest level in nearly four weeks, as housing demand weakened and earlier restocking momentum faded. Demand softened as financing costs edged higher and housing activity cooled, with US pending home sales plunging 9.3% month on month in December 2025, removing a key source of construction and renovation related wood consumption ahead of the spring building season. At the same time, mills continued running to rebuild inventories after the winter squeeze, increasing physical availability while distributors reported quieter order books. The combination of softer demand and rising availability encouraged position unwinds after January’s rally, with falling volumes and open interest amplifying the price decline. [END]

Canada’s housing and homelessness crisis touches nearly every Canadian. Over the past decade, while federal housing spending has increased, affordability has worsened for all but the wealthiest, and homelessness is surging. Despite recent declines in housing prices and rents, unsheltered homelessness is still up 300% since 2018, according to the most recent national point-in-time count. The country has a narrow but historic window to tackle this crisis and rebuild our housing system so it delivers at the speed, scale and affordability this moment demands. …Federal action alone won’t get us there. Provinces and territories control the planning systems, development-charge frameworks, zoning rules, supportive housing, health services and income supports. …That is why we need a Canada Housing Accord. [Tim Richter is the chief executive of the Canadian Alliance to End Homelessness and Tyler Meredith is a senior fellow at the Munk School of Global Affairs and Public Policy]

Canada’s housing and homelessness crisis touches nearly every Canadian. Over the past decade, while federal housing spending has increased, affordability has worsened for all but the wealthiest, and homelessness is surging. Despite recent declines in housing prices and rents, unsheltered homelessness is still up 300% since 2018, according to the most recent national point-in-time count. The country has a narrow but historic window to tackle this crisis and rebuild our housing system so it delivers at the speed, scale and affordability this moment demands. …Federal action alone won’t get us there. Provinces and territories control the planning systems, development-charge frameworks, zoning rules, supportive housing, health services and income supports. …That is why we need a Canada Housing Accord. [Tim Richter is the chief executive of the Canadian Alliance to End Homelessness and Tyler Meredith is a senior fellow at the Munk School of Global Affairs and Public Policy] RUSS TAYLOR provided the latest quarterly report from the

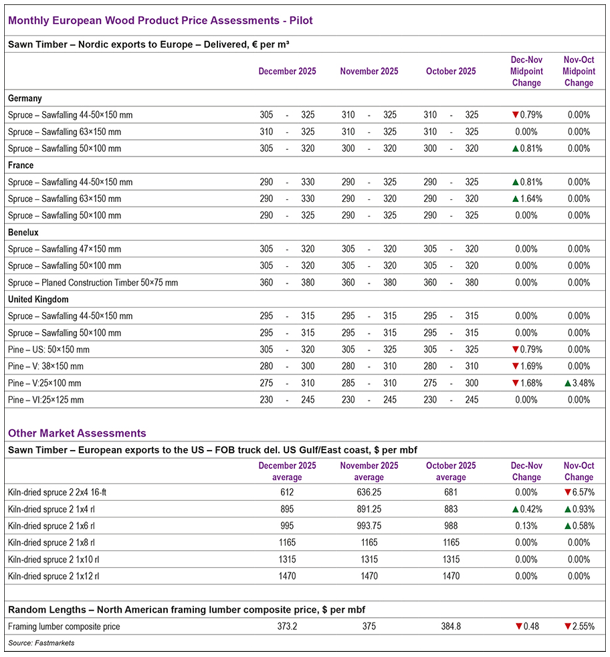

RUSS TAYLOR provided the latest quarterly report from the

MONTREAL — Tariffs and economic angst delivered a significant blow to Canadian National Railway Co. last year, as the question mark hanging over North American free trade continues to threaten profits in 2026. “Tariffs, trade uncertainty and volatility impacted our full-year 2025 revenues by over $350 million,” chief commercial officer Janet Drysdale told analysts on a conference call Friday. Forest products and metals took the biggest bruising, she said, with the two segments seeing a year-over-year revenue drop of eight and four per cent, respectively, in the latest quarter. …On top of trade uncertainty, a less publicized source of angst has rippled through the rail industry since last summer. Union Pacific Corp., the second-largest railway operator in the United States, announced in July it wants to buy Norfolk Southern Corp. in a US$85-billion deal that would create that country’s first transcontinental railway, and potentially trigger a final wave of rail mergers across North America.

MONTREAL — Tariffs and economic angst delivered a significant blow to Canadian National Railway Co. last year, as the question mark hanging over North American free trade continues to threaten profits in 2026. “Tariffs, trade uncertainty and volatility impacted our full-year 2025 revenues by over $350 million,” chief commercial officer Janet Drysdale told analysts on a conference call Friday. Forest products and metals took the biggest bruising, she said, with the two segments seeing a year-over-year revenue drop of eight and four per cent, respectively, in the latest quarter. …On top of trade uncertainty, a less publicized source of angst has rippled through the rail industry since last summer. Union Pacific Corp., the second-largest railway operator in the United States, announced in July it wants to buy Norfolk Southern Corp. in a US$85-billion deal that would create that country’s first transcontinental railway, and potentially trigger a final wave of rail mergers across North America.

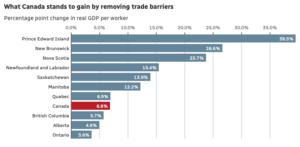

Canada’s economy could gain nearly 7%, or $210 billion, in real GDP over a gradual period by fully removing internal trade barriers between the country’s 13 provinces and territories, according to a report published Tuesday by the International Monetary Fund (IMF). On average, regulation-related barriers are the equivalent of a 9% tariff nationally, estimates the report, which was co-authored by IMF researchers Federico J. Diez and Yuanchen Yang with contributions from University of Calgary economist Trevor Tombe. …Because of the trade barriers between provinces, “Canada isn’t really one economy. It’s really 10 economies,” said Alicia Planincic, director of policy and economics at the Business Council of Alberta in Calgary. …The report points to finance, telecom, transportation and professional services as far-reaching sectors that “ripple through the economy” and raise costs for all of the businesses they touch.

Canada’s economy could gain nearly 7%, or $210 billion, in real GDP over a gradual period by fully removing internal trade barriers between the country’s 13 provinces and territories, according to a report published Tuesday by the International Monetary Fund (IMF). On average, regulation-related barriers are the equivalent of a 9% tariff nationally, estimates the report, which was co-authored by IMF researchers Federico J. Diez and Yuanchen Yang with contributions from University of Calgary economist Trevor Tombe. …Because of the trade barriers between provinces, “Canada isn’t really one economy. It’s really 10 economies,” said Alicia Planincic, director of policy and economics at the Business Council of Alberta in Calgary. …The report points to finance, telecom, transportation and professional services as far-reaching sectors that “ripple through the economy” and raise costs for all of the businesses they touch.

TORONTO — The review of North America’s free trade agreement will play a large part in determining the trajectory of the Canadian economy, as one strategist says he is optimistic that certain concessions could help achieve a positive outcome. Ashish Dewan, a senior investment strategist at Vanguard, said the Canadian economy is still significantly reliant on US trade despite attempts to diversify its trading partners. He said Canada currently has a “trade advantage,” due to a lower effective tariff rate compared with other nations, sitting around six per cent compared with about 16 to 19 per cent faced by other nations. “What’s really having a negative impact on the Canadian economy are those Section 232 sectoral tariffs,” Dewan said. Tariffs covered by Section 232 of the U.S. Trade Expansion Act of 1962 cover a wide range of products like steel, aluminum and lumber and are generally not exempt under the Canada-U.S.-Mexico Agreement, better known as CUSMA.

TORONTO — The review of North America’s free trade agreement will play a large part in determining the trajectory of the Canadian economy, as one strategist says he is optimistic that certain concessions could help achieve a positive outcome. Ashish Dewan, a senior investment strategist at Vanguard, said the Canadian economy is still significantly reliant on US trade despite attempts to diversify its trading partners. He said Canada currently has a “trade advantage,” due to a lower effective tariff rate compared with other nations, sitting around six per cent compared with about 16 to 19 per cent faced by other nations. “What’s really having a negative impact on the Canadian economy are those Section 232 sectoral tariffs,” Dewan said. Tariffs covered by Section 232 of the U.S. Trade Expansion Act of 1962 cover a wide range of products like steel, aluminum and lumber and are generally not exempt under the Canada-U.S.-Mexico Agreement, better known as CUSMA. Canada’s six largest CMAs recorded a 3.9% rise in housing starts in 2025, driven by a 58% jump in Montréal and record starts in Calgary and Edmonton, while Toronto fell 31% and Vancouver slipped 3%, CMHC said. CMHC said the metro gains helped lift the national annual total for all areas in Canada to 259,028 housing starts in 2025, up 5.6% from 245,367 in 2024 and ranking as the fifth highest annual total on record. …The year-over-year increase was driven by a second consecutive year of record rental housing starts, which made up just over half of all housing starts in Canada’s urban centres, CMHC said. …Among Canada’s three largest cities, CMHC said all posted year-over-year increases in December. Toronto recorded a 151% increase, driven by higher multi-unit starts. Montréal posted a 123% increase, driven by higher starts across all dwelling types. Vancouver reported a +17% increase, also driven by multi-unit starts.

Canada’s six largest CMAs recorded a 3.9% rise in housing starts in 2025, driven by a 58% jump in Montréal and record starts in Calgary and Edmonton, while Toronto fell 31% and Vancouver slipped 3%, CMHC said. CMHC said the metro gains helped lift the national annual total for all areas in Canada to 259,028 housing starts in 2025, up 5.6% from 245,367 in 2024 and ranking as the fifth highest annual total on record. …The year-over-year increase was driven by a second consecutive year of record rental housing starts, which made up just over half of all housing starts in Canada’s urban centres, CMHC said. …Among Canada’s three largest cities, CMHC said all posted year-over-year increases in December. Toronto recorded a 151% increase, driven by higher multi-unit starts. Montréal posted a 123% increase, driven by higher starts across all dwelling types. Vancouver reported a +17% increase, also driven by multi-unit starts. Canada’s annual inflation rate ticked up to 2.4% in December compared to the same period last year, when the federal government implemented a GST break that brought some prices down, Statistics Canada said. The temporary tax cut, which began on Dec. 14, 2024, lasted for two months. It reverberated through monthly inflation data for part of 2025 but officially fell out of the year-over-year movement last month, sending price growth accelerating, according to the data agency. December’s rate was a smidge higher than the 2.2% rate seen in November. It was partly offset by a year-over-year decline in gas prices. With energy excluded, inflation rose to 3% in December. …”The main takeaway here is that after a year of some wide divergences, almost all of the main measures of inflation are now very close to [2.5%], in tune with the Bank of Canada’s view on the pace of underlying inflation,” wrote BMO’s Douglas Porter.

Canada’s annual inflation rate ticked up to 2.4% in December compared to the same period last year, when the federal government implemented a GST break that brought some prices down, Statistics Canada said. The temporary tax cut, which began on Dec. 14, 2024, lasted for two months. It reverberated through monthly inflation data for part of 2025 but officially fell out of the year-over-year movement last month, sending price growth accelerating, according to the data agency. December’s rate was a smidge higher than the 2.2% rate seen in November. It was partly offset by a year-over-year decline in gas prices. With energy excluded, inflation rose to 3% in December. …”The main takeaway here is that after a year of some wide divergences, almost all of the main measures of inflation are now very close to [2.5%], in tune with the Bank of Canada’s view on the pace of underlying inflation,” wrote BMO’s Douglas Porter.

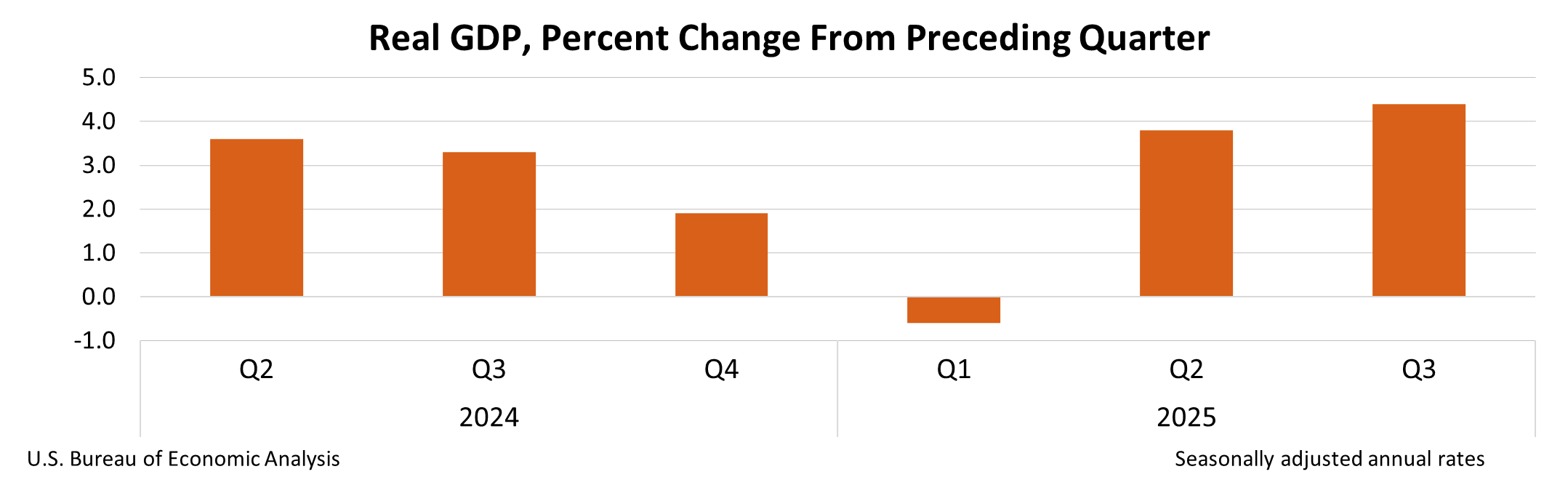

There are solid reasons to expect near-term strength in the US and Canadian construction markets. In the US, rapid technological progress and supportive federal policies are driving major investments in semiconductor fabrication, AI-related data centers, and energy infrastructure, with growing momentum toward nuclear power. In Canada, federal and provincial governments are promoting “nation-building” projects that emphasize LNG export capacity, port expansions, and new mines for critical minerals required by the digital economy. Both nations recognize that housing supply must rise substantially to meet population needs, signaling a long-term boost in residential construction. Yet, 2025 proved disappointing for overall construction performance, especially in employment. …Housing activity revealed a sharper divide between the two nations. U.S. housing starts in November 2025 dropped to an annualized 1.246 million units, the lowest since the pandemic. Most analysts believe the country needs at least 1.5 million starts per year to meet demand.

There are solid reasons to expect near-term strength in the US and Canadian construction markets. In the US, rapid technological progress and supportive federal policies are driving major investments in semiconductor fabrication, AI-related data centers, and energy infrastructure, with growing momentum toward nuclear power. In Canada, federal and provincial governments are promoting “nation-building” projects that emphasize LNG export capacity, port expansions, and new mines for critical minerals required by the digital economy. Both nations recognize that housing supply must rise substantially to meet population needs, signaling a long-term boost in residential construction. Yet, 2025 proved disappointing for overall construction performance, especially in employment. …Housing activity revealed a sharper divide between the two nations. U.S. housing starts in November 2025 dropped to an annualized 1.246 million units, the lowest since the pandemic. Most analysts believe the country needs at least 1.5 million starts per year to meet demand.  B.C.’s export performance moved against the national pattern in November. Domestic exports to international markets rose 7.6 per cent year over year to $4.59 billion, whereas exports nationally declined by about four per cent on a customs basis. This contrast partly reflects differences in the types of goods each region exports. Nevertheless, provincial export trends remain soft, reflecting U.S. tariffs on key products like lumber, and end of de minimis treatment of low value exports. Year-to-date, B.C. exports slipped a mild 0.1 per cent from same-period 2024, which was slightly stronger than the national reading. …That said, a declining trend continued in the battered forestry sector (-13.7 per cent year over year), where tariffs have compounded weakness from timber supply constraints and other duties already imposed by the U.S.

B.C.’s export performance moved against the national pattern in November. Domestic exports to international markets rose 7.6 per cent year over year to $4.59 billion, whereas exports nationally declined by about four per cent on a customs basis. This contrast partly reflects differences in the types of goods each region exports. Nevertheless, provincial export trends remain soft, reflecting U.S. tariffs on key products like lumber, and end of de minimis treatment of low value exports. Year-to-date, B.C. exports slipped a mild 0.1 per cent from same-period 2024, which was slightly stronger than the national reading. …That said, a declining trend continued in the battered forestry sector (-13.7 per cent year over year), where tariffs have compounded weakness from timber supply constraints and other duties already imposed by the U.S. EDMUNDSTON, New Brunswick – Acadian Timber reported financial and operating results for the three months ended December 31, 2025 as well as for the full 2025 fiscal year. “While 2025 brought a multitude of challenges, Acadian delivered steady operational performance in New Brunswick, helping to offset weather-related challenges, trucking constraints, and productivity issues in Maine,” said Adam Sheparski, President and Chief Executive Officer. …During the fourth quarter, Acadian generated sales of $22.0 million compared to $20.2 million in the fourth quarter of 2024. Acadian generated $5.2 million of Adjusted EBITDA and declared dividends of $5.3 million. During 2025, Acadian generated revenue from timber sales and services of $87.0 million, compared to $91.6 million in the prior year. The sale of 752,100 voluntary carbon credits contributed an additional $24.6 million to total sales in 2024 while no sales of carbon credits occurred in 2025.

EDMUNDSTON, New Brunswick – Acadian Timber reported financial and operating results for the three months ended December 31, 2025 as well as for the full 2025 fiscal year. “While 2025 brought a multitude of challenges, Acadian delivered steady operational performance in New Brunswick, helping to offset weather-related challenges, trucking constraints, and productivity issues in Maine,” said Adam Sheparski, President and Chief Executive Officer. …During the fourth quarter, Acadian generated sales of $22.0 million compared to $20.2 million in the fourth quarter of 2024. Acadian generated $5.2 million of Adjusted EBITDA and declared dividends of $5.3 million. During 2025, Acadian generated revenue from timber sales and services of $87.0 million, compared to $91.6 million in the prior year. The sale of 752,100 voluntary carbon credits contributed an additional $24.6 million to total sales in 2024 while no sales of carbon credits occurred in 2025.  Contractors in certain niches can expect some meaningful materials price reductions after the Supreme Court struck down most of President Trump’s tariffs Friday. The court rejected Trump’s claim to authority to impose reciprocal tariffs. That would drive “a modest but meaningful reduction in materials price escalation” for specialty equipment, HVAC and electrical systems and fixtures, said Anirban Basu, chief economist at Associated Builders and Contractors. …But the administration quickly signaled plans for alternative tariff methods shortly after the ruling. AGC also noted other materials-specific tariffs on lumber, steel, aluminum and copper products are unaffected by Friday’s decision. Taken together, that means the Supreme Court decision “could be short-lived and completely counteracted,” said Basu. That back-and-forth tends to stall construction activity as owners and contractors weigh whether the decision will hold. …AGC has told builders not to hold their breath waiting for refund checks.

Contractors in certain niches can expect some meaningful materials price reductions after the Supreme Court struck down most of President Trump’s tariffs Friday. The court rejected Trump’s claim to authority to impose reciprocal tariffs. That would drive “a modest but meaningful reduction in materials price escalation” for specialty equipment, HVAC and electrical systems and fixtures, said Anirban Basu, chief economist at Associated Builders and Contractors. …But the administration quickly signaled plans for alternative tariff methods shortly after the ruling. AGC also noted other materials-specific tariffs on lumber, steel, aluminum and copper products are unaffected by Friday’s decision. Taken together, that means the Supreme Court decision “could be short-lived and completely counteracted,” said Basu. That back-and-forth tends to stall construction activity as owners and contractors weigh whether the decision will hold. …AGC has told builders not to hold their breath waiting for refund checks.

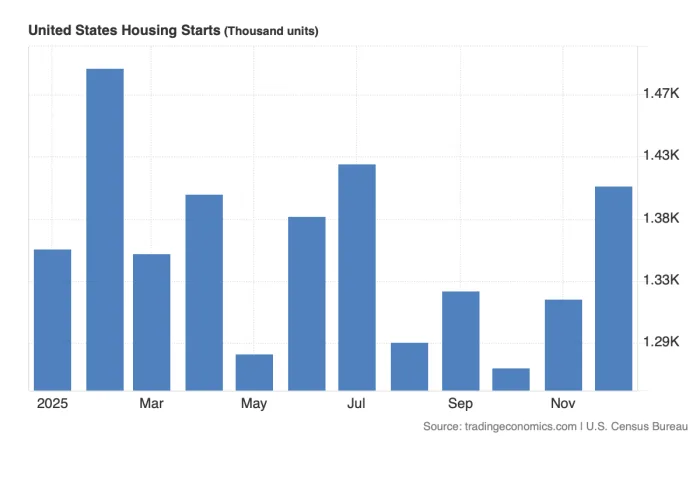

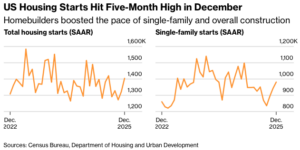

New residential construction in the US rose to a five-month high in December, as homebuilders boosted production to take advantage of lower borrowing costs. Housing starts increased 6.2% to an annual pace of 1.4 million homes in December, according to figures released Wednesday by the government, which were delayed by fall’s federal shutdown. …The advance was broad-based, with both single-family home starts and apartment projects rising at year’s end. The number of one-family homes started was the highest since February. The stronger construction numbers suggest that builders were growing more confident at year’s end even as they continued to sell off a bloated inventory of new houses. For the full year, however, starts notched a fourth-straight annual decline …In December, building permits, which point to future construction, rose 4.3% to an annualized pace of 1.45 million, the highest since March, government data show. Single-family permits fell slightly. [to access the full story a Bloomberg subscription is required]

New residential construction in the US rose to a five-month high in December, as homebuilders boosted production to take advantage of lower borrowing costs. Housing starts increased 6.2% to an annual pace of 1.4 million homes in December, according to figures released Wednesday by the government, which were delayed by fall’s federal shutdown. …The advance was broad-based, with both single-family home starts and apartment projects rising at year’s end. The number of one-family homes started was the highest since February. The stronger construction numbers suggest that builders were growing more confident at year’s end even as they continued to sell off a bloated inventory of new houses. For the full year, however, starts notched a fourth-straight annual decline …In December, building permits, which point to future construction, rose 4.3% to an annualized pace of 1.45 million, the highest since March, government data show. Single-family permits fell slightly. [to access the full story a Bloomberg subscription is required] Reality-television stars are rarely consulted on matters of public policy. But in April, Realtor.com asked Tarek El Moussa to comment on the White House’s “Liberation Day” tariffs. The Southern California entrepreneur, who rose to fame on the popularity of HGTV’s Flip or Fop franchise, warned that higher import taxes would harm “new-home builders” and “first-time buyers” the most — after all, “luxury buyers” could absorb greater costs. Aspiring homeowners, he averred, are “usually strapped for cash,” and “doing everything they can just to buy a house.” Now that the second Trump administration has passed its one-year anniversary, all evidence indicates that El Moussa understands his industry well. There is little doubt that his trade war erects a sizable obstacle before those looking to find a place of their own. …The types of wood available in the US are not always the same as what’s available from Canadian imports.

Reality-television stars are rarely consulted on matters of public policy. But in April, Realtor.com asked Tarek El Moussa to comment on the White House’s “Liberation Day” tariffs. The Southern California entrepreneur, who rose to fame on the popularity of HGTV’s Flip or Fop franchise, warned that higher import taxes would harm “new-home builders” and “first-time buyers” the most — after all, “luxury buyers” could absorb greater costs. Aspiring homeowners, he averred, are “usually strapped for cash,” and “doing everything they can just to buy a house.” Now that the second Trump administration has passed its one-year anniversary, all evidence indicates that El Moussa understands his industry well. There is little doubt that his trade war erects a sizable obstacle before those looking to find a place of their own. …The types of wood available in the US are not always the same as what’s available from Canadian imports.

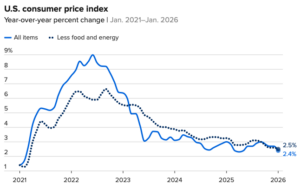

The cost of goods and services rose at a slower annual rate than expected in January, providing hope that the nagging U.S. inflation problem could be starting to ease. The consumer price index for January accelerated 2.4% from the same time a year ago, down 0.3 percentage point from the prior month, the Bureau of Labor Statistics reported Friday. That pulled the inflation rate down to where it was the month after President Donald Trump in April 2025 announced aggressive tariffs on U.S. imports. Excluding food and energy, the core CPI was up 2.5%. Economists surveyed by Dow Jones had been looking for an annual rate of 2.5% for both readings. On a monthly basis, the all-items index was up a seasonally adjusted 0.2% while core gained 0.3%. …Though the category accounted for much of the CPI gain, shelter costs rose just 0.2% for the month, bringing the annual increase down to 3%.

The cost of goods and services rose at a slower annual rate than expected in January, providing hope that the nagging U.S. inflation problem could be starting to ease. The consumer price index for January accelerated 2.4% from the same time a year ago, down 0.3 percentage point from the prior month, the Bureau of Labor Statistics reported Friday. That pulled the inflation rate down to where it was the month after President Donald Trump in April 2025 announced aggressive tariffs on U.S. imports. Excluding food and energy, the core CPI was up 2.5%. Economists surveyed by Dow Jones had been looking for an annual rate of 2.5% for both readings. On a monthly basis, the all-items index was up a seasonally adjusted 0.2% while core gained 0.3%. …Though the category accounted for much of the CPI gain, shelter costs rose just 0.2% for the month, bringing the annual increase down to 3%.

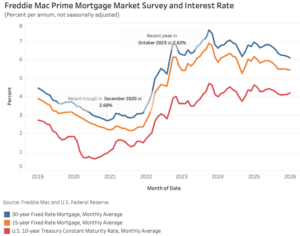

Long-term mortgage rates continued to decline in January. According to Freddie Mac, the 30-year fixed-rate mortgage averaged 6.10% last month, 9 basis points (bps) lower than December. Meanwhile, the 15-year rate declined 4 bps to 5.44%. Compared to a year ago, the 30-year rate is lower by 86 bps. The 15-year rate is also lower by 72 bps. The 10-year Treasury yield, a key benchmark for long-term borrowing, averaged 4.20% in January – an increase of 8 bps from the previous month, but remained considerably lower than last year by 43 bps. While mortgage rates typically move in tandem with the treasury yields, the spread between the two narrowed during the month. Reports that the Trump administration encouraged Fannie Mae and Freddie Mac to expand purchases of mortgage-backed securities (MBS) boosted demand for MBS, pushing mortgage rates lower. However, treasury yields rose sharply in the final week of January from global and fiscal pressures.

Long-term mortgage rates continued to decline in January. According to Freddie Mac, the 30-year fixed-rate mortgage averaged 6.10% last month, 9 basis points (bps) lower than December. Meanwhile, the 15-year rate declined 4 bps to 5.44%. Compared to a year ago, the 30-year rate is lower by 86 bps. The 15-year rate is also lower by 72 bps. The 10-year Treasury yield, a key benchmark for long-term borrowing, averaged 4.20% in January – an increase of 8 bps from the previous month, but remained considerably lower than last year by 43 bps. While mortgage rates typically move in tandem with the treasury yields, the spread between the two narrowed during the month. Reports that the Trump administration encouraged Fannie Mae and Freddie Mac to expand purchases of mortgage-backed securities (MBS) boosted demand for MBS, pushing mortgage rates lower. However, treasury yields rose sharply in the final week of January from global and fiscal pressures.  When it comes to housing affordability, the logic of “build build build” is straightforward enough: Housing is too expensive. If there were more of it, prices would fall. …Homebuilders are even pushing a plan for a million new affordable houses. …Unfortunately, it’s not that simple. The problem of housing affordability is much bigger than insufficient supply; it’s a mismatch with demand. And that demand is driven by income inequality that has seen soaring income growth at the top and tepid growth (or even stagnation) in the middle. In other words: The way to improve housing affordability is to reduce income inequality. …What’s needed are policies that increase income for households at the bottom and middle. Rather than boosting the housing supply in the hope that they benefit, the answer is to fix the labor market to make sure that they do.

When it comes to housing affordability, the logic of “build build build” is straightforward enough: Housing is too expensive. If there were more of it, prices would fall. …Homebuilders are even pushing a plan for a million new affordable houses. …Unfortunately, it’s not that simple. The problem of housing affordability is much bigger than insufficient supply; it’s a mismatch with demand. And that demand is driven by income inequality that has seen soaring income growth at the top and tepid growth (or even stagnation) in the middle. In other words: The way to improve housing affordability is to reduce income inequality. …What’s needed are policies that increase income for households at the bottom and middle. Rather than boosting the housing supply in the hope that they benefit, the answer is to fix the labor market to make sure that they do.  The United States is one of the world’s largest timberland investment markets, with returns driven primarily by land values rather than timber prices, according to Domain Timber Advisors’ timberland market analysis. Timberland values remain strong at the end of 2025, supported by continued appreciation in land values, while timber prices remain relatively flat. …During 2025, Domain underwrites 14 institutional bid events, 54 public listings, and 38 off-market or non-public offerings. By the end of the fourth quarter, the acquisition pipeline consists of 46 deals covering more than 500 thousand acres, providing visibility into pricing dynamics, regional demand shifts, and emerging non-timber value drivers. …Looking ahead, Domain states that renewable energy development and technology infrastructure are expected to expand non-timber revenue opportunities in 2026 and beyond. Alternative timber product markets, including molded fiber products and biomass-to-electricity, are expected to offset part of the pulpwood demand lost due to mill closures and production quotas.

The United States is one of the world’s largest timberland investment markets, with returns driven primarily by land values rather than timber prices, according to Domain Timber Advisors’ timberland market analysis. Timberland values remain strong at the end of 2025, supported by continued appreciation in land values, while timber prices remain relatively flat. …During 2025, Domain underwrites 14 institutional bid events, 54 public listings, and 38 off-market or non-public offerings. By the end of the fourth quarter, the acquisition pipeline consists of 46 deals covering more than 500 thousand acres, providing visibility into pricing dynamics, regional demand shifts, and emerging non-timber value drivers. …Looking ahead, Domain states that renewable energy development and technology infrastructure are expected to expand non-timber revenue opportunities in 2026 and beyond. Alternative timber product markets, including molded fiber products and biomass-to-electricity, are expected to offset part of the pulpwood demand lost due to mill closures and production quotas.

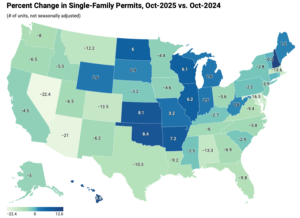

In October, single-family building permits weakened, reflecting continued caution among builders amid affordability constraints and financing challenges. In contrast, multifamily permit activity remained steady and continued to perform relatively well. Together, these trends suggest that while demand for new housing persists, builders are adjusting residential construction activity in response to evolving market conditions. Because permits typically precede construction starts, these patterns offer insight into the near-term outlook for residential building activity. Over the first ten months of 2025, the number of single-family permits issued nationwide reached 787,122. On a year-over-year basis, this represents a 7.0 percent decline compared with the October 2024 year-to-date total of 846,446. Multifamily permitting activity was stronger, with 426,352 permits issued nationwide, marking a 5.7 percent increase from the same period last year.

In October, single-family building permits weakened, reflecting continued caution among builders amid affordability constraints and financing challenges. In contrast, multifamily permit activity remained steady and continued to perform relatively well. Together, these trends suggest that while demand for new housing persists, builders are adjusting residential construction activity in response to evolving market conditions. Because permits typically precede construction starts, these patterns offer insight into the near-term outlook for residential building activity. Over the first ten months of 2025, the number of single-family permits issued nationwide reached 787,122. On a year-over-year basis, this represents a 7.0 percent decline compared with the October 2024 year-to-date total of 846,446. Multifamily permitting activity was stronger, with 426,352 permits issued nationwide, marking a 5.7 percent increase from the same period last year.

Global markets plunged Tuesday after President Trump reignited fears of a US trade war with the European Union, America’s largest trading partner. The president showed no signs of backing off his threat from Saturday to hit seven EU countries and the United Kingdom with new tariffs unless they supported his push for American control of Greenland. Asked if he would be willing to use force to seize the semi-autonomous Danish territory, Trump replied, “No comment,” on Monday. The S&P 500 sold off by around 1.3% in early trading, while the Nasdaq Composite plunged 1.7%. The Dow Jones Industrial Average dropped more than 600 points. The S&P 500 has erased its gains for the year so far. Investors also sold off U.S. government bonds, driving up interest rates. Rising returns on US treasuries usually translate into higher mortgage rates and interest on new personal loans.

Global markets plunged Tuesday after President Trump reignited fears of a US trade war with the European Union, America’s largest trading partner. The president showed no signs of backing off his threat from Saturday to hit seven EU countries and the United Kingdom with new tariffs unless they supported his push for American control of Greenland. Asked if he would be willing to use force to seize the semi-autonomous Danish territory, Trump replied, “No comment,” on Monday. The S&P 500 sold off by around 1.3% in early trading, while the Nasdaq Composite plunged 1.7%. The Dow Jones Industrial Average dropped more than 600 points. The S&P 500 has erased its gains for the year so far. Investors also sold off U.S. government bonds, driving up interest rates. Rising returns on US treasuries usually translate into higher mortgage rates and interest on new personal loans.

Russia’s lumber industry is entering a period of sustained pressure as production volumes continue to fall and regulatory risks increase. Official data shows that lumber output declined by more than 2.5% last year, reinforcing concerns across the forestry and wood processing sectors. According to Rosstat, Russia’s lumber production dropped from 29.2 million cubic metres in 2024 to 28.48 million cubic metres in 2025. Output remains well below historical highs. Current production is estimated to be 2 to 3 million cubic metres lower than the 2019 peak of roughly 32 million cubic metres. The downturn reflects structural challenges rather than short-term disruption. Domestic demand has weakened. Export markets have narrowed. Access to European machinery and technology has been reduced. These pressures are being felt across both logging and downstream processing operations. China now absorbs more than 70% of Russia’s lumber exports. …Softwood lumber production fell by 3.5% last year. Output declined to 25.7 million cubic metres.

Russia’s lumber industry is entering a period of sustained pressure as production volumes continue to fall and regulatory risks increase. Official data shows that lumber output declined by more than 2.5% last year, reinforcing concerns across the forestry and wood processing sectors. According to Rosstat, Russia’s lumber production dropped from 29.2 million cubic metres in 2024 to 28.48 million cubic metres in 2025. Output remains well below historical highs. Current production is estimated to be 2 to 3 million cubic metres lower than the 2019 peak of roughly 32 million cubic metres. The downturn reflects structural challenges rather than short-term disruption. Domestic demand has weakened. Export markets have narrowed. Access to European machinery and technology has been reduced. These pressures are being felt across both logging and downstream processing operations. China now absorbs more than 70% of Russia’s lumber exports. …Softwood lumber production fell by 3.5% last year. Output declined to 25.7 million cubic metres.

HÀ NỘI — Despite unprecedented challenges from global markets and the growing impacts of climate change, 2025 marked a historic milestone for Việt Nam’s wood industry, as export turnover of timber and wood products surpassed US$17 billion for the first time. According to data from Việt Nam Customs, exports of timber and wood products reached nearly $1.7 billion in December 2025 alone, bringing total export value for the year to $17.2 billion – an increase of nearly 6 per cent compared with 2024. In 2025, exports of timber and wood products to the US totalled $9.46 billion, up 4.4 per cent year on year and accounting for approximately 55 per cent of the industry’s total export turnover. Việt Nam continued to maintain its position as the largest supplier of wooden furniture to the US market. …Việt Nam’s market share of wooden furniture in the US increased significantly, rising from 40.5 per cent in the first eight months of 2024 to 45.3 per cent in the same period of 2025.

HÀ NỘI — Despite unprecedented challenges from global markets and the growing impacts of climate change, 2025 marked a historic milestone for Việt Nam’s wood industry, as export turnover of timber and wood products surpassed US$17 billion for the first time. According to data from Việt Nam Customs, exports of timber and wood products reached nearly $1.7 billion in December 2025 alone, bringing total export value for the year to $17.2 billion – an increase of nearly 6 per cent compared with 2024. In 2025, exports of timber and wood products to the US totalled $9.46 billion, up 4.4 per cent year on year and accounting for approximately 55 per cent of the industry’s total export turnover. Việt Nam continued to maintain its position as the largest supplier of wooden furniture to the US market. …Việt Nam’s market share of wooden furniture in the US increased significantly, rising from 40.5 per cent in the first eight months of 2024 to 45.3 per cent in the same period of 2025.

Deposits $10.6 Billion CAD + Interest 2.6 Billion + FX Gain 0.5 Billion = Total $13.7 Billion

Canadian softwood lumber exporters are currently paying a combined duty deposit rate of 45.16% on lumber imported into the United States.