The Trump administration is expected to formally declare on Wednesday that it will not extend the US-Mexico-Canada Agreement on trade, starting a decade-long clock to wind down the 32-year-old North American free trade zone. That declaration will kick off a six-year review session, part of a “sunset clause” negotiated by President Trump’s first administration. However, it will do little to alter contentious negotiations over the pact’s future, including sweeping demands to boost US content in automotive production and trade protections to block Chinese goods. …Trade chiefs from the US, Mexico and Canada are expected to meet virtually on Wednesday and declare whether they want to extend the pact for another 16 years. …Failure to reach agreement on revisions to USMCA would keep the trade pact in an indefinite limbo, with similar review sessions annually for the next 10 years. …The review and sunset process is separate from a termination clause that the US could exercise, triggering a withdrawal within six months.

The Trump administration is expected to formally declare on Wednesday that it will not extend the US-Mexico-Canada Agreement on trade, starting a decade-long clock to wind down the 32-year-old North American free trade zone. That declaration will kick off a six-year review session, part of a “sunset clause” negotiated by President Trump’s first administration. However, it will do little to alter contentious negotiations over the pact’s future, including sweeping demands to boost US content in automotive production and trade protections to block Chinese goods. …Trade chiefs from the US, Mexico and Canada are expected to meet virtually on Wednesday and declare whether they want to extend the pact for another 16 years. …Failure to reach agreement on revisions to USMCA would keep the trade pact in an indefinite limbo, with similar review sessions annually for the next 10 years. …The review and sunset process is separate from a termination clause that the US could exercise, triggering a withdrawal within six months.

Related coverage by:

- Kelly Malone, Canadian Press: Trade pact set to stay in place as US blows past key deadline

- Daniel Desrochers in Politico: Trump ‘hates’ his own trade deal. But he’ll have a hard time killing it

- Shawn Jeffords in CBC News: Businesses and unions are balancing anxiety and hope for CUSMA

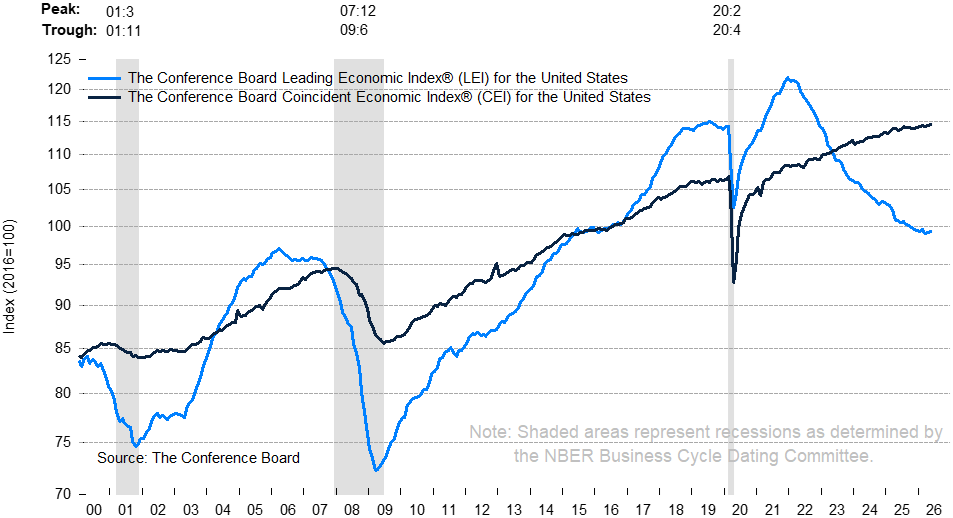

Corporate bosses are more relaxed about tariffs now than at any time since US President Trump’s return to power unleashed a spate of trade policy chaos. The share of corporate earnings calls in which tariffs were mentioned has fallen to the lowest level since Mr. Trump won the 2024 election, according to an analysis of transcripts. …The same pattern has played out on both sides of the border, even though companies have plenty of reasons to remain anxious on the trade front. The USMCA is set to enter uncharted territory on July 1. …Steep sectoral duties remain in place. …Meanwhile, Mr. Trump is expected to launch a wave of hefty tariffs next month to replace temporary duties he imposed after the U.S. Supreme Court struck down his earlier emergency tariffs. [to access the full story a Globe and Mail subscription is required]

Corporate bosses are more relaxed about tariffs now than at any time since US President Trump’s return to power unleashed a spate of trade policy chaos. The share of corporate earnings calls in which tariffs were mentioned has fallen to the lowest level since Mr. Trump won the 2024 election, according to an analysis of transcripts. …The same pattern has played out on both sides of the border, even though companies have plenty of reasons to remain anxious on the trade front. The USMCA is set to enter uncharted territory on July 1. …Steep sectoral duties remain in place. …Meanwhile, Mr. Trump is expected to launch a wave of hefty tariffs next month to replace temporary duties he imposed after the U.S. Supreme Court struck down his earlier emergency tariffs. [to access the full story a Globe and Mail subscription is required]

A Toronto company is suing BC, saying it was stripped of its mining rights as part of a deal with the Gitxaała Nation. In a lawsuit filed in BC Supreme Court, MCC Canadian Gold Ventures says it was asked to rescue a small gold mine on Banks Island, south of Prince Rupert. But then the BC government stripped its mining rights to offset some of the impacts of another BC Supreme Court ruling involving the Gitxaała. The company says it invested millions in the property and now cannot move ahead on the project. …The province has not filed a response. …MCC said their case has “striking” parallels to a lawsuit launched by Carrier Lumber in the 1990s. In 2002, the province paid a large settlement to Carrier Lumber over a lawsuit it won over government decisions the company said made it impossible to harvest timber in the BC Interior.

A Toronto company is suing BC, saying it was stripped of its mining rights as part of a deal with the Gitxaała Nation. In a lawsuit filed in BC Supreme Court, MCC Canadian Gold Ventures says it was asked to rescue a small gold mine on Banks Island, south of Prince Rupert. But then the BC government stripped its mining rights to offset some of the impacts of another BC Supreme Court ruling involving the Gitxaała. The company says it invested millions in the property and now cannot move ahead on the project. …The province has not filed a response. …MCC said their case has “striking” parallels to a lawsuit launched by Carrier Lumber in the 1990s. In 2002, the province paid a large settlement to Carrier Lumber over a lawsuit it won over government decisions the company said made it impossible to harvest timber in the BC Interior.

A sprawling legislative package aimed at lowering the cost of housing and spurring more home construction won bipartisan approval from Congress this week, but it’s hit a major roadblock in becoming law: President Trump. The White House supported the

A sprawling legislative package aimed at lowering the cost of housing and spurring more home construction won bipartisan approval from Congress this week, but it’s hit a major roadblock in becoming law: President Trump. The White House supported the  The European Union has formally removed its remaining tariffs on American wood-based industrial products after the European Parliament approved legislation implementing the long-awaited

The European Union has formally removed its remaining tariffs on American wood-based industrial products after the European Parliament approved legislation implementing the long-awaited

OTTAWA — Canada’s annual inflation rate in May accelerated more than expected to 3.2%, a 29-month high, data showed on Monday, as the impact of higher crude oil prices due to the Iran conflict continued to filter through gasoline costs. Analysts polled by Reuters had estimated the annual inflation rate to touch 3% in May, up from 2.8% in April. The prices, however, are already showing a major reversal in June after an interim peace deal was signed between the United States and Iran last week, which, analysts have said, could help ease the headline number in June. Statistics Canada said excluding the impact of gasoline prices, the consumer price index still posted a higher increase of 2.2% in May from 2% in April. The monthly inflation rate rose to 1% in May, exceeding expectations of 0.8% rise. This is the highest monthly rise in 15 months.

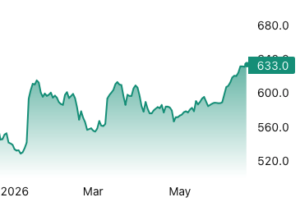

OTTAWA — Canada’s annual inflation rate in May accelerated more than expected to 3.2%, a 29-month high, data showed on Monday, as the impact of higher crude oil prices due to the Iran conflict continued to filter through gasoline costs. Analysts polled by Reuters had estimated the annual inflation rate to touch 3% in May, up from 2.8% in April. The prices, however, are already showing a major reversal in June after an interim peace deal was signed between the United States and Iran last week, which, analysts have said, could help ease the headline number in June. Statistics Canada said excluding the impact of gasoline prices, the consumer price index still posted a higher increase of 2.2% in May from 2% in April. The monthly inflation rate rose to 1% in May, exceeding expectations of 0.8% rise. This is the highest monthly rise in 15 months. Lumber climbed past $630 per thousand board feet, the highest level since October, amid higher effective US import costs on Canadian softwood and tighter expected supply. Prices rose despite a small reduction in preliminary antidumping and countervailing duties, because the combined tariff burden remains high at about 35.9% including the existing Section 232 levy, set to take effect in August. The market is also being driven by uncertainty ahead of final duty decisions, prompting buyers to accelerate purchases and lift near-term demand. At the same time, US domestic production is still constrained, while housing-related consumption remains structurally large, with softwood lumber and engineered wood products heavily used in new construction. Each new home requires roughly 15,000 board feet of lumber plus extensive engineered wood products, keeping baseline consumption elevated even in a softer housing cycle. [END]

Lumber climbed past $630 per thousand board feet, the highest level since October, amid higher effective US import costs on Canadian softwood and tighter expected supply. Prices rose despite a small reduction in preliminary antidumping and countervailing duties, because the combined tariff burden remains high at about 35.9% including the existing Section 232 levy, set to take effect in August. The market is also being driven by uncertainty ahead of final duty decisions, prompting buyers to accelerate purchases and lift near-term demand. At the same time, US domestic production is still constrained, while housing-related consumption remains structurally large, with softwood lumber and engineered wood products heavily used in new construction. Each new home requires roughly 15,000 board feet of lumber plus extensive engineered wood products, keeping baseline consumption elevated even in a softer housing cycle. [END] The U.S. goods trade deficit is widening, the Commerce Department said Friday, suggesting stockpiling ahead of higher tariffs and a continued reliance on imports for the domestic data center rollout, analysts say. The goods trade deficit for May jumped more than $20 billion to $105.8 billion, up from $83 billion in April, according to

The U.S. goods trade deficit is widening, the Commerce Department said Friday, suggesting stockpiling ahead of higher tariffs and a continued reliance on imports for the domestic data center rollout, analysts say. The goods trade deficit for May jumped more than $20 billion to $105.8 billion, up from $83 billion in April, according to

The Federal Reserve’s primary price gauge rose at its highest level since 2023, reinforcing the central bank’s recent tough talk on inflation. Excluding food and energy, the personal consumption expenditures price index showed a 3.4% annual rate after rising 0.3% for the month. The annual core reading was the highest since October 2023. For the all-items reading, the PCE index showed inflation running at a

The Federal Reserve’s primary price gauge rose at its highest level since 2023, reinforcing the central bank’s recent tough talk on inflation. Excluding food and energy, the personal consumption expenditures price index showed a 3.4% annual rate after rising 0.3% for the month. The annual core reading was the highest since October 2023. For the all-items reading, the PCE index showed inflation running at a

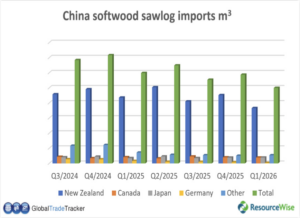

China remains one of the world’s major importers of softwood logs and lumber, but its

China remains one of the world’s major importers of softwood logs and lumber, but its  While supply concerns are still weighing on housing affordability, a combination of soaring prices and economic uncertainty is dragging on housing demand, according to the annual

While supply concerns are still weighing on housing affordability, a combination of soaring prices and economic uncertainty is dragging on housing demand, according to the annual

Russia’s timber exports to China, its largest overseas market, fell sharply in the first four months of 2026 as Beijing’s prolonged property downturn weighed on demand, adding to mounting pressure on an industry already struggling with sanctions, high borrowing costs and weak profitability. Exports of Russian sawn timber to China dropped 30% year on year to 2.6 million cubic meters in January-April, while export revenue declined 26% to $603.7 million, the Vedomosti business daily reported. …China accounted for roughly half of Russia’s sawn timber exports in 2025 after Europe closed its market following Moscow’s full-scale invasion of Ukraine. But weakening Chinese construction activity, rising logistics costs and a stronger ruble have eroded demand, leaving Russian producers with fewer alternative markets. Russia’s total sawn timber exports fell 32% year-on-year to around 4 million cubic meters in the January-April period. China imported 11.2 million cubic meters of Russian sawn timber in 2025.

Russia’s timber exports to China, its largest overseas market, fell sharply in the first four months of 2026 as Beijing’s prolonged property downturn weighed on demand, adding to mounting pressure on an industry already struggling with sanctions, high borrowing costs and weak profitability. Exports of Russian sawn timber to China dropped 30% year on year to 2.6 million cubic meters in January-April, while export revenue declined 26% to $603.7 million, the Vedomosti business daily reported. …China accounted for roughly half of Russia’s sawn timber exports in 2025 after Europe closed its market following Moscow’s full-scale invasion of Ukraine. But weakening Chinese construction activity, rising logistics costs and a stronger ruble have eroded demand, leaving Russian producers with fewer alternative markets. Russia’s total sawn timber exports fell 32% year-on-year to around 4 million cubic meters in the January-April period. China imported 11.2 million cubic meters of Russian sawn timber in 2025.

ATLANTA — At

ATLANTA — At  A bipartisan bill in the US House is calling for additional incentives to use of mass timber building materials in federal contracting. Introduced by House Ag Committee Chair Glenn Thompson (R-PA) and Andrea Salinas (D-OR), the

A bipartisan bill in the US House is calling for additional incentives to use of mass timber building materials in federal contracting. Introduced by House Ag Committee Chair Glenn Thompson (R-PA) and Andrea Salinas (D-OR), the  A proposed change to England’s fire-safety guidance could make it much harder to use timber in load-bearing structures above 11 metres. The consultation on changes to Approved Document B, the fire-safety guidance used under the Building Regulations in England, closes on 1 July 2026. Under the draft text, load-bearing elements of structure in buildings with a storey more than 11 metres above ground level should be made from materials or products achieving at least class A2-s3,d2. Most structural timber and mass timber products do not normally meet this reaction-to-fire classification. The proposal would move the debate beyond external walls and cladding. It could affect the structural frame itself in a much wider group of mid-rise residential, commercial and mixed-use buildings. This matters because mass timber and CLT are increasingly used in projects where developers want faster construction and lower embodied carbon compared with concrete or steel.

A proposed change to England’s fire-safety guidance could make it much harder to use timber in load-bearing structures above 11 metres. The consultation on changes to Approved Document B, the fire-safety guidance used under the Building Regulations in England, closes on 1 July 2026. Under the draft text, load-bearing elements of structure in buildings with a storey more than 11 metres above ground level should be made from materials or products achieving at least class A2-s3,d2. Most structural timber and mass timber products do not normally meet this reaction-to-fire classification. The proposal would move the debate beyond external walls and cladding. It could affect the structural frame itself in a much wider group of mid-rise residential, commercial and mixed-use buildings. This matters because mass timber and CLT are increasingly used in projects where developers want faster construction and lower embodied carbon compared with concrete or steel. SINGAPORE — The Alliance to End Plastic Waste today published

SINGAPORE — The Alliance to End Plastic Waste today published

British Columbians are subsidizing the province’s forest companies to the tune of tens of millions of dollars each year under a government program that defrays the cost of shipping logs from remote forests to distant mills. In 2023, logging companies received nearly $33 million in public funds to underwrite the costs of hauling “low-value” logs to wood pulp and pellet mills. …The subsidies are posted online by the Forest Enhancement Society of BC, or FESBC, an organization created and funded by the provincial government and that reports to Forests Minister Ravi Parmar. The society’s mandate includes “preventing and mitigating the impact of wildfires” and “improving habitat for wildlife.” But many FESBC funds simply underwrite the increasing costs of hauling logs. Those expenses have been marching upward as logging activities push farther into the hinterland. That has some questioning whether the funding is accelerating the logging of forests, rather than enhancing them.

British Columbians are subsidizing the province’s forest companies to the tune of tens of millions of dollars each year under a government program that defrays the cost of shipping logs from remote forests to distant mills. In 2023, logging companies received nearly $33 million in public funds to underwrite the costs of hauling “low-value” logs to wood pulp and pellet mills. …The subsidies are posted online by the Forest Enhancement Society of BC, or FESBC, an organization created and funded by the provincial government and that reports to Forests Minister Ravi Parmar. The society’s mandate includes “preventing and mitigating the impact of wildfires” and “improving habitat for wildlife.” But many FESBC funds simply underwrite the increasing costs of hauling logs. Those expenses have been marching upward as logging activities push farther into the hinterland. That has some questioning whether the funding is accelerating the logging of forests, rather than enhancing them.

Way back in 1995 Bob Brown, the Republican president of the Montana Senate, called me into his office. He had co-sponsored a bill with a pro-logging Missoula Democrat to establish a “sustained yield” level of logging on Montana’s state trust lands – and he was worried it wasn’t working out the way he hoped. Bob was right to be worried then and Montanans are right to be worried now because Trump’s Forest Service Chief and former timber industry lobbyist Tom Schultz, has just unleashed the “sustained yield” scam on Montana’s National Forests. …My advice to Bob was to let the bill die because he didn’t have the votes to remove the amendments the timber industry lobbyists stuck on the bill. But he didn’t take that advice. …Two years later, Tom Schultz went to work for Montana’s Department of Natural Resources and Conservation, earning the sobriquet “Chainsaw Tom” for his pro-logging zeal.

Way back in 1995 Bob Brown, the Republican president of the Montana Senate, called me into his office. He had co-sponsored a bill with a pro-logging Missoula Democrat to establish a “sustained yield” level of logging on Montana’s state trust lands – and he was worried it wasn’t working out the way he hoped. Bob was right to be worried then and Montanans are right to be worried now because Trump’s Forest Service Chief and former timber industry lobbyist Tom Schultz, has just unleashed the “sustained yield” scam on Montana’s National Forests. …My advice to Bob was to let the bill die because he didn’t have the votes to remove the amendments the timber industry lobbyists stuck on the bill. But he didn’t take that advice. …Two years later, Tom Schultz went to work for Montana’s Department of Natural Resources and Conservation, earning the sobriquet “Chainsaw Tom” for his pro-logging zeal.

Nordic, Baltic and Austrian forest industry associations are calling for a realistic and enabling EU climate target for the land-use sector, warning that overly high expectations for forest carbon sinks could place unnecessary pressure on forestry and the bioeconomy. In a joint letter dated 24 June 2026, several European forest industry associations said the EU’s post-2030 climate framework should focus primarily on phasing out fossil emissions, while allowing the land-use sector to continue providing renewable raw materials and climate solutions. The associations argue that forests and the wider land-use sector provide sustainable biomass that can replace fossil-based or carbon-intensive products, materials and energy. They say this role is important for Europe’s transition towards a circular and climate-neutral bioeconomy.

Nordic, Baltic and Austrian forest industry associations are calling for a realistic and enabling EU climate target for the land-use sector, warning that overly high expectations for forest carbon sinks could place unnecessary pressure on forestry and the bioeconomy. In a joint letter dated 24 June 2026, several European forest industry associations said the EU’s post-2030 climate framework should focus primarily on phasing out fossil emissions, while allowing the land-use sector to continue providing renewable raw materials and climate solutions. The associations argue that forests and the wider land-use sector provide sustainable biomass that can replace fossil-based or carbon-intensive products, materials and energy. They say this role is important for Europe’s transition towards a circular and climate-neutral bioeconomy. LONDON — The world’s rainforests are to be better protected from deforestation as the government will confirm during London Climate Action Week, that plans to take forward new rules in Great Britain including using powers in the Environment Act alongside legislation strengthening the UK Timber Regulation. Under the proposals UK businesses who trade in commodities sourced from rainforests… will need to check that their supply chains are not contributing to illegal deforestation. …UK companies have been at the forefront of global efforts to tackle deforestation within their supply chains, but voluntary action alone cannot tackle this global challenge, and several major supermarkets have been calling for stronger regulation. Rainforests and other forests are vital for storing carbon and sustaining biodiversity, yet they are increasingly threatened by deforestation. … Rules will be enforced using powers in the Environment Act, alongside legislation strengthening existing timber rules.

LONDON — The world’s rainforests are to be better protected from deforestation as the government will confirm during London Climate Action Week, that plans to take forward new rules in Great Britain including using powers in the Environment Act alongside legislation strengthening the UK Timber Regulation. Under the proposals UK businesses who trade in commodities sourced from rainforests… will need to check that their supply chains are not contributing to illegal deforestation. …UK companies have been at the forefront of global efforts to tackle deforestation within their supply chains, but voluntary action alone cannot tackle this global challenge, and several major supermarkets have been calling for stronger regulation. Rainforests and other forests are vital for storing carbon and sustaining biodiversity, yet they are increasingly threatened by deforestation. … Rules will be enforced using powers in the Environment Act, alongside legislation strengthening existing timber rules. During the 1930s, Italy’s government launched a sweeping reforestation effort in the Prealps region near Lake Como, planting fast-growing Norway spruce on land that had been pasture and meadow for centuries. It was a conscious decision, made mainly to answer the demand for timber, but it did not involve much ecological thinking. Now, 90 years later, a new study has gone back to measure what that decision actually did to the landscape, and the results are not flattering. According to the study, ‘

During the 1930s, Italy’s government launched a sweeping reforestation effort in the Prealps region near Lake Como, planting fast-growing Norway spruce on land that had been pasture and meadow for centuries. It was a conscious decision, made mainly to answer the demand for timber, but it did not involve much ecological thinking. Now, 90 years later, a new study has gone back to measure what that decision actually did to the landscape, and the results are not flattering. According to the study, ‘ JAKARTA — Pulp and paper giant APRIL’s recent decision to lower its deforestation commitments and source wood from two companies associated with extensive recent forest loss has created a new challenge for its relationship with the Forest Stewardship Council (FSC), with environmental groups urging the world’s leading forestry certifier to terminate the already suspended reassociation process. In late May, APRIL announced it was reviewing its decade-old Sustainable Forest Management Policy 2.0 and lowering its deforestation cutoff date from 2015 to Dec. 31, 2020. The move allows the pulp and paper producer to source wood from PT Industrial Forest Plantation and PT Mayawana Persada, two companies that have experienced some of the country’s largest recent forest losses. APRIL said the decision was necessary to address fibre shortages after the Indonesian government revoked the operating permits of four of its long-term suppliers earlier this year, affecting around 15% of its wood supply in Riau Province.

JAKARTA — Pulp and paper giant APRIL’s recent decision to lower its deforestation commitments and source wood from two companies associated with extensive recent forest loss has created a new challenge for its relationship with the Forest Stewardship Council (FSC), with environmental groups urging the world’s leading forestry certifier to terminate the already suspended reassociation process. In late May, APRIL announced it was reviewing its decade-old Sustainable Forest Management Policy 2.0 and lowering its deforestation cutoff date from 2015 to Dec. 31, 2020. The move allows the pulp and paper producer to source wood from PT Industrial Forest Plantation and PT Mayawana Persada, two companies that have experienced some of the country’s largest recent forest losses. APRIL said the decision was necessary to address fibre shortages after the Indonesian government revoked the operating permits of four of its long-term suppliers earlier this year, affecting around 15% of its wood supply in Riau Province. AUSTRALIA — Tasmania’s public native forestry company has corrected the record in a parliamentary committee after earlier stating that all logs from public native forests were processed in Tasmania. Tasmanian sawmill operator James Neville-Smith confirmed that some logs had been sent to Victoria, where processors had received compensation from the Victorian government as part of its industry shutdown. Mr Neville-Smith said the decision was due to retooling a sawmill to be plantation-only, meaning that hardwood logs needed to be processed elsewhere. Logs displaying stickers from Tasmanian state forests were also spotted at a mill in Powelltown, in the Yarra Valley, that was also a recipient of millions in Victorian compensation payments. Victoria phased out native forest logging in 2024. Since then, environmental groups have raised concerns about large quantities of logs being transported to Victoria on the Spirit of Tasmania, but were told that all were from private forests.

AUSTRALIA — Tasmania’s public native forestry company has corrected the record in a parliamentary committee after earlier stating that all logs from public native forests were processed in Tasmania. Tasmanian sawmill operator James Neville-Smith confirmed that some logs had been sent to Victoria, where processors had received compensation from the Victorian government as part of its industry shutdown. Mr Neville-Smith said the decision was due to retooling a sawmill to be plantation-only, meaning that hardwood logs needed to be processed elsewhere. Logs displaying stickers from Tasmanian state forests were also spotted at a mill in Powelltown, in the Yarra Valley, that was also a recipient of millions in Victorian compensation payments. Victoria phased out native forest logging in 2024. Since then, environmental groups have raised concerns about large quantities of logs being transported to Victoria on the Spirit of Tasmania, but were told that all were from private forests. UK — The City watchdog has closed an investigation into the owner of the Drax power plant after an almost 10-month review into whether the company’s sustainability claims mislead shareholders. The Financial Conduct Authority said it had “reviewed thousands of pages” of “complex material” relating to the company’s sourcing of wood pellets for the Drax power plant in Selby, North Yorkshire, but “did not find evidence that justified any further action”. The regulator began the investigation last year into whether Drax’s annual reports and accounts between 2021 and 2023 misled shareholders or left out important information investors needed to know about the origins of its biomass fuel. …Ofgem found at the time that there was no evidence to suggest the breach was deliberate, and said instead that it was “technical in nature”. It also found no evidence that the biomass sourced was unsustainable or that Drax had wrongly laid claim to renewable energy subsidies.

UK — The City watchdog has closed an investigation into the owner of the Drax power plant after an almost 10-month review into whether the company’s sustainability claims mislead shareholders. The Financial Conduct Authority said it had “reviewed thousands of pages” of “complex material” relating to the company’s sourcing of wood pellets for the Drax power plant in Selby, North Yorkshire, but “did not find evidence that justified any further action”. The regulator began the investigation last year into whether Drax’s annual reports and accounts between 2021 and 2023 misled shareholders or left out important information investors needed to know about the origins of its biomass fuel. …Ofgem found at the time that there was no evidence to suggest the breach was deliberate, and said instead that it was “technical in nature”. It also found no evidence that the biomass sourced was unsustainable or that Drax had wrongly laid claim to renewable energy subsidies. OTTAWA — Three young women and two environmental groups on Tuesday filed a lawsuit against the Canadian government seeking to force it to develop an action plan to meet its key climate goals. The lawsuit comes as Prime Minister Mark Carney’s government shifts Canada’s climate and energy priorities, rolling back key environmental policies while advancing major energy and infrastructure projects to reduce dependence on the United States. Announcing the lawsuit, plaintiff Shirley Barnea, a university student from Quebec, said authorities had an obligation to build a sustainable future for younger generations. …The legal action aims to compel the government “to chart a credible, up-to-date course of action” and “to protect Canadians from the worsening impacts of climate change,” according to a statement from the Canadian Association of Physicians for the Environment (CAPE), which is also a party to the lawsuit.

OTTAWA — Three young women and two environmental groups on Tuesday filed a lawsuit against the Canadian government seeking to force it to develop an action plan to meet its key climate goals. The lawsuit comes as Prime Minister Mark Carney’s government shifts Canada’s climate and energy priorities, rolling back key environmental policies while advancing major energy and infrastructure projects to reduce dependence on the United States. Announcing the lawsuit, plaintiff Shirley Barnea, a university student from Quebec, said authorities had an obligation to build a sustainable future for younger generations. …The legal action aims to compel the government “to chart a credible, up-to-date course of action” and “to protect Canadians from the worsening impacts of climate change,” according to a statement from the Canadian Association of Physicians for the Environment (CAPE), which is also a party to the lawsuit.