Kevin Mason

Having spent the past two months in freefall, lumber prices have found a near-term price floor. Western S-P-F 2×4 prices declined from $1,090 in early May to a low of $555 in mid-June, but have since rebounded to $600. SYP 2×4 prices corrected much earlier than S-P-F and thus had less room to fall this quarter, but they are still off by $274 since early May (trading at $560 last week). The correction in lumber prices this quarter has been driven by a combination of improved supply and slowing demand from the residential construction sector. While the outlook for demand, and particularly residential construction, remains shaky, we do expect lumber supply to also check back in high-cost BC.

A look at our regional lumber margin comparison table shows just how challenging BC sawmilling economics have become. …When government stumpage rates increase in BC next week, we think log costs will rise by up to US$25/m3, effectively adding more than $100/mbf to total lumber production costs. This will push our theoretical breakeven lumber price above $600 for BC producers, even before factoring in the impact of duties. For less efficient mills with a weaker lumber recovery factor (i.e., the volume of logs required to produce one thousand board feet of lumber) and higher conversion costs, that breakeven price point could be comfortably above $650 in the quarters to come. In the U.S. South, delivered sawlog prices have risen from ~$43/ton to ~$48/ton in the past couple of years. While we expect them to continue grinding higher in the years to come, southern mills’ log costs remain less than half of those in BC.

BC’s pending stumpage increase shows just how challenging BC sawmilling economics have become: ERA. In related news: US and Canadian housing-starts scale back; and tissue production shows solid growth. In other Business news: Mercer provides update on fire at Stendal pulp mill; and pundits weigh in on Premier Horgan’s retirement and what it means for the NDP.

BC’s pending stumpage increase shows just how challenging BC sawmilling economics have become: ERA. In related news: US and Canadian housing-starts scale back; and tissue production shows solid growth. In other Business news: Mercer provides update on fire at Stendal pulp mill; and pundits weigh in on Premier Horgan’s retirement and what it means for the NDP.

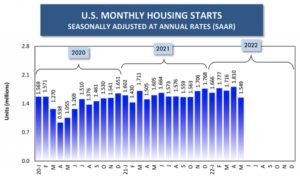

Triggered by mortgage rate increases, expectations concerning housing starts in the U.S. and Canada have been scaled back. Nevertheless, the starts statistics are holding up not too badly to this point in time. In the U.S., the monthly average of unit groundbreakings has increased by +8.5% year to date, although the latest monthly level was -14.4% compared with the previous month, falling from 1.810 million units in April to 1.549 million units in May. Upcoming June’s results will make clearer whether there is still support for a decent number of starts this year. In Canada, the monthly average is -12.4% year to date compared with Jan-May 2021, but the individual month of May was quite strong, 287,000 units SAAR. The 287,000 number was the highest in any month so far in 2022 and the best since November of last, when 306,000 units were initiated.

Triggered by mortgage rate increases, expectations concerning housing starts in the U.S. and Canada have been scaled back. Nevertheless, the starts statistics are holding up not too badly to this point in time. In the U.S., the monthly average of unit groundbreakings has increased by +8.5% year to date, although the latest monthly level was -14.4% compared with the previous month, falling from 1.810 million units in April to 1.549 million units in May. Upcoming June’s results will make clearer whether there is still support for a decent number of starts this year. In Canada, the monthly average is -12.4% year to date compared with Jan-May 2021, but the individual month of May was quite strong, 287,000 units SAAR. The 287,000 number was the highest in any month so far in 2022 and the best since November of last, when 306,000 units were initiated. US parent roll production increased +7.7% y/y – According to RISI, US parent roll production increased by 58k tons y/y to 815k tons, while tissue mill capacity was up 4k tons y/y to 872k tons, increasing the US industry operating rate to 93.5% vs. 87.2% last year. However, the US industry operating rate decreased by 0.7 percentage points m/m, as production increased by 20k tons m/m, while capacity increased by 28k tons m/m. …Other RISI findings include:

US parent roll production increased +7.7% y/y – According to RISI, US parent roll production increased by 58k tons y/y to 815k tons, while tissue mill capacity was up 4k tons y/y to 872k tons, increasing the US industry operating rate to 93.5% vs. 87.2% last year. However, the US industry operating rate decreased by 0.7 percentage points m/m, as production increased by 20k tons m/m, while capacity increased by 28k tons m/m. …Other RISI findings include:

Scientists have warned Members of European Parliament (MEPs) that a high-level move to water down EU legislation on deforestation could undermine Europe’s net zero emissions plans. European environment ministers rewrote a draft regulation last week to define “forest degradation” as the replacement of primary forest by plantations or other wooded land. In the EU, which has about 3.1m hectaresof primary forest amid 159m hectares of overall forest, it would limit the law’s reach to only 2% of the total area. While the proposal would also apply internationally, this could “hinder the legislation from tackling forest loss on EU soil and create a perception that the EU is evading its own forest-related responsibilities – instead throwing the burden on to developing countries in the tropics”, the scientists said. …Any exclusion of forest degradation from the law would… “gravely weaken” EU efforts to bolster global conservation, the letter adds.

Scientists have warned Members of European Parliament (MEPs) that a high-level move to water down EU legislation on deforestation could undermine Europe’s net zero emissions plans. European environment ministers rewrote a draft regulation last week to define “forest degradation” as the replacement of primary forest by plantations or other wooded land. In the EU, which has about 3.1m hectaresof primary forest amid 159m hectares of overall forest, it would limit the law’s reach to only 2% of the total area. While the proposal would also apply internationally, this could “hinder the legislation from tackling forest loss on EU soil and create a perception that the EU is evading its own forest-related responsibilities – instead throwing the burden on to developing countries in the tropics”, the scientists said. …Any exclusion of forest degradation from the law would… “gravely weaken” EU efforts to bolster global conservation, the letter adds.