I am surprised at how President Trump is gradually succeeding in his goal. …Canada, along with China, is the only country standing up to the US, but it is inevitable that if no agreement is reached, the chances of a recession will increase. …Canada needs the US to avoid the worst, but the point of the article is different: how much does the US need Canada? My impression is that this issue is often underestimated. …We don’t need their lumber. But is that really the case? …Why Canadian lumber is essential. …The first and probably most important reason is that US forests are mainly privately owned (by companies or families). …Becoming less dependent on Canada is extremely complicated for the US due to the usual logistical challenges. …This industry has been in gradual decline for decades, and wanting to save it in order to be less dependent on Canada is a waste of resources.

I am surprised at how President Trump is gradually succeeding in his goal. …Canada, along with China, is the only country standing up to the US, but it is inevitable that if no agreement is reached, the chances of a recession will increase. …Canada needs the US to avoid the worst, but the point of the article is different: how much does the US need Canada? My impression is that this issue is often underestimated. …We don’t need their lumber. But is that really the case? …Why Canadian lumber is essential. …The first and probably most important reason is that US forests are mainly privately owned (by companies or families). …Becoming less dependent on Canada is extremely complicated for the US due to the usual logistical challenges. …This industry has been in gradual decline for decades, and wanting to save it in order to be less dependent on Canada is a waste of resources.

The U.S. Commerce Department has announced it is nearly tripling its anti-dumping duties on Canadian lumber imports from 7.66% to 20.56% following its annual review of existing tariffs. The anti-dumping duties are in addition to current countervailing duties set at 6.74%, which would bring the total lumber duties above 27%. However, the countervailing duty rate is expected to move higher on Aug. 8. Commerce issued a preliminary determination on countervailing duties earlier this year that would raise the countervailing duty rate to 14.38%. Moreover, President Trump’s Section 232 [investigation] could result in higher lumber tariffs. …For years, NAHB has been leading the fight against lumber tariffs because of their detrimental effect on housing affordability. In effect, the lumber tariffs act as a tax on American builders, home buyers and consumers. …We are also urging the administration to move immediately to enter into negotiations with Canada on a new softwood lumber agreement that will… eliminate tariffs altogether.

The U.S. Commerce Department has announced it is nearly tripling its anti-dumping duties on Canadian lumber imports from 7.66% to 20.56% following its annual review of existing tariffs. The anti-dumping duties are in addition to current countervailing duties set at 6.74%, which would bring the total lumber duties above 27%. However, the countervailing duty rate is expected to move higher on Aug. 8. Commerce issued a preliminary determination on countervailing duties earlier this year that would raise the countervailing duty rate to 14.38%. Moreover, President Trump’s Section 232 [investigation] could result in higher lumber tariffs. …For years, NAHB has been leading the fight against lumber tariffs because of their detrimental effect on housing affordability. In effect, the lumber tariffs act as a tax on American builders, home buyers and consumers. …We are also urging the administration to move immediately to enter into negotiations with Canada on a new softwood lumber agreement that will… eliminate tariffs altogether. The US Lumber Coalition (USLC) has aggressively promoted strong enforcement of US trade laws and railed against “unfair Canadian trade practices.” …The USLC’s arguments have been challenged by a pair of Canadian independent consultants — Russ Taylor Global and Spar Tree Group:

The US Lumber Coalition (USLC) has aggressively promoted strong enforcement of US trade laws and railed against “unfair Canadian trade practices.” …The USLC’s arguments have been challenged by a pair of Canadian independent consultants — Russ Taylor Global and Spar Tree Group: OTTAWA—Home buyers and builders in Canada are in retreat, adding to the woes of an economy struggling under the weight of President Trump’s tariffs. Housing helped spur growth in Canada just prior to, and after the worst of, the Covid-19 pandemic. …Data this month indicated existing-home sales climbed modestly for three straight months as of June. But economists and real estate agents are far from convinced it signals recovery after a tariff-fueled slowdown. They note the sales rebound was the result of sellers cutting their listing price. Housing affordability remains stretched in Canada, according to the Bank of Canada data. …For builders, prices for new homes are failing to cover higher costs for labor, loans and taxes and fees set at the municipal level. The Canadian Home Builders’ Association said its own confidence index is at historically pessimistic levels. [to access the full story a WSJ subscription is required]

OTTAWA—Home buyers and builders in Canada are in retreat, adding to the woes of an economy struggling under the weight of President Trump’s tariffs. Housing helped spur growth in Canada just prior to, and after the worst of, the Covid-19 pandemic. …Data this month indicated existing-home sales climbed modestly for three straight months as of June. But economists and real estate agents are far from convinced it signals recovery after a tariff-fueled slowdown. They note the sales rebound was the result of sellers cutting their listing price. Housing affordability remains stretched in Canada, according to the Bank of Canada data. …For builders, prices for new homes are failing to cover higher costs for labor, loans and taxes and fees set at the municipal level. The Canadian Home Builders’ Association said its own confidence index is at historically pessimistic levels. [to access the full story a WSJ subscription is required] As a tariff storm blew in from south of the border earlier this year, many industries in Canada, including the home building sector, feared the unknown ahead of them. With stakeholders already keenly aware of the need to rapidly scale up housing supply and improve Canada’s housing affordability gap, blanket tariffs and more targeted material-specific levies meant additional unwelcome obstacles to overcome. That included a potential need to slow down the pace of construction as supply chains shifted and key construction parts became more expensive. …About six months after US President Trump’s return to the White House, many in the home construction sector say unpredictability persists around the cost and timing of obtaining the materials they need. For Geranium Homes, a residential developer in southern Ontario, that’s meant having to pivot on the fly when it comes to the supply chains it’s long relied on.

As a tariff storm blew in from south of the border earlier this year, many industries in Canada, including the home building sector, feared the unknown ahead of them. With stakeholders already keenly aware of the need to rapidly scale up housing supply and improve Canada’s housing affordability gap, blanket tariffs and more targeted material-specific levies meant additional unwelcome obstacles to overcome. That included a potential need to slow down the pace of construction as supply chains shifted and key construction parts became more expensive. …About six months after US President Trump’s return to the White House, many in the home construction sector say unpredictability persists around the cost and timing of obtaining the materials they need. For Geranium Homes, a residential developer in southern Ontario, that’s meant having to pivot on the fly when it comes to the supply chains it’s long relied on. A CUSMA Chapter 10 binational panel remanded [for further explanation] two statistical methodologies in the US Department of Commerce’s Administrative Review 1 antidumping duty determination on Canadian softwood lumber, requiring Commerce to reassess its use of the Cohen’s d test and to apply weighted pooled variances in its meaningful-difference analysis according to the panel’s Decision and Order. …The panel affirmed all other aspect of the results challenged in this appeal…The review stems from a December 22, 2020 request by Resolute Forest Products and the Ontario Forest Industries Association. …The panel remanded Commerce’s application of Cohen’s d because the Federal Circuit’s decision in Marmen Inc. v. United States Wind Tower Trade Coalition requires that the test’s key assumptions, normal data distribution, equal variances and adequate sample size, be demonstrated before use. …The panel also remanded Commerce’s pooling of variances, directing the Department to use weighted pooled variances that reflect differing sample sizes. …Commerce must respond by October 20, 2025.

A CUSMA Chapter 10 binational panel remanded [for further explanation] two statistical methodologies in the US Department of Commerce’s Administrative Review 1 antidumping duty determination on Canadian softwood lumber, requiring Commerce to reassess its use of the Cohen’s d test and to apply weighted pooled variances in its meaningful-difference analysis according to the panel’s Decision and Order. …The panel affirmed all other aspect of the results challenged in this appeal…The review stems from a December 22, 2020 request by Resolute Forest Products and the Ontario Forest Industries Association. …The panel remanded Commerce’s application of Cohen’s d because the Federal Circuit’s decision in Marmen Inc. v. United States Wind Tower Trade Coalition requires that the test’s key assumptions, normal data distribution, equal variances and adequate sample size, be demonstrated before use. …The panel also remanded Commerce’s pooling of variances, directing the Department to use weighted pooled variances that reflect differing sample sizes. …Commerce must respond by October 20, 2025. Lumber markets remained flat this week as vacation time, industry gatherings, sweltering heat and general economic uncertainty contributed to sluggish sales. Minimal immediate needs limited replenishment purchases to modest volumes while a lack of clarity regarding near-term prospects stifled speculative trading across North American framing lumber markets. 2×4 led gains in many species, but the increases were modest. Seasonal factors, including unusually heavy rainfall and normal summer heat, contributed to the ongoing sluggish pace across the South. Mills worked hard to capture modest premiums. The coming hike in duties on Canadian shipments to the US did little to alter the ongoing lack of urgency among buyers. …Sales of Western S-P-F were governed by tepid demand and uncertainty regarding the timing and scope of higher duties and potential tariffs. …Sales in the Coast region were lukewarm with most lumber markets trends holding.

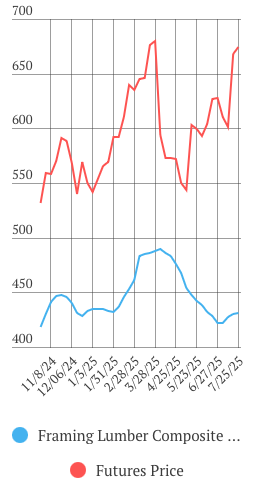

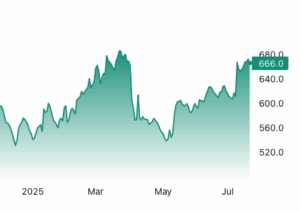

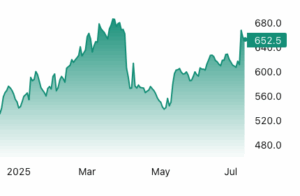

Lumber markets remained flat this week as vacation time, industry gatherings, sweltering heat and general economic uncertainty contributed to sluggish sales. Minimal immediate needs limited replenishment purchases to modest volumes while a lack of clarity regarding near-term prospects stifled speculative trading across North American framing lumber markets. 2×4 led gains in many species, but the increases were modest. Seasonal factors, including unusually heavy rainfall and normal summer heat, contributed to the ongoing sluggish pace across the South. Mills worked hard to capture modest premiums. The coming hike in duties on Canadian shipments to the US did little to alter the ongoing lack of urgency among buyers. …Sales of Western S-P-F were governed by tepid demand and uncertainty regarding the timing and scope of higher duties and potential tariffs. …Sales in the Coast region were lukewarm with most lumber markets trends holding.  Lumber futures traded above $680 per thousand board feet, approaching the two-and-a-half-year peak of $685 recorded on March?24th, driven by a squeeze on supply meeting unfaltering construction demand. On the demand front, US housing starts held surprisingly steady at an annualized 1.6?million units in June even as existing-home sales slipped 2.7% to a nine-month low, ensuring that framing requirements remained robust. At the same time, US softwood lumber tariffs on Canadian imports continue to add roughly 9% to landed costs, while Pacific Northwest mills have withdrawn nearly 20% of regional capacity for mid-season maintenance, sharply curtailing shipments to distributors. Internationally, imports from Europe and New?Zealand are throttled by 25% duties on Russian lumber and persistent ocean-freight bottlenecks, collectively depleting distributor inventories to their lowest levels in more than two years and reinforcing today’s sharp advance in futures prices. [END]

Lumber futures traded above $680 per thousand board feet, approaching the two-and-a-half-year peak of $685 recorded on March?24th, driven by a squeeze on supply meeting unfaltering construction demand. On the demand front, US housing starts held surprisingly steady at an annualized 1.6?million units in June even as existing-home sales slipped 2.7% to a nine-month low, ensuring that framing requirements remained robust. At the same time, US softwood lumber tariffs on Canadian imports continue to add roughly 9% to landed costs, while Pacific Northwest mills have withdrawn nearly 20% of regional capacity for mid-season maintenance, sharply curtailing shipments to distributors. Internationally, imports from Europe and New?Zealand are throttled by 25% duties on Russian lumber and persistent ocean-freight bottlenecks, collectively depleting distributor inventories to their lowest levels in more than two years and reinforcing today’s sharp advance in futures prices. [END] President Trump’s tariffs could have an unintended side effect: making homeownership even less affordable for many Americans. A new report from the Canadian Chamber of Commerce estimates that the average cost of building a US home could rise by an additional $14,000 by the end of 2027 if tariffs on Canadian imports remain in place, even as many experts estimate that America needs millions more affordable homes. In 2023 alone, Canada accounted for 69% of US lumber imports, 25% of imported iron and steel and 18% of copper imports, all key construction materials, the report said. The White House pushed back on the assertion that tariffs would increase costs for Americans. …The report underscores that Trump’s tariff policy, intended to support American industry, may instead worsen housing affordability. Taking into account tariffs first imposed during Trump’s first term, the total added cost from tariffs could reach $20,000 per home by 2027, the Canadian Chamber of Commerce found.

President Trump’s tariffs could have an unintended side effect: making homeownership even less affordable for many Americans. A new report from the Canadian Chamber of Commerce estimates that the average cost of building a US home could rise by an additional $14,000 by the end of 2027 if tariffs on Canadian imports remain in place, even as many experts estimate that America needs millions more affordable homes. In 2023 alone, Canada accounted for 69% of US lumber imports, 25% of imported iron and steel and 18% of copper imports, all key construction materials, the report said. The White House pushed back on the assertion that tariffs would increase costs for Americans. …The report underscores that Trump’s tariff policy, intended to support American industry, may instead worsen housing affordability. Taking into account tariffs first imposed during Trump’s first term, the total added cost from tariffs could reach $20,000 per home by 2027, the Canadian Chamber of Commerce found. During April’s election campaign, the Carney government promised to double the pace of homebuilding in Canada by 2035—an unlikely outcome in light of Canada’s shortage of construction workers and investment dollars. But even if homebuilding were miraculously doubled, it would not solve Canada’s housing affordability crisis. That’s the sobering conclusion of a recent

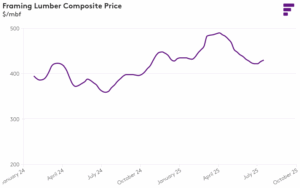

During April’s election campaign, the Carney government promised to double the pace of homebuilding in Canada by 2035—an unlikely outcome in light of Canada’s shortage of construction workers and investment dollars. But even if homebuilding were miraculously doubled, it would not solve Canada’s housing affordability crisis. That’s the sobering conclusion of a recent  Lumber futures traded above $650 per thousand board feet, hovering near April highs driven by tightening US sawmill output and dwindling import volumes, both of which are near their lowest levels in half a decade. Domestic production in the first quarter slipped year-on-year, and imports, including softwood lumber from Canada, have contracted sharply, leaving US framing material availability at its leanest since 2019. At the same time, builders are contending with looming tariff hikes that could push duties on Canadian lumber from roughly 14.5% today toward the mid-30s, adding several thousand dollars to the cost of new homes. Although a modest pull-back in construction activity has softened recent gains, overall demand remains sufficient to absorb current supply, and without a rapid expansion in US mill capacity or alternative sourcing, these supply constraints, compounded by rising trade barriers, are likely to sustain upward pressure on lumber prices in the months ahead.

Lumber futures traded above $650 per thousand board feet, hovering near April highs driven by tightening US sawmill output and dwindling import volumes, both of which are near their lowest levels in half a decade. Domestic production in the first quarter slipped year-on-year, and imports, including softwood lumber from Canada, have contracted sharply, leaving US framing material availability at its leanest since 2019. At the same time, builders are contending with looming tariff hikes that could push duties on Canadian lumber from roughly 14.5% today toward the mid-30s, adding several thousand dollars to the cost of new homes. Although a modest pull-back in construction activity has softened recent gains, overall demand remains sufficient to absorb current supply, and without a rapid expansion in US mill capacity or alternative sourcing, these supply constraints, compounded by rising trade barriers, are likely to sustain upward pressure on lumber prices in the months ahead.

OTTAWA — Canada’s annual inflation rate rose to 1.9% in June, meeting analysts’ expectations, as increases in the price of automobiles and clothing and footwear pushed the index higher, data showed on Tuesday. The consumer price index was at 1.7% in the prior month. Statistics Canada said on a monthly basis the CPI increased 0.1%, matching analysts’ forecasts. It is for the third month in a row that the CPI has been under 2%, or the mid-point of Bank of Canada’s inflation target range. This is the last major economic indicator to be released before the Bank of Canada’s rates decision later this month. The slight rise in prices across many segments, along with a strong jobs number last week, is likely to take away any incentive to cut interest rates, economists had earlier predicted. …Shelter prices rose by 2.9%, its first drop below 3% in more than four years.

OTTAWA — Canada’s annual inflation rate rose to 1.9% in June, meeting analysts’ expectations, as increases in the price of automobiles and clothing and footwear pushed the index higher, data showed on Tuesday. The consumer price index was at 1.7% in the prior month. Statistics Canada said on a monthly basis the CPI increased 0.1%, matching analysts’ forecasts. It is for the third month in a row that the CPI has been under 2%, or the mid-point of Bank of Canada’s inflation target range. This is the last major economic indicator to be released before the Bank of Canada’s rates decision later this month. The slight rise in prices across many segments, along with a strong jobs number last week, is likely to take away any incentive to cut interest rates, economists had earlier predicted. …Shelter prices rose by 2.9%, its first drop below 3% in more than four years. US and Chinese negotiators have agreed in principle to push back the deadline for escalating tariffs, although America’s representatives said any extension would need Donald Trump’s approval. Officials from both sides said after two days of talks in Stockholm that while had failed to find a resolution across the many areas of dispute they had agreed to extend a pause due to run out on 12 August. Beijing’s top trade negotiator, Li Chenggang, said the extension of a truce struck in mid-May would allow for further talks, without specifying when and for how long the latest pause would run. However, the US trade representative Jamieson Greer stressed that President Trump would have the “final call” on any extension. …Trump is on course to impose extra tariffs on Mexico and Canada from Friday, barring last-minute deals.

US and Chinese negotiators have agreed in principle to push back the deadline for escalating tariffs, although America’s representatives said any extension would need Donald Trump’s approval. Officials from both sides said after two days of talks in Stockholm that while had failed to find a resolution across the many areas of dispute they had agreed to extend a pause due to run out on 12 August. Beijing’s top trade negotiator, Li Chenggang, said the extension of a truce struck in mid-May would allow for further talks, without specifying when and for how long the latest pause would run. However, the US trade representative Jamieson Greer stressed that President Trump would have the “final call” on any extension. …Trump is on course to impose extra tariffs on Mexico and Canada from Friday, barring last-minute deals.

.png)

An earlier post described how the top 10 builders

An earlier post described how the top 10 builders

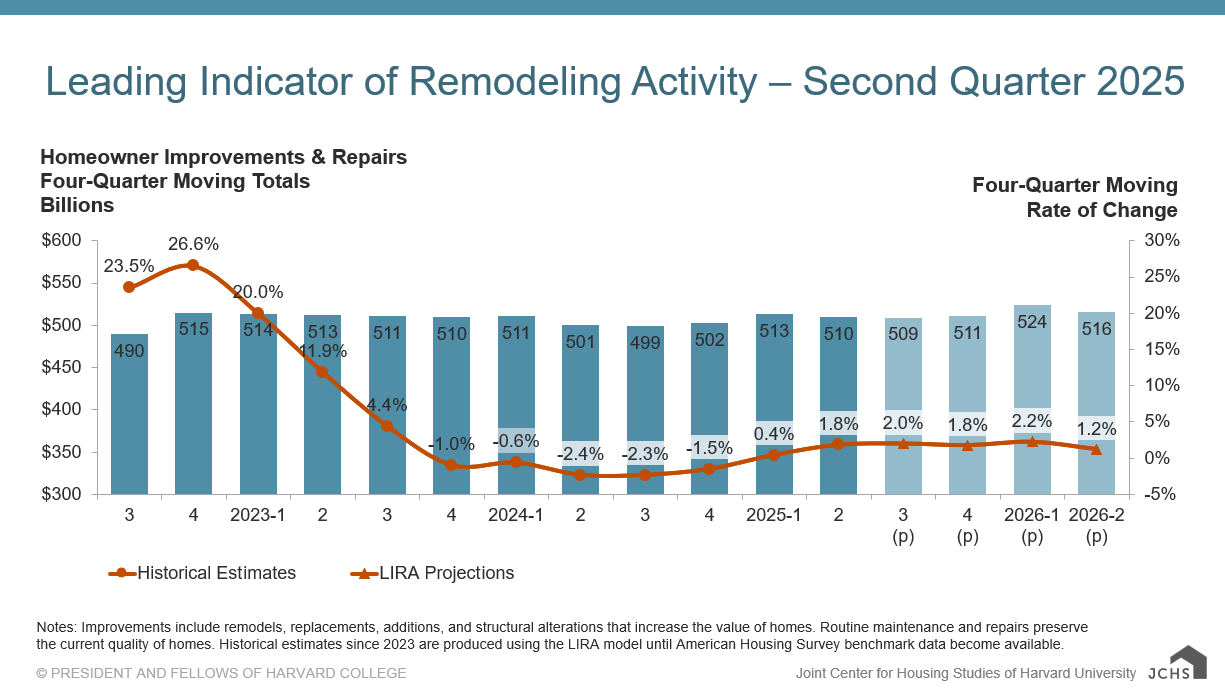

In the second quarter of 2025, the NAHB/Westlake Royal Remodeling Market Index (RMI) posted a reading of 59, down four points compared to the previous quarter. While this reading is still in positive territory, some remodelers, especially in the West, are seeing a slowing of activity in their markets. The second-quarter reading of 59 marks only the second time the RMI has dipped below 60 since the survey was revised in the first quarter of 2020. Higher interest rates and general economic uncertainty have affected consumer confidence and are headwinds for remodeling, but not to the extent that they have been for single-family construction, as is evident in June’s negative reading from the NAHB/Wells Fargo Housing Marketing Index (HMI). As a result, NAHB is still forecasting solid gains for remodeling spending in 2025, followed by more modest, but still positive, growth in 2026. …The Current Conditions Index averaged 66, down five points from the previous quarter.

In the second quarter of 2025, the NAHB/Westlake Royal Remodeling Market Index (RMI) posted a reading of 59, down four points compared to the previous quarter. While this reading is still in positive territory, some remodelers, especially in the West, are seeing a slowing of activity in their markets. The second-quarter reading of 59 marks only the second time the RMI has dipped below 60 since the survey was revised in the first quarter of 2020. Higher interest rates and general economic uncertainty have affected consumer confidence and are headwinds for remodeling, but not to the extent that they have been for single-family construction, as is evident in June’s negative reading from the NAHB/Wells Fargo Housing Marketing Index (HMI). As a result, NAHB is still forecasting solid gains for remodeling spending in 2025, followed by more modest, but still positive, growth in 2026. …The Current Conditions Index averaged 66, down five points from the previous quarter.  Economists, researchers and analysts have warned that President Trump’s tariffs on most goods will deliver a taxing blow to consumers via higher prices. However, recent months’ economic data has shown that overall inflation has remained fairly tame. Trump touts the positive economic reports as signs that tariffs are working. However, the chorus of concern is growing: Prices are moving higher, and economists say this is just the beginning. Here’s a look at the mechanisms behind why price hikes, and hotter inflation, are a slow burn: Tariffs have been applied in a staggered manner; …Trade policy and tariffs are in flux; …Shipping takes time; …Domestic supply chains take time, too; …Inventories were loaded up before tariffs hit; …Some costs are being eaten; …Businesses are hesitant to pass on higher prices; …Awareness of goods prices is lower in summer than fall and winter; …Economic data is often lagged; …Inflation indices are comprehensive.

Economists, researchers and analysts have warned that President Trump’s tariffs on most goods will deliver a taxing blow to consumers via higher prices. However, recent months’ economic data has shown that overall inflation has remained fairly tame. Trump touts the positive economic reports as signs that tariffs are working. However, the chorus of concern is growing: Prices are moving higher, and economists say this is just the beginning. Here’s a look at the mechanisms behind why price hikes, and hotter inflation, are a slow burn: Tariffs have been applied in a staggered manner; …Trade policy and tariffs are in flux; …Shipping takes time; …Domestic supply chains take time, too; …Inventories were loaded up before tariffs hit; …Some costs are being eaten; …Businesses are hesitant to pass on higher prices; …Awareness of goods prices is lower in summer than fall and winter; …Economic data is often lagged; …Inflation indices are comprehensive. UK softwood traders enjoyed a period of strong trading through the first two months of Q2, supported by a rise in demand gaining momentum through both April and May. This followed on from a stable Q1 when imports increased by just under 2% against the same period in 2024. Since the beginning of this year, a number of Nordic producers were short of spruce logs for structural grades, and in many cases switched to pine. That move had a knock-on effect on the amount of redwood available for production at some mills. With good demand and some shortages, Q2 prices moved upwards, not only to the UK but other markets in Europe and the US as well. However, the UK merchants adopted a more sceptical and cautious approach. Many held back from making longer-term commitments on the forward market to ensure the recovery and stability in the market was sustainable.

UK softwood traders enjoyed a period of strong trading through the first two months of Q2, supported by a rise in demand gaining momentum through both April and May. This followed on from a stable Q1 when imports increased by just under 2% against the same period in 2024. Since the beginning of this year, a number of Nordic producers were short of spruce logs for structural grades, and in many cases switched to pine. That move had a knock-on effect on the amount of redwood available for production at some mills. With good demand and some shortages, Q2 prices moved upwards, not only to the UK but other markets in Europe and the US as well. However, the UK merchants adopted a more sceptical and cautious approach. Many held back from making longer-term commitments on the forward market to ensure the recovery and stability in the market was sustainable. Timber and forestry investment is gaining ground in Europe, as private equity increasingly shifts towards climate-aligned strategies. A recent EY report highlights growing momentum behind timber and forestry funds, previously seen as niche, now positioned as core components of sustainability-focused portfolios. Despite global private equity fundraising falling to $680 billion in 2024, the lowest since 2015, investors are favouring fewer, larger deals. Europe is leading in sustainable asset allocation, with over half of all new fund launches in Article 8 and 9 categories under the EU Sustainable Finance Disclosure Regulation, according to Morningstar. Timber and forestry funds attracted $8.4 billion in 2024, slightly down from 2023 but above the five-year average. These funds often deliver double-digit internal rates of return, with top-performing vintages exceeding 16 percent.

Timber and forestry investment is gaining ground in Europe, as private equity increasingly shifts towards climate-aligned strategies. A recent EY report highlights growing momentum behind timber and forestry funds, previously seen as niche, now positioned as core components of sustainability-focused portfolios. Despite global private equity fundraising falling to $680 billion in 2024, the lowest since 2015, investors are favouring fewer, larger deals. Europe is leading in sustainable asset allocation, with over half of all new fund launches in Article 8 and 9 categories under the EU Sustainable Finance Disclosure Regulation, according to Morningstar. Timber and forestry funds attracted $8.4 billion in 2024, slightly down from 2023 but above the five-year average. These funds often deliver double-digit internal rates of return, with top-performing vintages exceeding 16 percent.