The European Parliament approved legislation implementing last year’s US-EU tariff agreement, while the Canada-US-Mexico trade deadline nears. In other Business news: West Fraser’s Quesnel sawmill was fined for an accidental death in 2025; Timber Invest Group acquires eastern US timberlands; and New Zealand’s PF Olsen merges with Forest360. Meanwhile: UBC researchers advance AI-driven modular construction; a mass timber hospital in Ontario earns international recognition; and FSC Canada’s June newsletter is out.

In Forestry news: the Osoyoos Indian Band launched a new tree nursery; a new study says prescribed burning may reduce California’s wildfire smoke pollution; CAL FIRE announced $4.5M for forest health research; and Connecticut launched $1.2M in Community Forestry Grants. Meanwhile: BC urges wildfire caution as drought risks rise; Oregon’s Governor declared an emergency due to state-wide wildfire threat; and fire updates from Princeton and West Kelowna, BC; Timmins, Ontario; and South Georgia.

Finally, a Nature commentary says forest management must shift from profit to prevention.

Kelly McCloskey, Tree Frog News Editor

The Trump administration is expected to formally declare on Wednesday that it will not extend the US-Mexico-Canada Agreement on trade, starting a decade-long clock to wind down the 32-year-old North American free trade zone. That declaration will kick off a six-year review session, part of a “sunset clause” negotiated by President Trump’s first administration. However, it will do little to alter contentious negotiations over the pact’s future, including sweeping demands to boost US content in automotive production and trade protections to block Chinese goods. …Trade chiefs from the US, Mexico and Canada are expected to meet virtually on Wednesday and declare whether they want to extend the pact for another 16 years. …Failure to reach agreement on revisions to USMCA would keep the trade pact in an indefinite limbo, with similar review sessions annually for the next 10 years. …The review and sunset process is separate from a termination clause that the US could exercise, triggering a withdrawal within six months.

The Trump administration is expected to formally declare on Wednesday that it will not extend the US-Mexico-Canada Agreement on trade, starting a decade-long clock to wind down the 32-year-old North American free trade zone. That declaration will kick off a six-year review session, part of a “sunset clause” negotiated by President Trump’s first administration. However, it will do little to alter contentious negotiations over the pact’s future, including sweeping demands to boost US content in automotive production and trade protections to block Chinese goods. …Trade chiefs from the US, Mexico and Canada are expected to meet virtually on Wednesday and declare whether they want to extend the pact for another 16 years. …Failure to reach agreement on revisions to USMCA would keep the trade pact in an indefinite limbo, with similar review sessions annually for the next 10 years. …The review and sunset process is separate from a termination clause that the US could exercise, triggering a withdrawal within six months.

The European Union has formally removed its remaining tariffs on American wood-based industrial products after the European Parliament approved legislation implementing the long-awaited

The European Union has formally removed its remaining tariffs on American wood-based industrial products after the European Parliament approved legislation implementing the long-awaited

Cepi’s

Cepi’s

NEW ZEALAND — PF Olsen and Forest360 have merged to become New Zealand’s biggest independent forestry manager, trading as Stand Forestry. The companies announced their merger late last year, backed by new investment from Adamantem Capital’s Environmental Opportunities Fund and supported by PF Olsen’s Quayside Holdings. …The new brand will combine 75 years’ experience, a workforce of more than 200 skilled professionals and 480,000ha of forestry under management on both sides of the Tasman, the companies said. …The company recently launched a new carbon joint venture model in New Zealand to make it easier for farmers and landowners to participate in the Emissions Trading Scheme. …The merged group has more than 1000 clients, from major institutional investors to family-run businesses and private landowners. PF Olsen also has a large operation in Australia, managing 212,000ha.

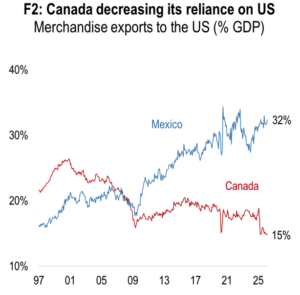

NEW ZEALAND — PF Olsen and Forest360 have merged to become New Zealand’s biggest independent forestry manager, trading as Stand Forestry. The companies announced their merger late last year, backed by new investment from Adamantem Capital’s Environmental Opportunities Fund and supported by PF Olsen’s Quayside Holdings. …The new brand will combine 75 years’ experience, a workforce of more than 200 skilled professionals and 480,000ha of forestry under management on both sides of the Tasman, the companies said. …The company recently launched a new carbon joint venture model in New Zealand to make it easier for farmers and landowners to participate in the Emissions Trading Scheme. …The merged group has more than 1000 clients, from major institutional investors to family-run businesses and private landowners. PF Olsen also has a large operation in Australia, managing 212,000ha. The US has formally declined to renew the USMCA trade agreement for a further 16 years. While existing tariff-free trade terms will continue, the decision triggers annual reviews until the agreement expires in 10 years. President Trump openly views the agreement as detrimental to US manufacturing, placing the burden of concessions firmly on Mexico and Canada. But as today’s chart shows, Canada has a much lower reliance on the US than Mexico, and the Carney administration is taking active steps to diversify its export base further. Exports from industrial sectors subject to tariffs – metals and auto – have fallen sharply, but the hit to activity is limited, as these account for just 2.5% of GDP. …Adjusted for a shrinking working-age population, production in these sectors has picked up. …Goods exports to the US make up close to one-third of Mexico’s GDP. Canada’s share is also high at 15%, but has fallen over time.

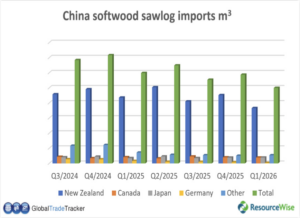

The US has formally declined to renew the USMCA trade agreement for a further 16 years. While existing tariff-free trade terms will continue, the decision triggers annual reviews until the agreement expires in 10 years. President Trump openly views the agreement as detrimental to US manufacturing, placing the burden of concessions firmly on Mexico and Canada. But as today’s chart shows, Canada has a much lower reliance on the US than Mexico, and the Carney administration is taking active steps to diversify its export base further. Exports from industrial sectors subject to tariffs – metals and auto – have fallen sharply, but the hit to activity is limited, as these account for just 2.5% of GDP. …Adjusted for a shrinking working-age population, production in these sectors has picked up. …Goods exports to the US make up close to one-third of Mexico’s GDP. Canada’s share is also high at 15%, but has fallen over time. China remains one of the world’s major importers of softwood logs and lumber, but its

China remains one of the world’s major importers of softwood logs and lumber, but its  Global oil prices fell on Monday following news of a tentative deal between Iran and the U.S. to extend their ceasefire agreement and reopen the Strait of Hormuz, but a veteran oil watcher doesn’t see crude prices returning to pre-war levels anytime soon. Eric Nuttall, partner at Ninepoint Partners, said that traders are trying to determine where the price of oil will settle out in the coming days and weeks, as many key details about the deal still need to be ironed out. …Nuttall noted that even if the strategically important Strait of Hormuz is fully reopened as a result of the Iran-U.S. deal, it will take time for oil markets to recover from the volatility of the last three and a half months. …In addition to the logistical backlog and supply chain disruption, the war in Iran has caused extensive damage to petroleum facilities across the Middle East, Nuttall explained.

Global oil prices fell on Monday following news of a tentative deal between Iran and the U.S. to extend their ceasefire agreement and reopen the Strait of Hormuz, but a veteran oil watcher doesn’t see crude prices returning to pre-war levels anytime soon. Eric Nuttall, partner at Ninepoint Partners, said that traders are trying to determine where the price of oil will settle out in the coming days and weeks, as many key details about the deal still need to be ironed out. …Nuttall noted that even if the strategically important Strait of Hormuz is fully reopened as a result of the Iran-U.S. deal, it will take time for oil markets to recover from the volatility of the last three and a half months. …In addition to the logistical backlog and supply chain disruption, the war in Iran has caused extensive damage to petroleum facilities across the Middle East, Nuttall explained. Japan’s housing starts surged 33.9% yoy in May 2026, sharply accelerating from a 11.4% increase in the previous month and marking the second straight month of expansion. It was also the fastest growth since March 2025, topping market expectations of 31.8%. Growth was broad-based across most segments, including owner-occupied homes (31.8% vs 19.5% in April), rental housing (33.3% vs 17.3%), built-for-sale housing (39.2% vs 3.4%), and two-by-four homes (24.8% vs 64.8%). In contrast, prefabricated housing fell 3.4%, swinging from a 11.1% increase in April.

Japan’s housing starts surged 33.9% yoy in May 2026, sharply accelerating from a 11.4% increase in the previous month and marking the second straight month of expansion. It was also the fastest growth since March 2025, topping market expectations of 31.8%. Growth was broad-based across most segments, including owner-occupied homes (31.8% vs 19.5% in April), rental housing (33.3% vs 17.3%), built-for-sale housing (39.2% vs 3.4%), and two-by-four homes (24.8% vs 64.8%). In contrast, prefabricated housing fell 3.4%, swinging from a 11.1% increase in April. Russia’s timber exports to China, its largest overseas market, fell sharply in the first four months of 2026 as Beijing’s prolonged property downturn weighed on demand, adding to mounting pressure on an industry already struggling with sanctions, high borrowing costs and weak profitability. Exports of Russian sawn timber to China dropped 30% year on year to 2.6 million cubic meters in January-April, while export revenue declined 26% to $603.7 million, the Vedomosti business daily reported. …China accounted for roughly half of Russia’s sawn timber exports in 2025 after Europe closed its market following Moscow’s full-scale invasion of Ukraine. But weakening Chinese construction activity, rising logistics costs and a stronger ruble have eroded demand, leaving Russian producers with fewer alternative markets. Russia’s total sawn timber exports fell 32% year-on-year to around 4 million cubic meters in the January-April period. China imported 11.2 million cubic meters of Russian sawn timber in 2025.

Russia’s timber exports to China, its largest overseas market, fell sharply in the first four months of 2026 as Beijing’s prolonged property downturn weighed on demand, adding to mounting pressure on an industry already struggling with sanctions, high borrowing costs and weak profitability. Exports of Russian sawn timber to China dropped 30% year on year to 2.6 million cubic meters in January-April, while export revenue declined 26% to $603.7 million, the Vedomosti business daily reported. …China accounted for roughly half of Russia’s sawn timber exports in 2025 after Europe closed its market following Moscow’s full-scale invasion of Ukraine. But weakening Chinese construction activity, rising logistics costs and a stronger ruble have eroded demand, leaving Russian producers with fewer alternative markets. Russia’s total sawn timber exports fell 32% year-on-year to around 4 million cubic meters in the January-April period. China imported 11.2 million cubic meters of Russian sawn timber in 2025. NEW Zealand — Increased trade is key to driving an innovative wood processing and manufacturing sector that will strengthen regional communities, reduce emissions, and build a more resilient and prosperous New Zealand, according to Mark Ross, Chief Executive of the Wood Processors and Manufacturers Association of New Zealand (WPMA). …“This includes supporting trade policies that open markets for high-value wood products, backing programmes such as the Value-Added Wood Exports Growth Accelerator, along with encouraging investment in domestic wood processing to grow the sector,” Mr Ross said. …The policy also highlights leading value-added wood and forestry trade missions into Asia and the Gulf region. The seven priority markets are Brazil, Switzerland, Argentina, Bangladesh, Nigeria, Uruguay and the European Free Trade Association (Iceland, Liechtenstein and Norway). …The Building the Future: New Zealand’s Next Billion Customers’ can be found

NEW Zealand — Increased trade is key to driving an innovative wood processing and manufacturing sector that will strengthen regional communities, reduce emissions, and build a more resilient and prosperous New Zealand, according to Mark Ross, Chief Executive of the Wood Processors and Manufacturers Association of New Zealand (WPMA). …“This includes supporting trade policies that open markets for high-value wood products, backing programmes such as the Value-Added Wood Exports Growth Accelerator, along with encouraging investment in domestic wood processing to grow the sector,” Mr Ross said. …The policy also highlights leading value-added wood and forestry trade missions into Asia and the Gulf region. The seven priority markets are Brazil, Switzerland, Argentina, Bangladesh, Nigeria, Uruguay and the European Free Trade Association (Iceland, Liechtenstein and Norway). …The Building the Future: New Zealand’s Next Billion Customers’ can be found

AUSTRALIA — The completion of the 6-Star Green Star Design redevelopment marks the first mass-timber social housing project in New South Wales, and one of the state’s earliest Class 2 timber apartment buildings. Completed in April 2026, the redevelopment delivers 75 new social homes for 130 tenants across two eight-storey towers and a separate three-storey terrace. …Since the initial concept, the project underwent several development application amendments to accommodate the use of mass timber. …One of cross-laminated timber (CLT)’s greatest advantages is speed. At Glebe, the eight-storey apartment floor was erected in as little as two weeks, while the three storey-terraces were fully completed in just three weeks. More than 2500 cubic metres of CLT and glulam were used in the construction. …The integration of a traditional brick façade introduced a slower, labour-intensive layer that disrupted sequencing. …While Australia is not short on sustainable building ambitions, regulatory frameworks have not kept pace with mass timber construction.

AUSTRALIA — The completion of the 6-Star Green Star Design redevelopment marks the first mass-timber social housing project in New South Wales, and one of the state’s earliest Class 2 timber apartment buildings. Completed in April 2026, the redevelopment delivers 75 new social homes for 130 tenants across two eight-storey towers and a separate three-storey terrace. …Since the initial concept, the project underwent several development application amendments to accommodate the use of mass timber. …One of cross-laminated timber (CLT)’s greatest advantages is speed. At Glebe, the eight-storey apartment floor was erected in as little as two weeks, while the three storey-terraces were fully completed in just three weeks. More than 2500 cubic metres of CLT and glulam were used in the construction. …The integration of a traditional brick façade introduced a slower, labour-intensive layer that disrupted sequencing. …While Australia is not short on sustainable building ambitions, regulatory frameworks have not kept pace with mass timber construction.

Join us for the 16th edition of this flagship event—the only conference of its kind this year offering such a comprehensive view of the Cellulose market, covering the entire value chain from upstream to downstream. CelCo started up the conference Investing in Cellulose in 2011. Since then, it has been running every year in London, in November, the first Monday of the London Pulp Week. Its objective is to gather the entire cellulose value chain: from specialty wood pulp and cotton linters pulp suppliers to all viscose, acetate, ether & MCC, nitrate, cellophane, tyrecord, sausage casings, and sponge applications, as well as final converters up to “Brand levels” (textile, hygiene, pharmaceutical, cigarette, automotive, food, construction industries, etc.). The one-day conference includes a full-day event with 8 speakers, a breakfast, formal lunch, coffee breaks, and a cocktail the previous evening. The event will be held on Monday, November 9, 2026, from 9:30 a.m. to 4:00 p.m. at the luxurious Waldorf Hotel near Covent Garden. …This event is organized by CelCo, a cellulose consulting company registered in Switzerland, led by Christian Chavassieu, and assisted by its partner, Numera Analytics.

Join us for the 16th edition of this flagship event—the only conference of its kind this year offering such a comprehensive view of the Cellulose market, covering the entire value chain from upstream to downstream. CelCo started up the conference Investing in Cellulose in 2011. Since then, it has been running every year in London, in November, the first Monday of the London Pulp Week. Its objective is to gather the entire cellulose value chain: from specialty wood pulp and cotton linters pulp suppliers to all viscose, acetate, ether & MCC, nitrate, cellophane, tyrecord, sausage casings, and sponge applications, as well as final converters up to “Brand levels” (textile, hygiene, pharmaceutical, cigarette, automotive, food, construction industries, etc.). The one-day conference includes a full-day event with 8 speakers, a breakfast, formal lunch, coffee breaks, and a cocktail the previous evening. The event will be held on Monday, November 9, 2026, from 9:30 a.m. to 4:00 p.m. at the luxurious Waldorf Hotel near Covent Garden. …This event is organized by CelCo, a cellulose consulting company registered in Switzerland, led by Christian Chavassieu, and assisted by its partner, Numera Analytics.

A proposed change to England’s fire-safety guidance could make it much harder to use timber in load-bearing structures above 11 metres. The consultation on changes to Approved Document B, the fire-safety guidance used under the Building Regulations in England, closes on 1 July 2026. Under the draft text, load-bearing elements of structure in buildings with a storey more than 11 metres above ground level should be made from materials or products achieving at least class A2-s3,d2. Most structural timber and mass timber products do not normally meet this reaction-to-fire classification. The proposal would move the debate beyond external walls and cladding. It could affect the structural frame itself in a much wider group of mid-rise residential, commercial and mixed-use buildings. This matters because mass timber and CLT are increasingly used in projects where developers want faster construction and lower embodied carbon compared with concrete or steel.

A proposed change to England’s fire-safety guidance could make it much harder to use timber in load-bearing structures above 11 metres. The consultation on changes to Approved Document B, the fire-safety guidance used under the Building Regulations in England, closes on 1 July 2026. Under the draft text, load-bearing elements of structure in buildings with a storey more than 11 metres above ground level should be made from materials or products achieving at least class A2-s3,d2. Most structural timber and mass timber products do not normally meet this reaction-to-fire classification. The proposal would move the debate beyond external walls and cladding. It could affect the structural frame itself in a much wider group of mid-rise residential, commercial and mixed-use buildings. This matters because mass timber and CLT are increasingly used in projects where developers want faster construction and lower embodied carbon compared with concrete or steel.

SINGAPORE — The Alliance to End Plastic Waste today published

SINGAPORE — The Alliance to End Plastic Waste today published

Timber frame homes built in as little as five days could be a way to increase the pace of housebuilding in London, some of the capital’s largest construction companies have heard. Industry leaders travelled to Scotland to learn how the housing is produced, from sustainable forestry through to completed homes, as developers and ministers look for ways to increase the number of homes in the city. Scotland has adopted timber frame construction on a greater scale than England. About 92% of new homes north of the border are built using timber frame, compared with 13% in England. Andrew Orriss, of the Structural Timber Association, said: “Scotland builds faster, greener, and more efficiently than England. …“And the reason is timber frame. …Mayor of London Sir Sadiq Khan has a target to build 88,000 new homes per year. …In Britain, structural timber are only permitted to a maximum height of 18 metres, or up to 6 storeys.

Timber frame homes built in as little as five days could be a way to increase the pace of housebuilding in London, some of the capital’s largest construction companies have heard. Industry leaders travelled to Scotland to learn how the housing is produced, from sustainable forestry through to completed homes, as developers and ministers look for ways to increase the number of homes in the city. Scotland has adopted timber frame construction on a greater scale than England. About 92% of new homes north of the border are built using timber frame, compared with 13% in England. Andrew Orriss, of the Structural Timber Association, said: “Scotland builds faster, greener, and more efficiently than England. …“And the reason is timber frame. …Mayor of London Sir Sadiq Khan has a target to build 88,000 new homes per year. …In Britain, structural timber are only permitted to a maximum height of 18 metres, or up to 6 storeys.

As the Victorian Forestry Transition Program comes to a close, some residents in regions that relied on the timber trade are questioning what has been done to build a replacement economy. The state government’s transition program ends today, two-and-a-half years after Victoria’s native logging industry was brought to an end with the flourish of a pen. The government committed $1.5 billion to support the transition, including $320 million to the Forestry Transition Program to provide financial support for affected workers, businesses and communities. But some residents remain unconvinced enough has been done to replace the jobs lost. …A Victorian auditor general’s

As the Victorian Forestry Transition Program comes to a close, some residents in regions that relied on the timber trade are questioning what has been done to build a replacement economy. The state government’s transition program ends today, two-and-a-half years after Victoria’s native logging industry was brought to an end with the flourish of a pen. The government committed $1.5 billion to support the transition, including $320 million to the Forestry Transition Program to provide financial support for affected workers, businesses and communities. But some residents remain unconvinced enough has been done to replace the jobs lost. …A Victorian auditor general’s

LONDON — The world’s rainforests are to be better protected from deforestation as the government will confirm during London Climate Action Week, that plans to take forward new rules in Great Britain including using powers in the Environment Act alongside legislation strengthening the UK Timber Regulation. Under the proposals UK businesses who trade in commodities sourced from rainforests… will need to check that their supply chains are not contributing to illegal deforestation. …UK companies have been at the forefront of global efforts to tackle deforestation within their supply chains, but voluntary action alone cannot tackle this global challenge, and several major supermarkets have been calling for stronger regulation. Rainforests and other forests are vital for storing carbon and sustaining biodiversity, yet they are increasingly threatened by deforestation. … Rules will be enforced using powers in the Environment Act, alongside legislation strengthening existing timber rules.

LONDON — The world’s rainforests are to be better protected from deforestation as the government will confirm during London Climate Action Week, that plans to take forward new rules in Great Britain including using powers in the Environment Act alongside legislation strengthening the UK Timber Regulation. Under the proposals UK businesses who trade in commodities sourced from rainforests… will need to check that their supply chains are not contributing to illegal deforestation. …UK companies have been at the forefront of global efforts to tackle deforestation within their supply chains, but voluntary action alone cannot tackle this global challenge, and several major supermarkets have been calling for stronger regulation. Rainforests and other forests are vital for storing carbon and sustaining biodiversity, yet they are increasingly threatened by deforestation. … Rules will be enforced using powers in the Environment Act, alongside legislation strengthening existing timber rules. AUSTRALIA — Tasmania’s public native forestry company has corrected the record in a parliamentary committee after earlier stating that all logs from public native forests were processed in Tasmania. Tasmanian sawmill operator James Neville-Smith confirmed that some logs had been sent to Victoria, where processors had received compensation from the Victorian government as part of its industry shutdown. Mr Neville-Smith said the decision was due to retooling a sawmill to be plantation-only, meaning that hardwood logs needed to be processed elsewhere. Logs displaying stickers from Tasmanian state forests were also spotted at a mill in Powelltown, in the Yarra Valley, that was also a recipient of millions in Victorian compensation payments. Victoria phased out native forest logging in 2024. Since then, environmental groups have raised concerns about large quantities of logs being transported to Victoria on the Spirit of Tasmania, but were told that all were from private forests.

AUSTRALIA — Tasmania’s public native forestry company has corrected the record in a parliamentary committee after earlier stating that all logs from public native forests were processed in Tasmania. Tasmanian sawmill operator James Neville-Smith confirmed that some logs had been sent to Victoria, where processors had received compensation from the Victorian government as part of its industry shutdown. Mr Neville-Smith said the decision was due to retooling a sawmill to be plantation-only, meaning that hardwood logs needed to be processed elsewhere. Logs displaying stickers from Tasmanian state forests were also spotted at a mill in Powelltown, in the Yarra Valley, that was also a recipient of millions in Victorian compensation payments. Victoria phased out native forest logging in 2024. Since then, environmental groups have raised concerns about large quantities of logs being transported to Victoria on the Spirit of Tasmania, but were told that all were from private forests. JAKARTA — Pulp and paper giant APRIL’s recent decision to lower its deforestation commitments and source wood from two companies associated with extensive recent forest loss has created a new challenge for its relationship with the Forest Stewardship Council (FSC), with environmental groups urging the world’s leading forestry certifier to terminate the already suspended reassociation process. In late May, APRIL announced it was reviewing its decade-old Sustainable Forest Management Policy 2.0 and lowering its deforestation cutoff date from 2015 to Dec. 31, 2020. The move allows the pulp and paper producer to source wood from PT Industrial Forest Plantation and PT Mayawana Persada, two companies that have experienced some of the country’s largest recent forest losses. APRIL said the decision was necessary to address fibre shortages after the Indonesian government revoked the operating permits of four of its long-term suppliers earlier this year, affecting around 15% of its wood supply in Riau Province.

JAKARTA — Pulp and paper giant APRIL’s recent decision to lower its deforestation commitments and source wood from two companies associated with extensive recent forest loss has created a new challenge for its relationship with the Forest Stewardship Council (FSC), with environmental groups urging the world’s leading forestry certifier to terminate the already suspended reassociation process. In late May, APRIL announced it was reviewing its decade-old Sustainable Forest Management Policy 2.0 and lowering its deforestation cutoff date from 2015 to Dec. 31, 2020. The move allows the pulp and paper producer to source wood from PT Industrial Forest Plantation and PT Mayawana Persada, two companies that have experienced some of the country’s largest recent forest losses. APRIL said the decision was necessary to address fibre shortages after the Indonesian government revoked the operating permits of four of its long-term suppliers earlier this year, affecting around 15% of its wood supply in Riau Province. During the 1930s, Italy’s government launched a sweeping reforestation effort in the Prealps region near Lake Como, planting fast-growing Norway spruce on land that had been pasture and meadow for centuries. It was a conscious decision, made mainly to answer the demand for timber, but it did not involve much ecological thinking. Now, 90 years later, a new study has gone back to measure what that decision actually did to the landscape, and the results are not flattering. According to the study, ‘

During the 1930s, Italy’s government launched a sweeping reforestation effort in the Prealps region near Lake Como, planting fast-growing Norway spruce on land that had been pasture and meadow for centuries. It was a conscious decision, made mainly to answer the demand for timber, but it did not involve much ecological thinking. Now, 90 years later, a new study has gone back to measure what that decision actually did to the landscape, and the results are not flattering. According to the study, ‘

OFUNATO, Iwate — An industry organization aimed at promoting the use of fire-damaged timber has been launched in this northeastern Japan city, in response to a forest fire that broke out here in February 2025 burning approximately 3,370 hectares. The organization, named “TEAM Shinrin Saisei Ofunato” … aims to address challenges surrounding the harvesting of damaged trees and expand distribution channels for related wood products. Trees can still be utilized for parts that were not burned or if the damage was limited to the bark, but they must be cut down promptly before moisture loss makes them difficult to use. By strengthening cooperation among the logging, lumber processing, and construction sectors, which are currently divided into separate segments of the wood industry, the organization hopes to make better use of the damaged timber and encourage forest owners to proceed with logging and reforestation.

OFUNATO, Iwate — An industry organization aimed at promoting the use of fire-damaged timber has been launched in this northeastern Japan city, in response to a forest fire that broke out here in February 2025 burning approximately 3,370 hectares. The organization, named “TEAM Shinrin Saisei Ofunato” … aims to address challenges surrounding the harvesting of damaged trees and expand distribution channels for related wood products. Trees can still be utilized for parts that were not burned or if the damage was limited to the bark, but they must be cut down promptly before moisture loss makes them difficult to use. By strengthening cooperation among the logging, lumber processing, and construction sectors, which are currently divided into separate segments of the wood industry, the organization hopes to make better use of the damaged timber and encourage forest owners to proceed with logging and reforestation. Demand for biofuels has been growing in many parts of the world. …Disruption to oil exports via the Strait of Hormuz this year created a further incentive to switch to biofuels to ensure energy security. While biofuels can’t fully replace petroleum, they can be blended into gasoline and diesel, allowing countries to stretch existing fuel supplies. Many environmentalists contest the idea that biofuels are a sustainable alternative source of energy. And as more farmland is used to produce them, there’s less available to make food, increasing the risk of global food shortages and hunger in the poorest nations. …The priciest biofuel is sustainable aviation fuel, or SAF, which uses advanced refining processes to convert waste oils into jet fuel that can be blended for use in aircraft. There’s also so-called advanced or second-generation biodiesel, made from non-food sources such as crop waste, wood chips and even algae, which avoids competing with food crops.

Demand for biofuels has been growing in many parts of the world. …Disruption to oil exports via the Strait of Hormuz this year created a further incentive to switch to biofuels to ensure energy security. While biofuels can’t fully replace petroleum, they can be blended into gasoline and diesel, allowing countries to stretch existing fuel supplies. Many environmentalists contest the idea that biofuels are a sustainable alternative source of energy. And as more farmland is used to produce them, there’s less available to make food, increasing the risk of global food shortages and hunger in the poorest nations. …The priciest biofuel is sustainable aviation fuel, or SAF, which uses advanced refining processes to convert waste oils into jet fuel that can be blended for use in aircraft. There’s also so-called advanced or second-generation biodiesel, made from non-food sources such as crop waste, wood chips and even algae, which avoids competing with food crops.

UK — The City watchdog has closed an investigation into the owner of the Drax power plant after an almost 10-month review into whether the company’s sustainability claims mislead shareholders. The Financial Conduct Authority said it had “reviewed thousands of pages” of “complex material” relating to the company’s sourcing of wood pellets for the Drax power plant in Selby, North Yorkshire, but “did not find evidence that justified any further action”. The regulator began the investigation last year into whether Drax’s annual reports and accounts between 2021 and 2023 misled shareholders or left out important information investors needed to know about the origins of its biomass fuel. …Ofgem found at the time that there was no evidence to suggest the breach was deliberate, and said instead that it was “technical in nature”. It also found no evidence that the biomass sourced was unsustainable or that Drax had wrongly laid claim to renewable energy subsidies.

UK — The City watchdog has closed an investigation into the owner of the Drax power plant after an almost 10-month review into whether the company’s sustainability claims mislead shareholders. The Financial Conduct Authority said it had “reviewed thousands of pages” of “complex material” relating to the company’s sourcing of wood pellets for the Drax power plant in Selby, North Yorkshire, but “did not find evidence that justified any further action”. The regulator began the investigation last year into whether Drax’s annual reports and accounts between 2021 and 2023 misled shareholders or left out important information investors needed to know about the origins of its biomass fuel. …Ofgem found at the time that there was no evidence to suggest the breach was deliberate, and said instead that it was “technical in nature”. It also found no evidence that the biomass sourced was unsustainable or that Drax had wrongly laid claim to renewable energy subsidies. Here’s the latest news concerning climate change and biodiversity loss in B.C. and around the world, from the steps leaders are taking to address the problems, to all the up-to-date science. Human activities like burning fossil fuels and farming livestock are the main drivers of climate change, according to the UN’s intergovernmental panel on climate change. The panel, which is made up of scientists from around the world, including researchers from B.C., has … issued a code red for humanity and warns the window to limit warming to 1.5 C above pre-industrial times is closing. …El Niño — a climate cycle that causes unusually warm ocean surface temperatures in the equatorial Pacific, altering global weather patterns — has begun and is expected to grow to historical strength, the U.S. National Oceanic and Atmospheric Administration

Here’s the latest news concerning climate change and biodiversity loss in B.C. and around the world, from the steps leaders are taking to address the problems, to all the up-to-date science. Human activities like burning fossil fuels and farming livestock are the main drivers of climate change, according to the UN’s intergovernmental panel on climate change. The panel, which is made up of scientists from around the world, including researchers from B.C., has … issued a code red for humanity and warns the window to limit warming to 1.5 C above pre-industrial times is closing. …El Niño — a climate cycle that causes unusually warm ocean surface temperatures in the equatorial Pacific, altering global weather patterns — has begun and is expected to grow to historical strength, the U.S. National Oceanic and Atmospheric Administration  LONDON — The United States accounted for about a third of the rise in global carbon emissions in 2025, as higher gas prices pushed power producers back to coal, an Energy Institute report showed. Highlights from the report include:

LONDON — The United States accounted for about a third of the rise in global carbon emissions in 2025, as higher gas prices pushed power producers back to coal, an Energy Institute report showed. Highlights from the report include: The German government has approved a draft law designed to limit the support for electricity generation from woody biomass, aiming the meet the EU requirements. As a result, certain categories of wood will be excluded from subsidisation under Germany’s Renewable Energy Sources Act (EEG), such as saw logs, veneer logs, other industrial-grade roundwood and stumps and roots harvested from forests. Electricity generation from these types of wood, however, may still receive support if it is necessary to safeguard Germany’s energy security or if local industry is unable to use the forestry biomass in ways that deliver greater economic and environmental value than energy production. Under the proposed law, industrial wood residues will remain eligible for financing.

The German government has approved a draft law designed to limit the support for electricity generation from woody biomass, aiming the meet the EU requirements. As a result, certain categories of wood will be excluded from subsidisation under Germany’s Renewable Energy Sources Act (EEG), such as saw logs, veneer logs, other industrial-grade roundwood and stumps and roots harvested from forests. Electricity generation from these types of wood, however, may still receive support if it is necessary to safeguard Germany’s energy security or if local industry is unable to use the forestry biomass in ways that deliver greater economic and environmental value than energy production. Under the proposed law, industrial wood residues will remain eligible for financing.

Western Europe is enduring a ferocious heatwave forecast to break temperature records, with half of France on red alert, rail services in Belgium disrupted and sports events in Spain and Germany cancelled or postponed. French authorities on Monday placed 49 of the country’s 96 mainland departments on a level 1 danger-to-life warning, urging 35 million people to exercise “absolute vigilance”, drink water often, avoid all strenuous exertion and stay out of direct sun. Another 40 departments were on a level 2 orange alert. “Very high temperatures are setting in for the long term across the country,” said the national meteorological service, Météo-France. “Day and night-time temperatures will be exceptional.” It said temperatures throughout western and central France were likely to exceed 40C from Monday afternoon, hitting 43C in Bordeaux, 41C in Limoges, 40C in Toulouse and Tours and 39C in Paris, and would continue rising until the end of the week.

Western Europe is enduring a ferocious heatwave forecast to break temperature records, with half of France on red alert, rail services in Belgium disrupted and sports events in Spain and Germany cancelled or postponed. French authorities on Monday placed 49 of the country’s 96 mainland departments on a level 1 danger-to-life warning, urging 35 million people to exercise “absolute vigilance”, drink water often, avoid all strenuous exertion and stay out of direct sun. Another 40 departments were on a level 2 orange alert. “Very high temperatures are setting in for the long term across the country,” said the national meteorological service, Météo-France. “Day and night-time temperatures will be exceptional.” It said temperatures throughout western and central France were likely to exceed 40C from Monday afternoon, hitting 43C in Bordeaux, 41C in Limoges, 40C in Toulouse and Tours and 39C in Paris, and would continue rising until the end of the week. A wildfire burning out of control in southwestern France has forced the evacuation of 10,000 people from two dozen small towns and villages near the Spanish border and officials said strong winds on Monday would further fan the blaze. The European Union said on Monday it was sending four waterbombing aircraft to France from Cyprus and Sweden to help firefighters around the city of Perpignan. …The blaze has injured 16 people, including four firefighters, and scorched some 4,600 hectares in the foothills of the French Pyrenees. Early summer heat waves in France and across western Europe in May and June have scorched vast areas of land, making them particularly vulnerable to wildfires this year. The Trevillach blaze was burning near the third stage of the Tour de France, leading to its closure to the public on Monday to allow firefighters easy access to the area, according to Tour de France director Christian Prudhomme.

A wildfire burning out of control in southwestern France has forced the evacuation of 10,000 people from two dozen small towns and villages near the Spanish border and officials said strong winds on Monday would further fan the blaze. The European Union said on Monday it was sending four waterbombing aircraft to France from Cyprus and Sweden to help firefighters around the city of Perpignan. …The blaze has injured 16 people, including four firefighters, and scorched some 4,600 hectares in the foothills of the French Pyrenees. Early summer heat waves in France and across western Europe in May and June have scorched vast areas of land, making them particularly vulnerable to wildfires this year. The Trevillach blaze was burning near the third stage of the Tour de France, leading to its closure to the public on Monday to allow firefighters easy access to the area, according to Tour de France director Christian Prudhomme. Hundreds of firefighters have been battling forest infernos in heatwave-scarred Europe, as temperatures are set to rise again on Sunday, local time. The latest wildfires have already devastated more than 17,000 hectares of land across France, Spain and Portugal where temperatures in some places are forecast to reach 40C. Authorities registered

Hundreds of firefighters have been battling forest infernos in heatwave-scarred Europe, as temperatures are set to rise again on Sunday, local time. The latest wildfires have already devastated more than 17,000 hectares of land across France, Spain and Portugal where temperatures in some places are forecast to reach 40C. Authorities registered