OTTAWA — The six-month trend in housing starts was higher in April, with an increase of 3.2% to 256,777 units, according to Canada Mortgage and Housing Corporation (CMHC). The trend measure is a six-month moving average of the seasonally adjusted annual rate (SAAR) of total housing starts for all areas in Canada. Actual housing starts were down 1% year-over-year in centres with a population of 10,000 or greater, with 21,805 units recorded in April, compared to 21,938 units in April 2025. The year-to-date total was 71,011 units, up 6% from the same period in 2025, driven by higher starts in British Columbia and Ontario. The total monthly SAAR of housing starts for all areas in Canada increased 17% in April (279,317 units) compared to March (239,747 units).

OTTAWA — The six-month trend in housing starts was higher in April, with an increase of 3.2% to 256,777 units, according to Canada Mortgage and Housing Corporation (CMHC). The trend measure is a six-month moving average of the seasonally adjusted annual rate (SAAR) of total housing starts for all areas in Canada. Actual housing starts were down 1% year-over-year in centres with a population of 10,000 or greater, with 21,805 units recorded in April, compared to 21,938 units in April 2025. The year-to-date total was 71,011 units, up 6% from the same period in 2025, driven by higher starts in British Columbia and Ontario. The total monthly SAAR of housing starts for all areas in Canada increased 17% in April (279,317 units) compared to March (239,747 units).

The Bank of Canada held its policy interest rate at 2.25 per cent for the fourth consecutive time on Wednesday, but warned that it would be closely watching the impact of rising oil prices on inflation in the coming months amid ongoing uncertainty caused by the war in Iran. …Inflation has been close to two per cent for over a year but rose to 2.4 per cent in March after slowing to 1.8 per cent in February. The central bank base case forecast is that inflation will peak in April at about three per cent before returning to the two per cent target in early 2027, but that is assuming global oil prices decline. U.S. tariff measures along with the uncertainty surrounding the Canada-United-States-Mexico Agreement (CUSMA) have also added to the uncertainty ahead of the July 1 CUSMA review deadline, especially since the Canadian government has not yet launched formal discussions with U.S. officials.

The Bank of Canada held its policy interest rate at 2.25 per cent for the fourth consecutive time on Wednesday, but warned that it would be closely watching the impact of rising oil prices on inflation in the coming months amid ongoing uncertainty caused by the war in Iran. …Inflation has been close to two per cent for over a year but rose to 2.4 per cent in March after slowing to 1.8 per cent in February. The central bank base case forecast is that inflation will peak in April at about three per cent before returning to the two per cent target in early 2027, but that is assuming global oil prices decline. U.S. tariff measures along with the uncertainty surrounding the Canada-United-States-Mexico Agreement (CUSMA) have also added to the uncertainty ahead of the July 1 CUSMA review deadline, especially since the Canadian government has not yet launched formal discussions with U.S. officials. Lumber futures fell to $566 per thousand board feet, the lowest in seven weeks, as broader uncertainty and ongoing trade tensions weigh on sentiment. The US has recently outlined preliminary antidumping and countervailing duties on Canadian softwood lumber, with the antidumping rate reduced from 20.

Lumber futures fell to $566 per thousand board feet, the lowest in seven weeks, as broader uncertainty and ongoing trade tensions weigh on sentiment. The US has recently outlined preliminary antidumping and countervailing duties on Canadian softwood lumber, with the antidumping rate reduced from 20. RUSS TAYLOR provided the latest quarterly report from the

RUSS TAYLOR provided the latest quarterly report from the

Premier David Eby’s plummeting approval numbers aren’t the only figures the NDP government needs to worry about when it comes to the backlash over Indigenous reconciliation and private property rights. Many B.C. businesses are reporting they plan to scale back operations due to the conflict as well. Almost 74 per cent of B.C. businesses plan to decrease investment due to uncertainty over the Declaration on the Rights of Indigenous Peoples Act, according to a new survey of senior executives Wednesday by the Business Council of B.C. The majority cite increased time, cost, complexity or uncertainty in permitting caused by the court rulings, policy flips and changing landscape around the NDP’s DRIPA. As many as one-third said they plan to reduce hiring. “The desire to work with Indigenous communities to create prosperity for all remains strong but the message from business leaders is clear: DRIPA isn’t working,” said BCBC president Laura Jones.

Premier David Eby’s plummeting approval numbers aren’t the only figures the NDP government needs to worry about when it comes to the backlash over Indigenous reconciliation and private property rights. Many B.C. businesses are reporting they plan to scale back operations due to the conflict as well. Almost 74 per cent of B.C. businesses plan to decrease investment due to uncertainty over the Declaration on the Rights of Indigenous Peoples Act, according to a new survey of senior executives Wednesday by the Business Council of B.C. The majority cite increased time, cost, complexity or uncertainty in permitting caused by the court rulings, policy flips and changing landscape around the NDP’s DRIPA. As many as one-third said they plan to reduce hiring. “The desire to work with Indigenous communities to create prosperity for all remains strong but the message from business leaders is clear: DRIPA isn’t working,” said BCBC president Laura Jones.

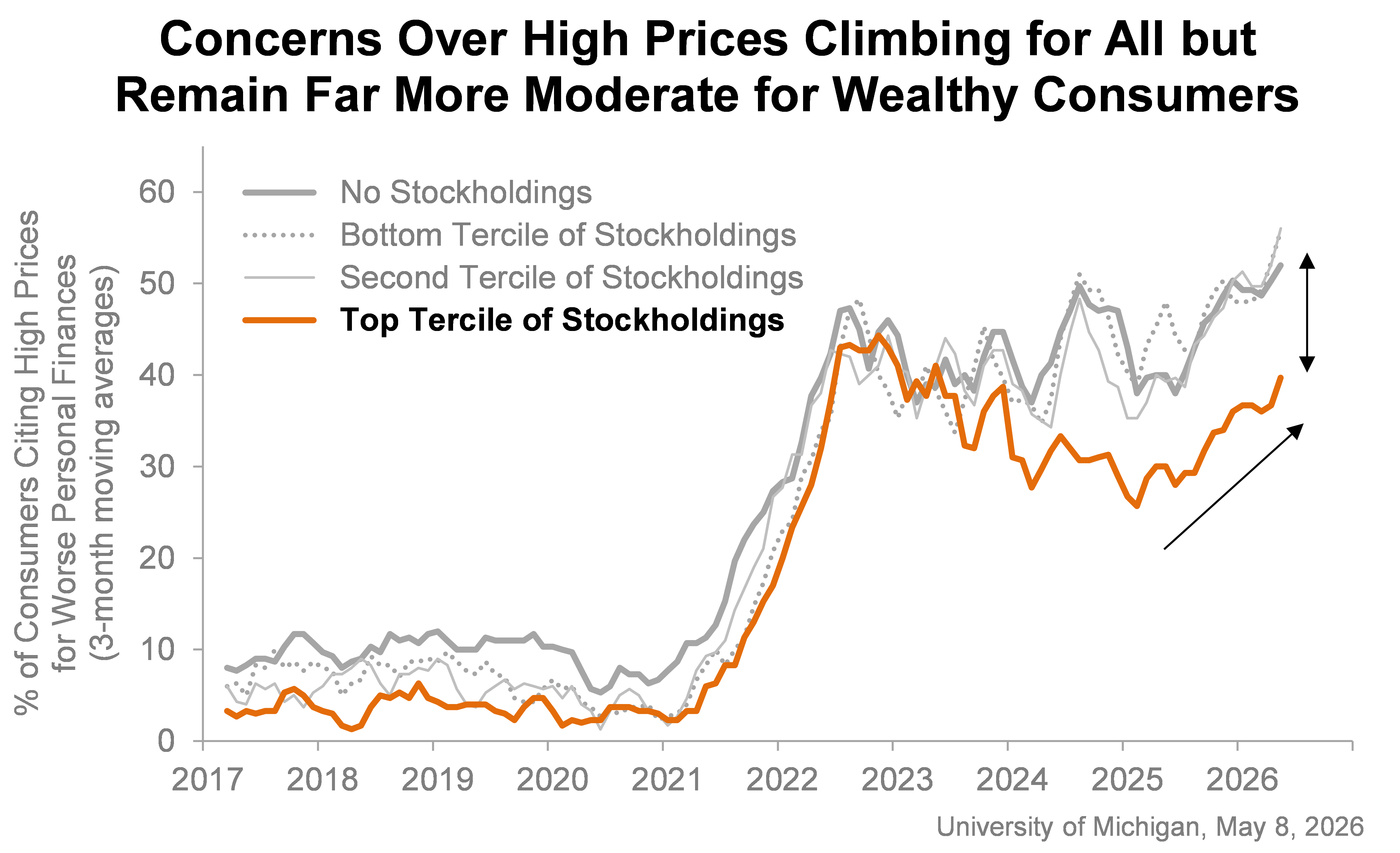

WASHINGTON — U.S. consumer confidence unexpectedly edged higher in April amid a rally in share prices following a ceasefire in the war with Iran and improved perceptions of the labor market, helping to ease households’ financial worries for now. Despite the rise in confidence to a four-month high, the survey from the Conference Board on Tuesday showed higher gasoline prices stemming from the conflict with Iran remained a source of concern for consumers. Fewer planned vacations over the next six months and the share of those intending to drive to their holiday destinations was the lowest since April 2020. …The Conference Board said its consumer confidence index climbed 0.6 point to 92.8 this month. Economists had forecast the index easing to 89.0. It was in stark contrast with the University of Michigan’s Surveys of Consumers, which last week showed its Consumer Sentiment Index slumping to a record low in April.

WASHINGTON — U.S. consumer confidence unexpectedly edged higher in April amid a rally in share prices following a ceasefire in the war with Iran and improved perceptions of the labor market, helping to ease households’ financial worries for now. Despite the rise in confidence to a four-month high, the survey from the Conference Board on Tuesday showed higher gasoline prices stemming from the conflict with Iran remained a source of concern for consumers. Fewer planned vacations over the next six months and the share of those intending to drive to their holiday destinations was the lowest since April 2020. …The Conference Board said its consumer confidence index climbed 0.6 point to 92.8 this month. Economists had forecast the index easing to 89.0. It was in stark contrast with the University of Michigan’s Surveys of Consumers, which last week showed its Consumer Sentiment Index slumping to a record low in April.