![]() NEW YORK — Mercer International reported third quarter 2025 Operating EBITDA of negative $28.1 million, a decrease from positive $50.5 million in the same quarter of 2024 and negative $20.9 million in the second quarter of 2025. In the third quarter of 2025, net loss was $80.8 million compared to $17.6 million in the same quarter of 2024 and $86.1 million in the second quarter of 2025. Mr. Juan Carlos Bueno, CEO, stated: “In the third quarter of 2025, persistent global economic and trade uncertainties, fiber scarcity in Germany as well as the impact of pulp substitution accelerated the decline in pulp market demand and pricing, which negatively impacted our operating results and contributed to a $20.4 million non-cash inventory impairment charge in the quarter.

NEW YORK — Mercer International reported third quarter 2025 Operating EBITDA of negative $28.1 million, a decrease from positive $50.5 million in the same quarter of 2024 and negative $20.9 million in the second quarter of 2025. In the third quarter of 2025, net loss was $80.8 million compared to $17.6 million in the same quarter of 2024 and $86.1 million in the second quarter of 2025. Mr. Juan Carlos Bueno, CEO, stated: “In the third quarter of 2025, persistent global economic and trade uncertainties, fiber scarcity in Germany as well as the impact of pulp substitution accelerated the decline in pulp market demand and pricing, which negatively impacted our operating results and contributed to a $20.4 million non-cash inventory impairment charge in the quarter.

Lumber futures steadied around $540 per thousand board feet, hovering near seven-week lows, after a sharp selloff driven mainly by softer US construction demand and lingering post-rally inventories. US housing starts and builder activity failed to accelerate, leaving order flow thin and dealer and distributor stocks higher than the summer buying binge implied. Supply has only partially adjusted, with North American mills signaling temporary curtailments, but looming US softwood measures and announced support for Canada’s industry have kept export channels and production incentives intact, preventing a rapid physical tightening. Traders are now pricing a likely mix of modest Q4 production cuts, seasonal pre-winter restocking and the risk of trade-related disruptions.

Lumber futures steadied around $540 per thousand board feet, hovering near seven-week lows, after a sharp selloff driven mainly by softer US construction demand and lingering post-rally inventories. US housing starts and builder activity failed to accelerate, leaving order flow thin and dealer and distributor stocks higher than the summer buying binge implied. Supply has only partially adjusted, with North American mills signaling temporary curtailments, but looming US softwood measures and announced support for Canada’s industry have kept export channels and production incentives intact, preventing a rapid physical tightening. Traders are now pricing a likely mix of modest Q4 production cuts, seasonal pre-winter restocking and the risk of trade-related disruptions. MONTREAL — CN Rail reported its financial and operating results for the third quarter ended September 30, 2025. Highlights include: Revenues of C$4,165 million, an increase of C$55 million, or 1%; Net income of C$1,139 million, an increase of C$54 million, or 5%. …Tracy Robinson, President and Chief Executive Officer said, “We are taking decisive actions to navigate a challenging macro environment including doubling down on productivity efforts, setting our 2026 capital spend at C$2.8 billion*, down nearly C$600 million from this year’s levels, driving increased free cash flow on a go-forward basis. We are positioning this business to benefit from higher future volumes and ensuring everything we do enhances our customers and shareholders long term value.”

MONTREAL — CN Rail reported its financial and operating results for the third quarter ended September 30, 2025. Highlights include: Revenues of C$4,165 million, an increase of C$55 million, or 1%; Net income of C$1,139 million, an increase of C$54 million, or 5%. …Tracy Robinson, President and Chief Executive Officer said, “We are taking decisive actions to navigate a challenging macro environment including doubling down on productivity efforts, setting our 2026 capital spend at C$2.8 billion*, down nearly C$600 million from this year’s levels, driving increased free cash flow on a go-forward basis. We are positioning this business to benefit from higher future volumes and ensuring everything we do enhances our customers and shareholders long term value.” Canadian Pacific Kansas City reported a big profit boost in its latest quarter despite US tariff disruption and fears over fallout from a potential merger of rivals down the line. The railway saw net income for the quarter ended Sept. 30 rise 10% year-over-year to $917 million. Revenues increased three per cent to $3.66 billion on the back of higher shipping volumes. Grain, potash and container volumes rose markedly year-over-year while forest products — struggling under a sectoral tariff imposed by US President Trump — and energy, chemicals and plastics sagged. …Cross-border steel shipments also dropped due to 50% US tariffs on imports of the metal, though CPKC helped make up the decline with domestic traffic and direct Canada-to-Mexico trade, said chief marketing officer John Brooks. A new item of concern crossed the CEO’s desk over the summer. Union Pacific announced in July it wants to buy Norfolk Southern, and potentially trigger a final wave of rail mergers.

Canadian Pacific Kansas City reported a big profit boost in its latest quarter despite US tariff disruption and fears over fallout from a potential merger of rivals down the line. The railway saw net income for the quarter ended Sept. 30 rise 10% year-over-year to $917 million. Revenues increased three per cent to $3.66 billion on the back of higher shipping volumes. Grain, potash and container volumes rose markedly year-over-year while forest products — struggling under a sectoral tariff imposed by US President Trump — and energy, chemicals and plastics sagged. …Cross-border steel shipments also dropped due to 50% US tariffs on imports of the metal, though CPKC helped make up the decline with domestic traffic and direct Canada-to-Mexico trade, said chief marketing officer John Brooks. A new item of concern crossed the CEO’s desk over the summer. Union Pacific announced in July it wants to buy Norfolk Southern, and potentially trigger a final wave of rail mergers. Lumber futures tumbled toward $560 per thousand board feet, a seven-week low, as weakening demand, persistent oversupply, and trade-policy uncertainties converged. US tariffs are intensifying pressure on Canadian softwood, with existing antidumping and countervailing duties around 35%, plus new Section 232 levies of 10% on timber and 25% on wood products, lifting import costs above 45%. Weak demand compounds the decline, with US residential building permits at a seasonally adjusted 1.4 million units in July, the lowest since June 2020, and construction spending down 3.4% from May 2024. Housing starts remain near five-year lows, keeping retail price pass-through muted despite higher import costs. Export channels have narrowed, with Canadian softwood constrained by tariffs and hardwood exports to China dropping from 40% of volume in 2017 to 7% today. Temporary curtailments and mill closures are emerging, yet abundant inventories and sluggish construction sustain downward pressure. [END]

Lumber futures tumbled toward $560 per thousand board feet, a seven-week low, as weakening demand, persistent oversupply, and trade-policy uncertainties converged. US tariffs are intensifying pressure on Canadian softwood, with existing antidumping and countervailing duties around 35%, plus new Section 232 levies of 10% on timber and 25% on wood products, lifting import costs above 45%. Weak demand compounds the decline, with US residential building permits at a seasonally adjusted 1.4 million units in July, the lowest since June 2020, and construction spending down 3.4% from May 2024. Housing starts remain near five-year lows, keeping retail price pass-through muted despite higher import costs. Export channels have narrowed, with Canadian softwood constrained by tariffs and hardwood exports to China dropping from 40% of volume in 2017 to 7% today. Temporary curtailments and mill closures are emerging, yet abundant inventories and sluggish construction sustain downward pressure. [END] The Bank of Canada cut its interest rate by 25 basis points to 2.25 per cent on Wednesday, but signalled that it may end its easing cycle there if the economy operates in line with its latest forecast. …Bank of Canada governor Tiff Macklem said, “If the economy evolves roughly in line with the outlook in our Monetary Policy Report, governing council sees the current policy rate at about the right level to keep inflation close to 2% while.” …The central bank presented its first baseline forecast since January after trade war uncertainty prompted policymakers to instead assess multiple potential scenarios. After a contraction in the second quarter, the bank expects weak growth for the remainder of 2025, with 0.5% annualized GDP growth in the third quarter and 1% growth in the last quarter of this year. It projects GDP growth of 1.1% in 2026 and 1.6& in 2027.

The Bank of Canada cut its interest rate by 25 basis points to 2.25 per cent on Wednesday, but signalled that it may end its easing cycle there if the economy operates in line with its latest forecast. …Bank of Canada governor Tiff Macklem said, “If the economy evolves roughly in line with the outlook in our Monetary Policy Report, governing council sees the current policy rate at about the right level to keep inflation close to 2% while.” …The central bank presented its first baseline forecast since January after trade war uncertainty prompted policymakers to instead assess multiple potential scenarios. After a contraction in the second quarter, the bank expects weak growth for the remainder of 2025, with 0.5% annualized GDP growth in the third quarter and 1% growth in the last quarter of this year. It projects GDP growth of 1.1% in 2026 and 1.6& in 2027. Let’s keep this simple: lumber and steel are two of the biggest drivers of flatbed freight in this country. …So where are we right now, closing out 2025? Lumber futures are sliding off their highs and steel demand is soft with some pockets still running hot. That combination is sending a pretty clear message to flatbed haulers: expect mixed demand instead of broad “every lane is on fire” demand. Some regions will stay busy. Some will get quiet. …Lumber futures have fallen back into the $590–$610/mbf range, down double digits from that August spike, and recently touched the lowest levels in weeks. …There are two main reasons for that weakness: Housing affordability is still brutal. Inventory is sitting. So instead of steady flatbed freight — lumber from mill to yard, yard to jobsite, jobsite to next jobsite — you get pauses. …Lumber and steel tell the truth before the broader market does.

Let’s keep this simple: lumber and steel are two of the biggest drivers of flatbed freight in this country. …So where are we right now, closing out 2025? Lumber futures are sliding off their highs and steel demand is soft with some pockets still running hot. That combination is sending a pretty clear message to flatbed haulers: expect mixed demand instead of broad “every lane is on fire” demand. Some regions will stay busy. Some will get quiet. …Lumber futures have fallen back into the $590–$610/mbf range, down double digits from that August spike, and recently touched the lowest levels in weeks. …There are two main reasons for that weakness: Housing affordability is still brutal. Inventory is sitting. So instead of steady flatbed freight — lumber from mill to yard, yard to jobsite, jobsite to next jobsite — you get pauses. …Lumber and steel tell the truth before the broader market does.  Before US President Donald Trump terminated trade negotiations with Canada late Thursday night, premiers were clashing over which tariff-beleaguered industries should be prioritized. Here’s a breakdown of the industries most under threat by tariffs in each province:

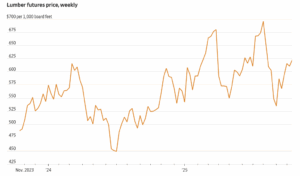

Before US President Donald Trump terminated trade negotiations with Canada late Thursday night, premiers were clashing over which tariff-beleaguered industries should be prioritized. Here’s a breakdown of the industries most under threat by tariffs in each province: Lumber futures tumbled toward $590 per thousand board feet, a near one-month low, as weakening US housing activity and pre-tariff front-loading left wholesalers awash with stock while stacked US duties on Canadian imports and trade uncertainty pushed prices lower. US homebuilding has slowed, with housing starts falling 8.5% in August to a 1.307 million annualized pace and building permits drifting lower. Many US buyers front-loaded inventories ahead of expected import tariffs earlier this autumn, leaving distributors to work down excess stock before fresh order flow returns. On the supply side, a 10% Section-232 tariff added in mid-October atop roughly 35% in existing duties lifted border costs above 45% for many Canadian shipments, forcing sellers to find new markets or accept lower domestic prices. Producers like Interfor have trimmed output since mid-October, but the cuts are too recent to significantly reduce inventories or regional log supply.

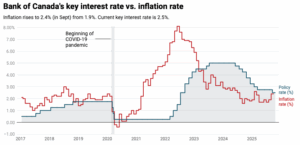

Lumber futures tumbled toward $590 per thousand board feet, a near one-month low, as weakening US housing activity and pre-tariff front-loading left wholesalers awash with stock while stacked US duties on Canadian imports and trade uncertainty pushed prices lower. US homebuilding has slowed, with housing starts falling 8.5% in August to a 1.307 million annualized pace and building permits drifting lower. Many US buyers front-loaded inventories ahead of expected import tariffs earlier this autumn, leaving distributors to work down excess stock before fresh order flow returns. On the supply side, a 10% Section-232 tariff added in mid-October atop roughly 35% in existing duties lifted border costs above 45% for many Canadian shipments, forcing sellers to find new markets or accept lower domestic prices. Producers like Interfor have trimmed output since mid-October, but the cuts are too recent to significantly reduce inventories or regional log supply. OTTAWA — Some economists say surprisingly strong September inflation figures will give the Bank of Canada pause ahead of its interest rate decision next week. Annual inflation accelerated to 2.4% last month, Statistics Canada said Tuesday. That’s a jump of half a percentage point from 1.9% in August and a tick higher than economists’ expectations. …The September inflation report will be the Bank of Canada’s last look at price data before the central bank’s next interest rate decision on Oct. 29. The central bank lowered its benchmark interest rate by a quarter point to 2.5% at its last decision in September. The Bank of Canada’s preferred measures of core inflation showed some stubbornness in September, holding above the three per cent mark. “This will make the Bank of Canada’s decision a bit more interesting next week than previously expected,” said BMO chief economist Doug Porter.

OTTAWA — Some economists say surprisingly strong September inflation figures will give the Bank of Canada pause ahead of its interest rate decision next week. Annual inflation accelerated to 2.4% last month, Statistics Canada said Tuesday. That’s a jump of half a percentage point from 1.9% in August and a tick higher than economists’ expectations. …The September inflation report will be the Bank of Canada’s last look at price data before the central bank’s next interest rate decision on Oct. 29. The central bank lowered its benchmark interest rate by a quarter point to 2.5% at its last decision in September. The Bank of Canada’s preferred measures of core inflation showed some stubbornness in September, holding above the three per cent mark. “This will make the Bank of Canada’s decision a bit more interesting next week than previously expected,” said BMO chief economist Doug Porter. Alain Ouzilleau, owner of Groupe Cabico, spent millions upgrading his two factories in Quebec and Ontario into state-of-the-art facilities shipping around $100-million worth of high-end kitchen cabinets to the US each year. Almost overnight, that business has been thrown into jeopardy. …“We have very long-term loyal customers,” Mr. Ouzilleau said. “But the 50% that is planned to be effective January 1st is just a death sentence.” …Hundreds of other Canadian cabinet and furniture makers also stand to lose their key export business, with limited ability to expand in a crowded domestic market. …What started as tariffs on steel, aluminum and automobiles has expanded to include copper and lumber, with a tariff on heavy trucks slated to come into force in November. The Trump administration is also conducting investigations into aircraft, semiconductors and industrial machinery, among other industries, suggesting more tariffs are on the horizon. [to access the full story a Globe & Mail subscription is required]

Alain Ouzilleau, owner of Groupe Cabico, spent millions upgrading his two factories in Quebec and Ontario into state-of-the-art facilities shipping around $100-million worth of high-end kitchen cabinets to the US each year. Almost overnight, that business has been thrown into jeopardy. …“We have very long-term loyal customers,” Mr. Ouzilleau said. “But the 50% that is planned to be effective January 1st is just a death sentence.” …Hundreds of other Canadian cabinet and furniture makers also stand to lose their key export business, with limited ability to expand in a crowded domestic market. …What started as tariffs on steel, aluminum and automobiles has expanded to include copper and lumber, with a tariff on heavy trucks slated to come into force in November. The Trump administration is also conducting investigations into aircraft, semiconductors and industrial machinery, among other industries, suggesting more tariffs are on the horizon. [to access the full story a Globe & Mail subscription is required] Lumber futures fell below $610 per thousand board feet, their lowest level since October 8 and down 12% from a three-year high in early August, as a slowing US housing market outweighed potential supply curbs from tariffs. August building permits dropped to a seasonally adjusted annualized rate of 1.33 million, the lowest since May 2020, while housing starts fell 8.5%, marking the fourth-lowest reading in over five years. Earlier this month, the US imposed a 10% tariff on Canadian lumber, with the Trump administration stating it aims to expand domestic timber harvesting and reduce reliance on foreign lumber. Looking ahead, expected Federal Reserve rate cuts could stimulate construction and home buying and encourage homeowners to borrow for repairs and renovations, the largest driver of lumber demand. However, signs of a slowing labor market and rising inflation suggest demand may remain subdued.

Lumber futures fell below $610 per thousand board feet, their lowest level since October 8 and down 12% from a three-year high in early August, as a slowing US housing market outweighed potential supply curbs from tariffs. August building permits dropped to a seasonally adjusted annualized rate of 1.33 million, the lowest since May 2020, while housing starts fell 8.5%, marking the fourth-lowest reading in over five years. Earlier this month, the US imposed a 10% tariff on Canadian lumber, with the Trump administration stating it aims to expand domestic timber harvesting and reduce reliance on foreign lumber. Looking ahead, expected Federal Reserve rate cuts could stimulate construction and home buying and encourage homeowners to borrow for repairs and renovations, the largest driver of lumber demand. However, signs of a slowing labor market and rising inflation suggest demand may remain subdued. The Canadian government has opened applications for a $700 million loan guarantee program that helps lumber companies weather mounting US tariffs that have pushed some firms into bankruptcy. The Business Development Bank of Canada

The Canadian government has opened applications for a $700 million loan guarantee program that helps lumber companies weather mounting US tariffs that have pushed some firms into bankruptcy. The Business Development Bank of Canada

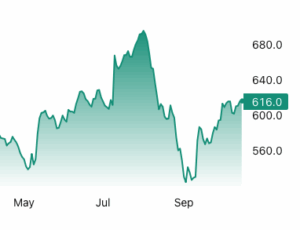

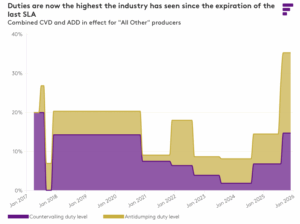

Lumber futures have risen about 19% from a low hit in early September, driven by the production cuts, hopes that declining interest rates will revive the housing market and Trump’s import tax. The 10% levy is on top of steep duties on Canadian lumber, which are adjusted annually in a heavily litigated process that is the result of a decades-long trade dispute. Those antidumping and countervailing duties rose in August to about 35% for most Canadian producers, up from roughly 15%. Canada’s sawmills are by far the largest source of softwood lumber from beyond U.S. borders, fulfilling about 24% of domestic consumption last year. Other significant importers of softwood lumber, the type used to frame houses, include Brazil and European countries such as Germany and Sweden. Homebuilders argue that import taxes will raise construction costs. U.S. lumber producers and timberland owners, however, urged Trump to enact a tariff.

Lumber futures have risen about 19% from a low hit in early September, driven by the production cuts, hopes that declining interest rates will revive the housing market and Trump’s import tax. The 10% levy is on top of steep duties on Canadian lumber, which are adjusted annually in a heavily litigated process that is the result of a decades-long trade dispute. Those antidumping and countervailing duties rose in August to about 35% for most Canadian producers, up from roughly 15%. Canada’s sawmills are by far the largest source of softwood lumber from beyond U.S. borders, fulfilling about 24% of domestic consumption last year. Other significant importers of softwood lumber, the type used to frame houses, include Brazil and European countries such as Germany and Sweden. Homebuilders argue that import taxes will raise construction costs. U.S. lumber producers and timberland owners, however, urged Trump to enact a tariff. Lumber futures rose past $610 per thousand board feet in mid-October, approaching monthly highs as markets priced in tighter near-term supply and looming trade restrictions. Under newly announced US Section 232 tariffs that take effect on October 14th, imported softwood lumber will face a 10% duty and finished wood goods such as cabinets and furniture will face higher levies, prompting importers to front-load purchases and draw down inventories. Domestic output is also constrained as sawmills run cautiously after years of underinvestment, logging curbs in sensitive regions and slow capacity restarts have limited production. The cost and delay of switching suppliers is material given that Canadian lumber, which supplies much of US demand, already carries elevated antidumping and countervailing duties, intensifying the supply squeeze.

Lumber futures rose past $610 per thousand board feet in mid-October, approaching monthly highs as markets priced in tighter near-term supply and looming trade restrictions. Under newly announced US Section 232 tariffs that take effect on October 14th, imported softwood lumber will face a 10% duty and finished wood goods such as cabinets and furniture will face higher levies, prompting importers to front-load purchases and draw down inventories. Domestic output is also constrained as sawmills run cautiously after years of underinvestment, logging curbs in sensitive regions and slow capacity restarts have limited production. The cost and delay of switching suppliers is material given that Canadian lumber, which supplies much of US demand, already carries elevated antidumping and countervailing duties, intensifying the supply squeeze. North America’s softwood lumber market looks likely to end 2025 no more settled than it was at the beginning. Producers and buyers alike continue navigating a landscape shaped by fluctuating demand, shifting trade patterns, and an uncertain housing outlook. Despite modest production declines in early 2025, the lumber market remains oversupplied. Mills across the US and Canada are contending with high inventories built up earlier in the year. Expectations of tariff hikes spurred an early rush of exports from Canada to the US, flooding the market while demand was soft. However, in the first half of 2025 softwood lumber exports from Canada to the US declined, while US imports from Europe in the first seven months of 2025 increased by 6% year-over-year. Underlying these supply pressures is a US housing market stuck in the doldrums. August saw an 8.5% decline in overall housing starts, with single-family construction down nearly 7%.

North America’s softwood lumber market looks likely to end 2025 no more settled than it was at the beginning. Producers and buyers alike continue navigating a landscape shaped by fluctuating demand, shifting trade patterns, and an uncertain housing outlook. Despite modest production declines in early 2025, the lumber market remains oversupplied. Mills across the US and Canada are contending with high inventories built up earlier in the year. Expectations of tariff hikes spurred an early rush of exports from Canada to the US, flooding the market while demand was soft. However, in the first half of 2025 softwood lumber exports from Canada to the US declined, while US imports from Europe in the first seven months of 2025 increased by 6% year-over-year. Underlying these supply pressures is a US housing market stuck in the doldrums. August saw an 8.5% decline in overall housing starts, with single-family construction down nearly 7%. President Trump unveiled sweeping tariffs on imported lumber and wood products that his administration says are needed to protect the US economy and boost domestic manufacturing. Starting Oct. 14, softwood lumber will face 10% duties, while kitchen cabinets, bathroom vanities, and other finished wood goods will be hit with 25% tariffs that rise further in January. The biggest blow will fall on Canada, the US’s top lumber supplier, whose lumber exports are already subject to separate duties totaling 35.19%. …Though Canada dominates exports of lumber to the US, many other countries export wood products to the US. The Section 232 tariffs on lumber and wood products affect them in varying ways; some countries benefit from trade deals with the US that cap the rates, and others bear the full brunt. …Though lumber accounts for less than 20% of building costs, the National Association of Homebuilders has long said that restrictions on Canadian lumber translate to higher construction costs. [to access the full story a Bloomberg subscription is required]

President Trump unveiled sweeping tariffs on imported lumber and wood products that his administration says are needed to protect the US economy and boost domestic manufacturing. Starting Oct. 14, softwood lumber will face 10% duties, while kitchen cabinets, bathroom vanities, and other finished wood goods will be hit with 25% tariffs that rise further in January. The biggest blow will fall on Canada, the US’s top lumber supplier, whose lumber exports are already subject to separate duties totaling 35.19%. …Though Canada dominates exports of lumber to the US, many other countries export wood products to the US. The Section 232 tariffs on lumber and wood products affect them in varying ways; some countries benefit from trade deals with the US that cap the rates, and others bear the full brunt. …Though lumber accounts for less than 20% of building costs, the National Association of Homebuilders has long said that restrictions on Canadian lumber translate to higher construction costs. [to access the full story a Bloomberg subscription is required] Canada’s international trade deficit swelled to $6.3 billion in August, its second-largest shortfall on record, as new United States tariffs took a heavy toll on key exports and injected fresh volatility into cross-border flows. The latest figures, released by Statistics Canada, show how US trade policy continues to affect Canadian exporters and make the Bank of Canada’s next interest rate decision more complicated. Exports in August fell 3% by value and 3.2% in volume, led by sharp declines in copper ore and lumber shipments, both of which were hit by new US tariffs. …Imports, meanwhile, rose 0.9%, buoyed by higher consumer goods, a sign of resilient household demand, even as business investment remained soft. …Exports to the US, Canada’s largest trading partner, fell 3.4% in August after three consecutive monthly gains, and were down 8% year-over-year. Exports to non-US destinations edged up 1.8% from a year ago but slipped 2% from July.

Canada’s international trade deficit swelled to $6.3 billion in August, its second-largest shortfall on record, as new United States tariffs took a heavy toll on key exports and injected fresh volatility into cross-border flows. The latest figures, released by Statistics Canada, show how US trade policy continues to affect Canadian exporters and make the Bank of Canada’s next interest rate decision more complicated. Exports in August fell 3% by value and 3.2% in volume, led by sharp declines in copper ore and lumber shipments, both of which were hit by new US tariffs. …Imports, meanwhile, rose 0.9%, buoyed by higher consumer goods, a sign of resilient household demand, even as business investment remained soft. …Exports to the US, Canada’s largest trading partner, fell 3.4% in August after three consecutive monthly gains, and were down 8% year-over-year. Exports to non-US destinations edged up 1.8% from a year ago but slipped 2% from July. Canada’s merchandise trade deficit widened in August to C$6.32 billion ($4.53 billion) as exports fell faster in both value and volume than the rise in imports on a monthly basis, official government statistics showed on Tuesday. The trade deficit in August was led by drop in exports not only to its top trading partner the U.S. but also because its shipments to the rest of the world shrank in the month. Canada’s international trade numbers took a beating early this year as US President Trump imposed sectoral tariffs on the country, forcing businesses to reorient supply chain from its biggest trading partner. But the shift has been volatile and erratic. Analysts polled by Reuters had forecast the August trade deficit at C$5.55 billion, up from an upwardly revised C$3.82 billion in the prior month. Total exports dropped by 3% while imports increased 0.9%, StatsCan said.

Canada’s merchandise trade deficit widened in August to C$6.32 billion ($4.53 billion) as exports fell faster in both value and volume than the rise in imports on a monthly basis, official government statistics showed on Tuesday. The trade deficit in August was led by drop in exports not only to its top trading partner the U.S. but also because its shipments to the rest of the world shrank in the month. Canada’s international trade numbers took a beating early this year as US President Trump imposed sectoral tariffs on the country, forcing businesses to reorient supply chain from its biggest trading partner. But the shift has been volatile and erratic. Analysts polled by Reuters had forecast the August trade deficit at C$5.55 billion, up from an upwardly revised C$3.82 billion in the prior month. Total exports dropped by 3% while imports increased 0.9%, StatsCan said. It’s hard to find anything good to say about Canadian forestry stocks right now. Some of the biggest names in the sector have been on a downward slide for the past three years. … But the onslaught of grim news has highlighted some bargains. …Okay, the definition of attractive rests on an assumption that risk-averse investors might not want to embrace just yet: Despite Mr. Trump’s bluster, the US still needs Canadian lumber in a big way to feed its lumber-intensive home construction industry. Says who? The National Association of Home Builders, for one. …Some analysts believe that US forestry companies will struggle to replace Canadian softwood. Ben Isaacson, at Bank of Nova Scotia, estimates that US producers would have to build 50 new mills to become fully independent of Canadian lumber. Just two companies build the specialized equipment required in mills. They would struggle to supply even two mills a year. [to access the full story a Globe & Mail subscription is required]

It’s hard to find anything good to say about Canadian forestry stocks right now. Some of the biggest names in the sector have been on a downward slide for the past three years. … But the onslaught of grim news has highlighted some bargains. …Okay, the definition of attractive rests on an assumption that risk-averse investors might not want to embrace just yet: Despite Mr. Trump’s bluster, the US still needs Canadian lumber in a big way to feed its lumber-intensive home construction industry. Says who? The National Association of Home Builders, for one. …Some analysts believe that US forestry companies will struggle to replace Canadian softwood. Ben Isaacson, at Bank of Nova Scotia, estimates that US producers would have to build 50 new mills to become fully independent of Canadian lumber. Just two companies build the specialized equipment required in mills. They would struggle to supply even two mills a year. [to access the full story a Globe & Mail subscription is required] Although we are skeptical how effective the C$500 million in “transition” funding will be, the C$700 million in loan guarantees, which are clearly designed as a short-term lifeline for companies to weather the storm, seem pretty meaningful to the Canadian industry at first glance. …If Canadian producers were to simply absorb the incremental duty rate increase, using today’s FOB price for most Canadian softwood lumber and last year’s export volumes to the US translates to a “just pay it” cost of C$1.6-1.7 billion in additional duty payments over the next 12 months. Canadian mill operators are not in a financial position to simply absorb an additional 21-percentage-point increase in duties, so this is an extreme estimate of the true cost. Mills will curtail output rather than continue producing at heavy losses until prices adjust accordingly. Additionally, there is usually some degree of passthrough from the buyer to the seller.

Although we are skeptical how effective the C$500 million in “transition” funding will be, the C$700 million in loan guarantees, which are clearly designed as a short-term lifeline for companies to weather the storm, seem pretty meaningful to the Canadian industry at first glance. …If Canadian producers were to simply absorb the incremental duty rate increase, using today’s FOB price for most Canadian softwood lumber and last year’s export volumes to the US translates to a “just pay it” cost of C$1.6-1.7 billion in additional duty payments over the next 12 months. Canadian mill operators are not in a financial position to simply absorb an additional 21-percentage-point increase in duties, so this is an extreme estimate of the true cost. Mills will curtail output rather than continue producing at heavy losses until prices adjust accordingly. Additionally, there is usually some degree of passthrough from the buyer to the seller. The softwood lumber trade dispute between the US and Canada, which has led to ever-higher US import duties on Canadian lumber, has lasted for decades. …Canadian lumber has the backing NAHB, which sees lumber tariffs as exacerbating high costs for builders and worsening the US housing affordability crisis. There is currently a “Wall of Wood” in the US, after Canadian producers increased shipments to the US in anticipation of the hike to existing ADD and CVD duties in August. Expectations that a large increase in duties would force the closure of Canadian sawmills, lead to shortages, and a boost in lumber prices, overlooked the current weak US demand for lumber, according to Matt Layman. …As US homebuilders now face additional tariff-driven costs, including a 50% tariff on cabinets and vanities, it’s hard to see the lumber demand situation improving, even if more Canadian suppliers have to curtail production or close sawmills.

The softwood lumber trade dispute between the US and Canada, which has led to ever-higher US import duties on Canadian lumber, has lasted for decades. …Canadian lumber has the backing NAHB, which sees lumber tariffs as exacerbating high costs for builders and worsening the US housing affordability crisis. There is currently a “Wall of Wood” in the US, after Canadian producers increased shipments to the US in anticipation of the hike to existing ADD and CVD duties in August. Expectations that a large increase in duties would force the closure of Canadian sawmills, lead to shortages, and a boost in lumber prices, overlooked the current weak US demand for lumber, according to Matt Layman. …As US homebuilders now face additional tariff-driven costs, including a 50% tariff on cabinets and vanities, it’s hard to see the lumber demand situation improving, even if more Canadian suppliers have to curtail production or close sawmills.

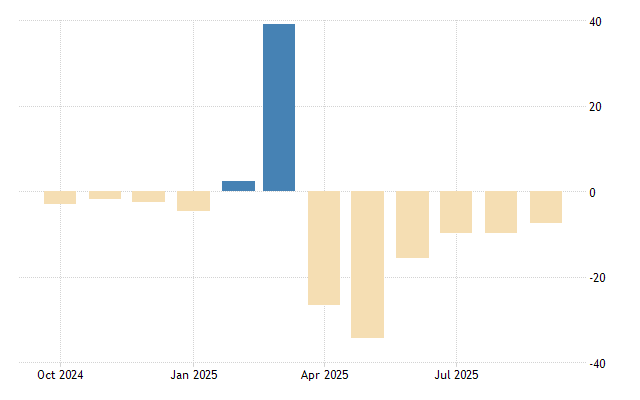

Canada’s merchandise exports fell by three per cent in August to a seasonally adjusted $60.5 billion. This was the second lowest month of the year after April as sales to the U.S. retreated. Imports rose by 0.9 per cent to a seasonally adjusted $66.9 billion during the month. Consequently, the trade deficit grew to $6.3 billion, down from a revised $3.8 billion in July. …The decline was led by a 21.2 per cent drop in forestry products and a 12.5 per cent decline in energy products. The steep decline in forestry products in August 2025 followed the increase of anti-dumping and countervailing duty rates on Canadian softwood lumber that took effect in the U.S. in late July and early August. Section 232 tariffs on lumber in effect in October will be a further headwind. …Year-to-date exports are down slightly (-0.1 per cent) with lower forestry products and building and packaging materials exports (-6.1 per cent)

Canada’s merchandise exports fell by three per cent in August to a seasonally adjusted $60.5 billion. This was the second lowest month of the year after April as sales to the U.S. retreated. Imports rose by 0.9 per cent to a seasonally adjusted $66.9 billion during the month. Consequently, the trade deficit grew to $6.3 billion, down from a revised $3.8 billion in July. …The decline was led by a 21.2 per cent drop in forestry products and a 12.5 per cent decline in energy products. The steep decline in forestry products in August 2025 followed the increase of anti-dumping and countervailing duty rates on Canadian softwood lumber that took effect in the U.S. in late July and early August. Section 232 tariffs on lumber in effect in October will be a further headwind. …Year-to-date exports are down slightly (-0.1 per cent) with lower forestry products and building and packaging materials exports (-6.1 per cent) EDMUNDSTON, New Brunswick – Acadian Timber reported financial and operating results1 for the three months ended September 27, 2025. Acadian generated sales of $23.0 million, compared to $26.0 million in the prior year period. …Operating costs and expenses decreased $2.0 million compared to the prior year period as a result of decreased timber sales volumes and timber services activity, partially offset by higher average operating costs and expenses per m

EDMUNDSTON, New Brunswick – Acadian Timber reported financial and operating results1 for the three months ended September 27, 2025. Acadian generated sales of $23.0 million, compared to $26.0 million in the prior year period. …Operating costs and expenses decreased $2.0 million compared to the prior year period as a result of decreased timber sales volumes and timber services activity, partially offset by higher average operating costs and expenses per m An extended slowdown in sales of cardboard boxes is intensifying concern that this holiday season will be a disappointing one for US retailers. US corrugated box shipments fell to the lowest third-quarter reading since 2015, maintaining the more measured pace seen in the previous quarter, according to the Fibre Box Association. Packaging companies in recent weeks have warned that economic uncertainty is weighing on retailers and consumers. …This time of year is crucial for the box industry, with shipments typically peaking in October as retailers prepare for the holidays. Box plants said orders were flat or below normal in October, while US consumer sentiment fell to a five-month low and manufacturing activity dropped for an eighth straight month. …US box industry shipments are poised to drop 1% to 1.5% this year versus 2024,” IP’s Andy Silvernail said last week. [to access the full story a Bloomberg subscription is required]

An extended slowdown in sales of cardboard boxes is intensifying concern that this holiday season will be a disappointing one for US retailers. US corrugated box shipments fell to the lowest third-quarter reading since 2015, maintaining the more measured pace seen in the previous quarter, according to the Fibre Box Association. Packaging companies in recent weeks have warned that economic uncertainty is weighing on retailers and consumers. …This time of year is crucial for the box industry, with shipments typically peaking in October as retailers prepare for the holidays. Box plants said orders were flat or below normal in October, while US consumer sentiment fell to a five-month low and manufacturing activity dropped for an eighth straight month. …US box industry shipments are poised to drop 1% to 1.5% this year versus 2024,” IP’s Andy Silvernail said last week. [to access the full story a Bloomberg subscription is required] Kimberly-Clark is buying Tylenol maker Kenvue in a cash and stock deal worth about $48.7 billion, creating a massive consumer health goods company. Shareholders of Kimberly-Clark will own about 54% of the combined company. Kenvue shareholders will own about 46%. The combined company will have a large stable of household brands under one roof, putting Kenvue’s Listerine mouthwash and Band-Aid side-by-side with Kimberly-Clark’s Cottonelle toilet paper, Huggies and Kleenex tissues. It will also generate about $32 billion in annual revenue. Kenvue has spent a relatively brief period as an independent company, having been spun off by Johnson & Johnson two years ago. The deal announced Monday is among the largest corporate takeovers of the year. …The deal is expected to close in the second half of next year. It still needs approval from shareholders of both both companies. …Shares of Kimberly-Clark slipped more than 15% before the market open, while Kenvue’s stock jumped more than 20%.

Kimberly-Clark is buying Tylenol maker Kenvue in a cash and stock deal worth about $48.7 billion, creating a massive consumer health goods company. Shareholders of Kimberly-Clark will own about 54% of the combined company. Kenvue shareholders will own about 46%. The combined company will have a large stable of household brands under one roof, putting Kenvue’s Listerine mouthwash and Band-Aid side-by-side with Kimberly-Clark’s Cottonelle toilet paper, Huggies and Kleenex tissues. It will also generate about $32 billion in annual revenue. Kenvue has spent a relatively brief period as an independent company, having been spun off by Johnson & Johnson two years ago. The deal announced Monday is among the largest corporate takeovers of the year. …The deal is expected to close in the second half of next year. It still needs approval from shareholders of both both companies. …Shares of Kimberly-Clark slipped more than 15% before the market open, while Kenvue’s stock jumped more than 20%.

Shares of D.R. Horton took a hit Tuesday, as the home builder confirmed that the market for new houses was still weak, and it wasn’t just because prices and mortgage rates were too high — people are afraid to shell out so much for a new house when they’re worried about the economy and their jobs. …But even with lower prices and mortgage rates, the number of homes closed fell 1.2% to 23,368, which was below the average analyst estimate. And that weakness comes despite higher incentives to home buyers to boost sales, which pushed profits below what Wall Street was expecting. …Chief Executive Paul Romanowski said affordability was certainly still an issue. But consumers were also concerned about the “volatility and uncertainty” in the economy, which may be leading to worries about the job market. It certainly won’t help matters to see large layoff announcements from high-profile companies.

Shares of D.R. Horton took a hit Tuesday, as the home builder confirmed that the market for new houses was still weak, and it wasn’t just because prices and mortgage rates were too high — people are afraid to shell out so much for a new house when they’re worried about the economy and their jobs. …But even with lower prices and mortgage rates, the number of homes closed fell 1.2% to 23,368, which was below the average analyst estimate. And that weakness comes despite higher incentives to home buyers to boost sales, which pushed profits below what Wall Street was expecting. …Chief Executive Paul Romanowski said affordability was certainly still an issue. But consumers were also concerned about the “volatility and uncertainty” in the economy, which may be leading to worries about the job market. It certainly won’t help matters to see large layoff announcements from high-profile companies.

Section 232 tariffs were once seen as a fortress for US metals. Yet, that fortress now casts a much longer shadow. Companies far removed from the steel and aluminum sector could soon find themselves ensnared in tariffs they never imagined, thanks to the inclusion process for “derivative” products. The Trump Administration has steadily expanded Section 232 authority well beyond their original steel and aluminum targets, to copper, automobiles, trucks, lumber, and even wooden cabinets. These tariffs, which range from 10% (for lumber) to 50% (for steel and aluminum), are layered on top of normal import duties. At first glance, these measures appeared to strike only those industries handling raw materials. But in 2025 the Administration sought to close what it saw as a loophole: downstream products containing tariffed metals that could enter duty-free. As a result, section 232 tariffs were imposed on the raw material and a finite list of derivative products.

Section 232 tariffs were once seen as a fortress for US metals. Yet, that fortress now casts a much longer shadow. Companies far removed from the steel and aluminum sector could soon find themselves ensnared in tariffs they never imagined, thanks to the inclusion process for “derivative” products. The Trump Administration has steadily expanded Section 232 authority well beyond their original steel and aluminum targets, to copper, automobiles, trucks, lumber, and even wooden cabinets. These tariffs, which range from 10% (for lumber) to 50% (for steel and aluminum), are layered on top of normal import duties. At first glance, these measures appeared to strike only those industries handling raw materials. But in 2025 the Administration sought to close what it saw as a loophole: downstream products containing tariffed metals that could enter duty-free. As a result, section 232 tariffs were imposed on the raw material and a finite list of derivative products. Ikea is increasing the amount of products it makes in the US as the world’s largest home furnishings retailer comes under pressure from US President Donald Trump’s tariffs on furniture and kitchen cabinets. The flat-pack retailer, which made revenues of $5.5bn in the US last year, currently produces only about 15% of products that it sells in the US domestically. That compares with 75% local production in Europe and 80% in Asia. “We want to continue to expand in the US and Canada — how do we optimise a good supply set-up where we secure the right access to materials, to components, to production? That’s very long-term work that we’re doing,” Jon Abrahamsson Ring, chief executive of Inter Ikea. Trump imposed tariffs of between 10% and 50% on imports of foreign furniture and wood products. Ikea, which is responsible for about 1% of total industrial production, is set to take a significant hit.

Ikea is increasing the amount of products it makes in the US as the world’s largest home furnishings retailer comes under pressure from US President Donald Trump’s tariffs on furniture and kitchen cabinets. The flat-pack retailer, which made revenues of $5.5bn in the US last year, currently produces only about 15% of products that it sells in the US domestically. That compares with 75% local production in Europe and 80% in Asia. “We want to continue to expand in the US and Canada — how do we optimise a good supply set-up where we secure the right access to materials, to components, to production? That’s very long-term work that we’re doing,” Jon Abrahamsson Ring, chief executive of Inter Ikea. Trump imposed tariffs of between 10% and 50% on imports of foreign furniture and wood products. Ikea, which is responsible for about 1% of total industrial production, is set to take a significant hit.

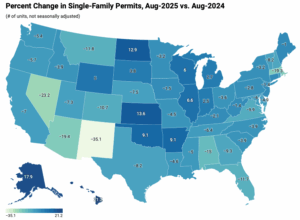

In August, single-family permit activity softened, reflecting caution among developers amid persistent economic headwinds. This trend has been consistent for eight continuous months. On the multifamily front, permitting also cooled in August but remains in the positive territory. While single-family continues to bear the brunt of affordability headwinds, the multifamily space is showing tentative signs of rebalancing. Over the first eight months of 2025, the total number of single-family permits issued year-to-date (YTD) nationwide reached 637,096. On a year-over-year (YoY) basis, this is a decline of 7.1% over the August 2024 level of 685,923. For multifamily, the total number of permits issued nationwide reached 330,617. This is 1.4% higher compared to the August 2024 level of 326,080. HBGI analysis indicates that this growth for multifamily development has been concentrated in lower density areas and among smaller builders.

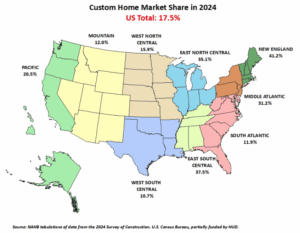

In August, single-family permit activity softened, reflecting caution among developers amid persistent economic headwinds. This trend has been consistent for eight continuous months. On the multifamily front, permitting also cooled in August but remains in the positive territory. While single-family continues to bear the brunt of affordability headwinds, the multifamily space is showing tentative signs of rebalancing. Over the first eight months of 2025, the total number of single-family permits issued year-to-date (YTD) nationwide reached 637,096. On a year-over-year (YoY) basis, this is a decline of 7.1% over the August 2024 level of 685,923. For multifamily, the total number of permits issued nationwide reached 330,617. This is 1.4% higher compared to the August 2024 level of 326,080. HBGI analysis indicates that this growth for multifamily development has been concentrated in lower density areas and among smaller builders. In 2024, 17.5% of all new single-family homes started were custom homes. This share decreased from 18.8% in 2023 and from 20.4% in 2022, according to data tabulated from the Census Bureau’s Survey of Construction (SOC). The custom home market consists of contractor-built and owner-built homes—homes built for owner occupancy on the owner’s land, with either the owner or a builder acting as a general contractor. The alternatives are homes built-for-sale (on the builder’s land, often in subdivisions, with the intention of selling the house and land in one transaction) and homes built-for-rent. In 2024, 73.1% of the single-family homes started were built-for-sale and 9.3% were built-for-rent. At a 17.5% share, the number of custom homes started in 2024 was 176,932, falling from 177,850 in 2023.

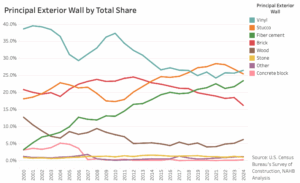

In 2024, 17.5% of all new single-family homes started were custom homes. This share decreased from 18.8% in 2023 and from 20.4% in 2022, according to data tabulated from the Census Bureau’s Survey of Construction (SOC). The custom home market consists of contractor-built and owner-built homes—homes built for owner occupancy on the owner’s land, with either the owner or a builder acting as a general contractor. The alternatives are homes built-for-sale (on the builder’s land, often in subdivisions, with the intention of selling the house and land in one transaction) and homes built-for-rent. In 2024, 73.1% of the single-family homes started were built-for-sale and 9.3% were built-for-rent. At a 17.5% share, the number of custom homes started in 2024 was 176,932, falling from 177,850 in 2023. In 2024, vinyl siding was the most used principal exterior wall material for homes started. It holds just over a quarter share of homes, slightly surpassing stucco for the first time since 2018. …Vinyl was followed closely by stucco at 25%, and by fiber cement siding (such as Hardiplank or Hardiboard) at 23%. Each of these materials holds about a quarter of the market, with another 16% held by brick or brick veneer. Far smaller shares of single-family homes had wood or wood products (6%), stone, rock or other stone materials (1%), other (1%), or cement blocks (.2%) as the principal exterior wall material. …The strongest trend has been the growing popularity in fiber cement siding. The share of exterior siding material for fiber cement siding has increased by 5.5 percentage points in the last ten years…. Also notable is the decline of brick siding, from almost a quarter of homes in 2012, to just 16% in 2024.

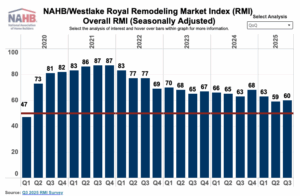

In 2024, vinyl siding was the most used principal exterior wall material for homes started. It holds just over a quarter share of homes, slightly surpassing stucco for the first time since 2018. …Vinyl was followed closely by stucco at 25%, and by fiber cement siding (such as Hardiplank or Hardiboard) at 23%. Each of these materials holds about a quarter of the market, with another 16% held by brick or brick veneer. Far smaller shares of single-family homes had wood or wood products (6%), stone, rock or other stone materials (1%), other (1%), or cement blocks (.2%) as the principal exterior wall material. …The strongest trend has been the growing popularity in fiber cement siding. The share of exterior siding material for fiber cement siding has increased by 5.5 percentage points in the last ten years…. Also notable is the decline of brick siding, from almost a quarter of homes in 2012, to just 16% in 2024. In the third quarter of 2025, the NAHB/Westlake Royal Remodeling Market Index (RMI) posted a reading of 60, up one point compared to the previous quarter. With the reading of 60, the RMI remains solidly in positive territory above 50, but lower than it had been at any time from 2021 through 2024. Overall, remodelers remain optimistic about the market, although slightly less optimistic than they were at this time last year. The most significant headwinds they are facing include high material and labor costs, as well as economic and political uncertainty making some of their potential customers cautious about moving forward with remodeling projects. The small quarter-over-quarter improvement is consistent with flat construction spending trends and the current wait-and-see demand environment.

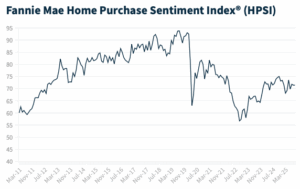

In the third quarter of 2025, the NAHB/Westlake Royal Remodeling Market Index (RMI) posted a reading of 60, up one point compared to the previous quarter. With the reading of 60, the RMI remains solidly in positive territory above 50, but lower than it had been at any time from 2021 through 2024. Overall, remodelers remain optimistic about the market, although slightly less optimistic than they were at this time last year. The most significant headwinds they are facing include high material and labor costs, as well as economic and political uncertainty making some of their potential customers cautious about moving forward with remodeling projects. The small quarter-over-quarter improvement is consistent with flat construction spending trends and the current wait-and-see demand environment. WASHINGTON, DC – Fannie Mae published the results of its September 2025

WASHINGTON, DC – Fannie Mae published the results of its September 2025  President Donald Trump has reignited debate over the nation’s housing shortage, calling on Fannie Mae and Freddie Mac to spur a wave of new home construction. Trump accused large homebuilders of “sitting on 2 million empty lots, a record,” and likened their behavior to OPEC’s control of oil prices. …“I’m asking Fannie Mae and Freddie Mac to get Big Homebuilders going and, by so doing, help restore the American Dream!” The president’s comments come as housing inventory has rebounded from historic lows in 2022, but builders continue to face limited incentives to ramp up construction. …Since taking office, Trump has made housing a central policy focus, including an executive order for emergency price relief and a campaign to pressure the Federal Reserve for lower rates. …Despite Trump’s calls, the mechanics of how Fannie and Freddie might spur more homebuilding remain unclear.

President Donald Trump has reignited debate over the nation’s housing shortage, calling on Fannie Mae and Freddie Mac to spur a wave of new home construction. Trump accused large homebuilders of “sitting on 2 million empty lots, a record,” and likened their behavior to OPEC’s control of oil prices. …“I’m asking Fannie Mae and Freddie Mac to get Big Homebuilders going and, by so doing, help restore the American Dream!” The president’s comments come as housing inventory has rebounded from historic lows in 2022, but builders continue to face limited incentives to ramp up construction. …Since taking office, Trump has made housing a central policy focus, including an executive order for emergency price relief and a campaign to pressure the Federal Reserve for lower rates. …Despite Trump’s calls, the mechanics of how Fannie and Freddie might spur more homebuilding remain unclear.  President Trump’s latest round of tariffs aimed at wood, furniture and other household furnishings could drive up the cost of building and owning homes, further weighing on an already weak housing sector. Analysts said the steep levies could aggravate the nationwide housing shortage by slowing the pace of new home construction. The higher costs, as well as hefty tariffs on steel and aluminum that went into effect in June, could also dampen any jolt the housing market might have derived as the Federal Reserve begins to lower interest rates. …“These tariffs are really hard to understand given that the president has said to his supporters, ‘I want to bring down inflation, I want to bring down interest rates,’” said Anirban Basu, at the Associated Builders and Contractors. …And there could be ripple effects, including higher prices for home insurance because houses and their components would cost more to replace. [to access the full story a NY Times subscription is required]

President Trump’s latest round of tariffs aimed at wood, furniture and other household furnishings could drive up the cost of building and owning homes, further weighing on an already weak housing sector. Analysts said the steep levies could aggravate the nationwide housing shortage by slowing the pace of new home construction. The higher costs, as well as hefty tariffs on steel and aluminum that went into effect in June, could also dampen any jolt the housing market might have derived as the Federal Reserve begins to lower interest rates. …“These tariffs are really hard to understand given that the president has said to his supporters, ‘I want to bring down inflation, I want to bring down interest rates,’” said Anirban Basu, at the Associated Builders and Contractors. …And there could be ripple effects, including higher prices for home insurance because houses and their components would cost more to replace. [to access the full story a NY Times subscription is required]

Anthony Cabrera, who started working with a contractor in March to construct the three-bedroom house, was eager to get ahead of a fresh round of tariffs on key building materials and home items that took effect earlier this week. Mr Cabrera had already seen his initial budget of roughly $300,000 balloon to $450,000 as prices for a range of products. …A recent report from Goldman Sachs found that US consumers will shoulder as much as 55% of the cost. It takes time to raise prices on consumers, the economists noted, and US firms will increasingly pass on costs in the coming months. The new tariffs “will create additional headwinds for an already challenged housing market” Buddy Hughes, chairman for the NAHB, said. Affordable housing construction could be hit particularly hard, said Elena Patel, of the Urban-Brookings Tax Policy Center. …Matthew Walsh, at Moody’s Analytics, said that cost uncertainty will be the most immediate effect.

Anthony Cabrera, who started working with a contractor in March to construct the three-bedroom house, was eager to get ahead of a fresh round of tariffs on key building materials and home items that took effect earlier this week. Mr Cabrera had already seen his initial budget of roughly $300,000 balloon to $450,000 as prices for a range of products. …A recent report from Goldman Sachs found that US consumers will shoulder as much as 55% of the cost. It takes time to raise prices on consumers, the economists noted, and US firms will increasingly pass on costs in the coming months. The new tariffs “will create additional headwinds for an already challenged housing market” Buddy Hughes, chairman for the NAHB, said. Affordable housing construction could be hit particularly hard, said Elena Patel, of the Urban-Brookings Tax Policy Center. …Matthew Walsh, at Moody’s Analytics, said that cost uncertainty will be the most immediate effect. China’s pulp and paper industry continues to expand at an unprecedented pace, with new mill projects, advanced technologies, and state-backed financing driving record output. What began as a push to meet domestic demand has now evolved into an era of overcapacity and a structural imbalance that is reshaping trade dynamics, pricing strategies, and sustainability priorities worldwide. This expansion has far-reaching effects: global producers are contending with lower-priced exports, disrupted supply chains, and a shifting balance of power that challenges traditional market leaders in North America and Europe. …Industry observers expect consolidation in China’s pulp and paper sector, as smaller and less efficient mills struggle to survive. Strategic investments in transparency, benchmarking, and efficiency will be crucial for staying competitive in a tightening global market.

China’s pulp and paper industry continues to expand at an unprecedented pace, with new mill projects, advanced technologies, and state-backed financing driving record output. What began as a push to meet domestic demand has now evolved into an era of overcapacity and a structural imbalance that is reshaping trade dynamics, pricing strategies, and sustainability priorities worldwide. This expansion has far-reaching effects: global producers are contending with lower-priced exports, disrupted supply chains, and a shifting balance of power that challenges traditional market leaders in North America and Europe. …Industry observers expect consolidation in China’s pulp and paper sector, as smaller and less efficient mills struggle to survive. Strategic investments in transparency, benchmarking, and efficiency will be crucial for staying competitive in a tightening global market. The UK timber industry is currently experiencing a crisis, even as it reports record sales of softwood, raising concerns over supply chain challenges, rising costs, and sustainability issues. The surge in softwood sales, particularly in the construction and woodworking sectors, has overshadowed the ongoing difficulties facing the industry. While the demand for timber has been high, particularly due to the growing construction boom and a shift toward more sustainable building materials, the challenges related to timber shortages and price increases remain deeply concerning for businesses across the sector. …The Timber Trade Federation (TTF) reports that softwood sales in the UK reached record levels in 2024. However, one of the most pressing issues facing the UK timber sector is the disruption of supply chains. The UK has faced considerable difficulty in securing a steady supply of raw timber. The global timber shortage has exacerbated the situation.

The UK timber industry is currently experiencing a crisis, even as it reports record sales of softwood, raising concerns over supply chain challenges, rising costs, and sustainability issues. The surge in softwood sales, particularly in the construction and woodworking sectors, has overshadowed the ongoing difficulties facing the industry. While the demand for timber has been high, particularly due to the growing construction boom and a shift toward more sustainable building materials, the challenges related to timber shortages and price increases remain deeply concerning for businesses across the sector. …The Timber Trade Federation (TTF) reports that softwood sales in the UK reached record levels in 2024. However, one of the most pressing issues facing the UK timber sector is the disruption of supply chains. The UK has faced considerable difficulty in securing a steady supply of raw timber. The global timber shortage has exacerbated the situation.